Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

VaR value at several of the volatility estimation method and cl ...

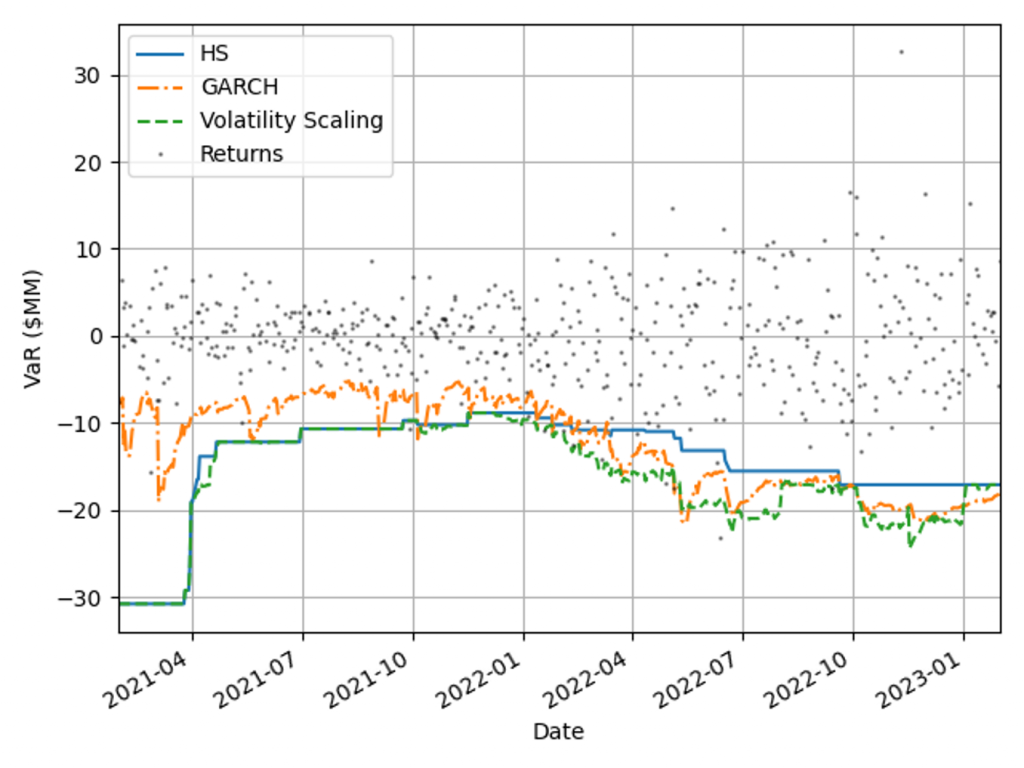

6. VaR time plot historical simulation with volatility updating ...

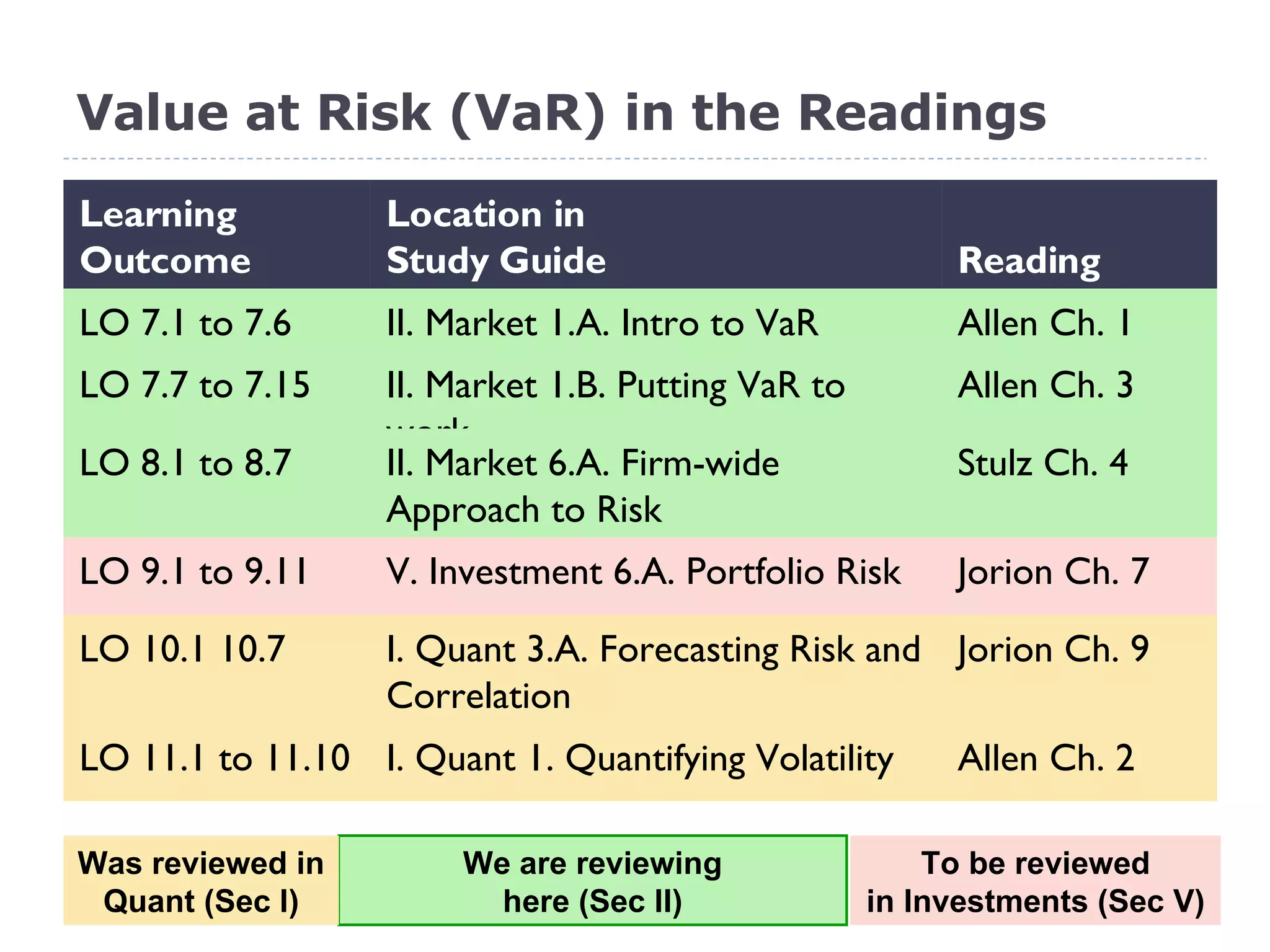

Quantifying Volatility in VaR Models | FRM Part I

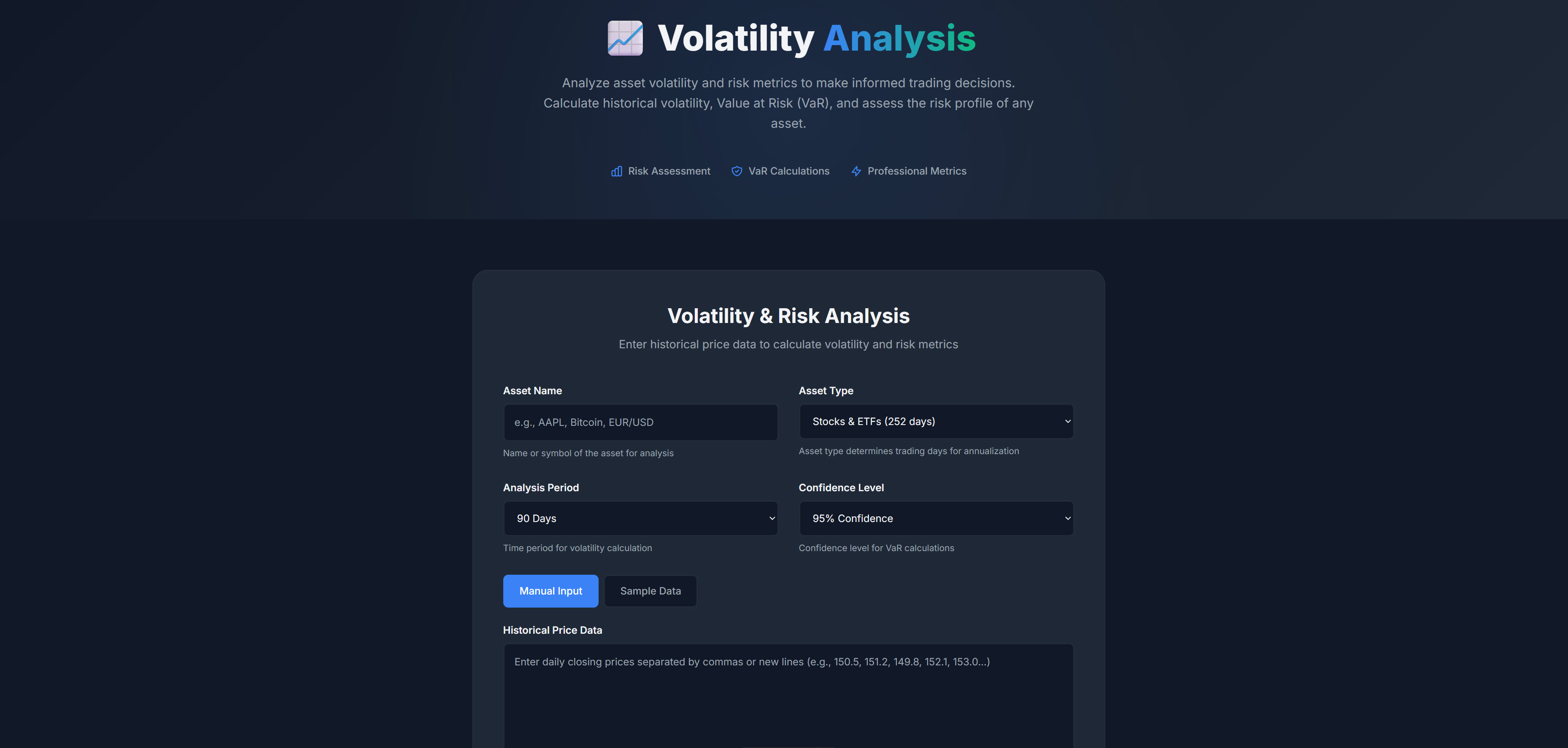

Volatility Analysis Tool – Free Historical Volatility & VaR Calculator ...

Forecasted volatility and VaR from january to december, 2020 | Download ...

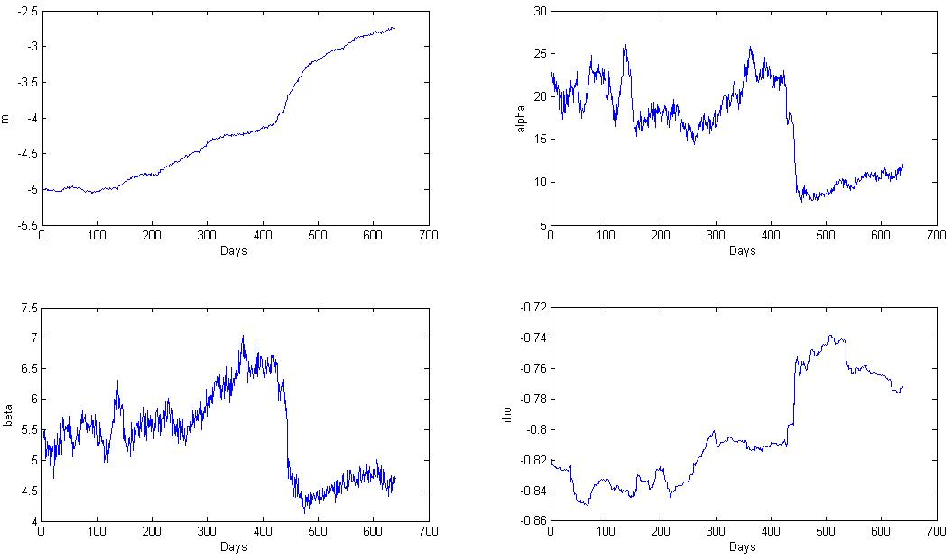

Stochastic volatility estimates from VAR models. Note: The red solid ...

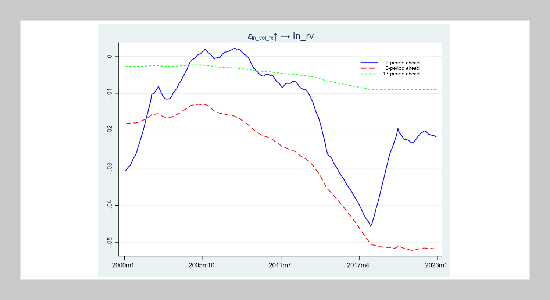

Log volatility estimates from VAR models—samples including and ...

Volatility and VaR forecast based on EWMA model | Download Scientific ...

(PDF) Volatility Sensitive Bayesian Estimation of Portfolio VaR and CVaR

Topic 52 Quantifying Volatility in VaR Models - Answers PDF | PDF ...

Volatility spillovers based on quantile VAR (extreme low quantile ...

Volatility Modelling and VaR Estimation Techniques

Relative Margins (%), Monthly volatility (Volm,%) and VaR (VaR_RiskM_m ...

VaR Volatility Models | PDF | Volatility (Finance) | Statistical Theory

Relative market volatility in the VaR economy. The figure plots ...

Figure 1 from Modeling and Forecasting the Markets Volatility and VaR ...

Dynamic volatility spillover in the quantile VAR (median quantile ...

Volatility spillovers based on quantile VAR (median Tau = 0.5). Note: a ...

The Result of Volatility H/L VAR Model Estimation | Download Table

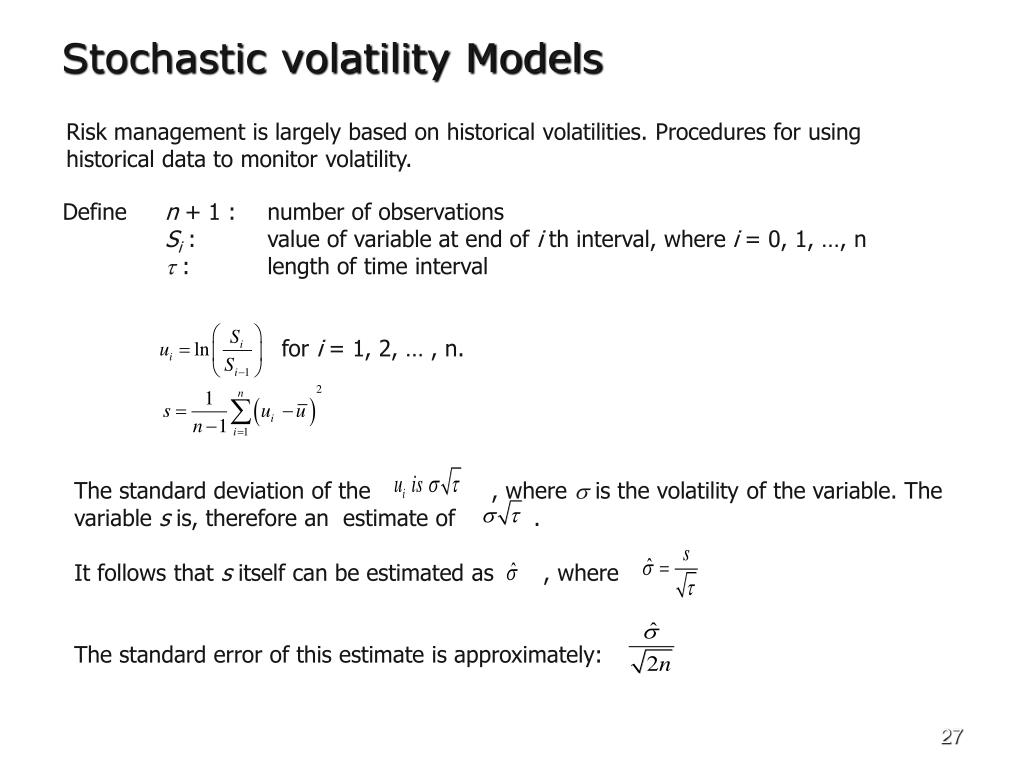

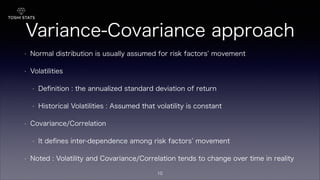

lecture 12.pdf - Quantifying Volatility in VaR Models Defining VaR ...

Contributions of Volatility Based on VAR Model in Table 14 | Download Table

Volatility spillover table for the 2N-dimensional VAR model with ...

Table 1 from Volatility Sensitive Bayesian Estimation of Portfolio VaR ...

Average volatility spillover for the 2N-dimensional VAR model with ...

Results of Investment Volatility Equation in the VAR | Download Table

The best performing models for out-of-sample volatility and VaR ...

VaR Volatility Man. Risiko_Kelompok 2.pptx

Volatility and Correlation Results: International VAR | Download Table

Volatility spillovers based on quantile VAR – Sub-sample analysis ...

The impact of volatility on VaR. Note that the symbols “∘”, “*”, and ...

VaR Backtesting in Turbulent Market Conditions : Enhancing the ...

PPT - Week 10: VaR and GARCH model PowerPoint Presentation, free ...

Chapter 8 Value at risk | Volatility modelling and market risk analysis ...

(PDF) Value at Risk (VaR) Using Volatility Forecasting Models: EWMA ...

Volatility, VaR and CVaR in a (a) loss and (b) revenue distribution ...

High-frequency enhanced VaR: A robust univariate realized volatility ...

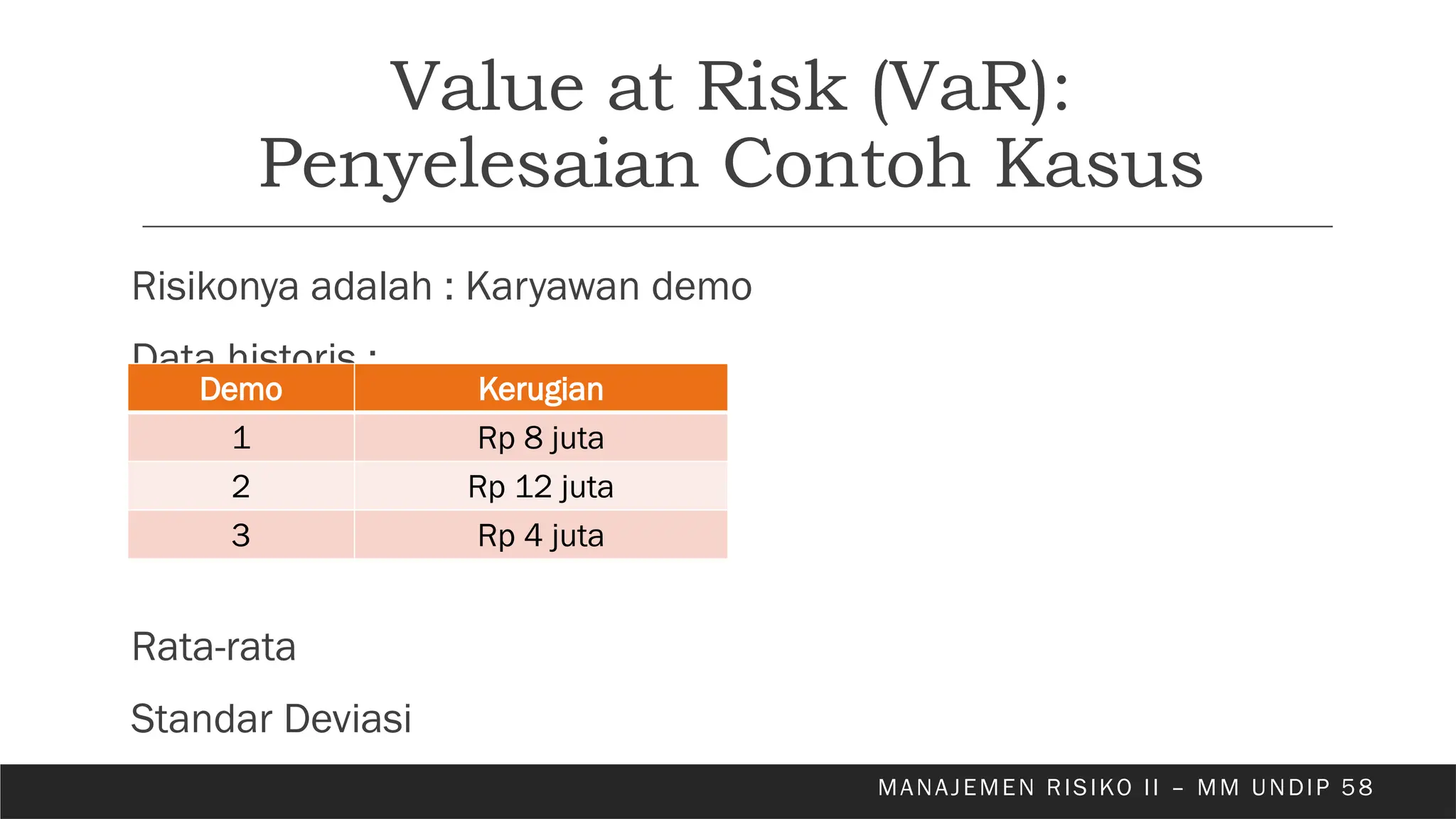

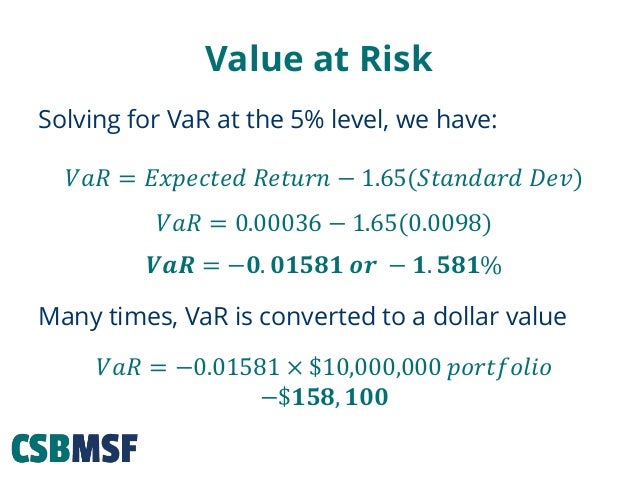

Module 7 var analytical method step by step

value at risk - What does this formula (to derive annualized volatility ...

Forecasting Volatility with the GARCH-VAR Model | by Cristian Velasquez ...

Dynamic multipliers of VAR model controlling for cryptocurrency ...

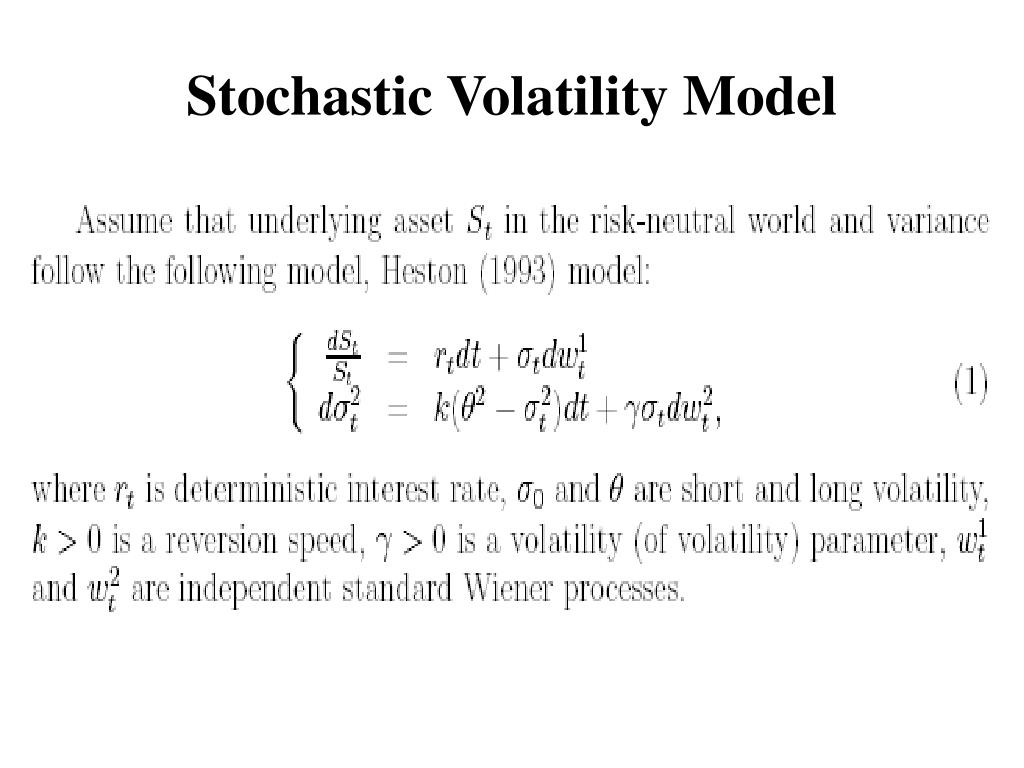

PPT - Market Risk Management using Stochastic Volatility Models ...

VAR estimation results under different term structures. | Download ...

Volatility Swap - Definition, Explained, Example, Vs Variance Swap

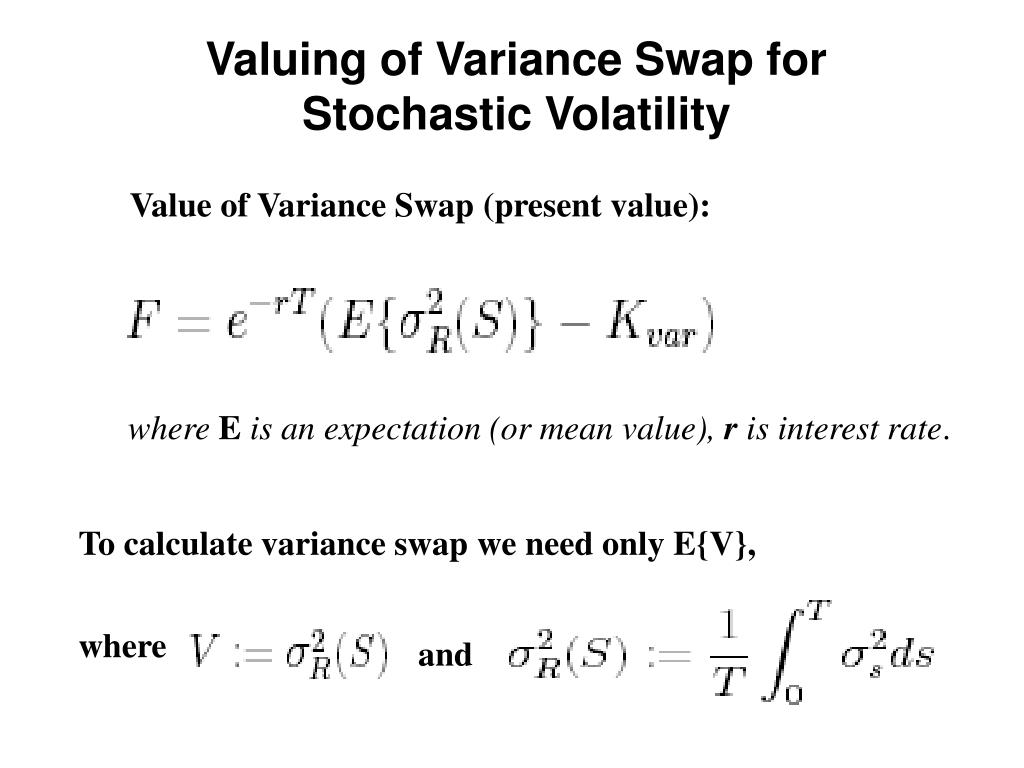

PPT - Modeling of Variance and Volatility Swaps for Financial Markets ...

Realized Volatility (Definition,Formula)| How to Calculate Realized ...

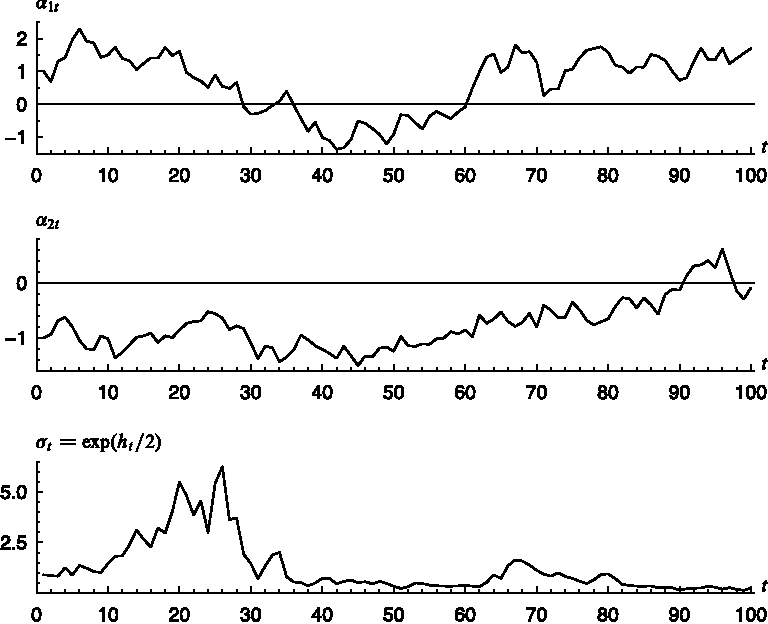

Estimated stochastic volatility from the TVP-VAR Model. a Variance of ...

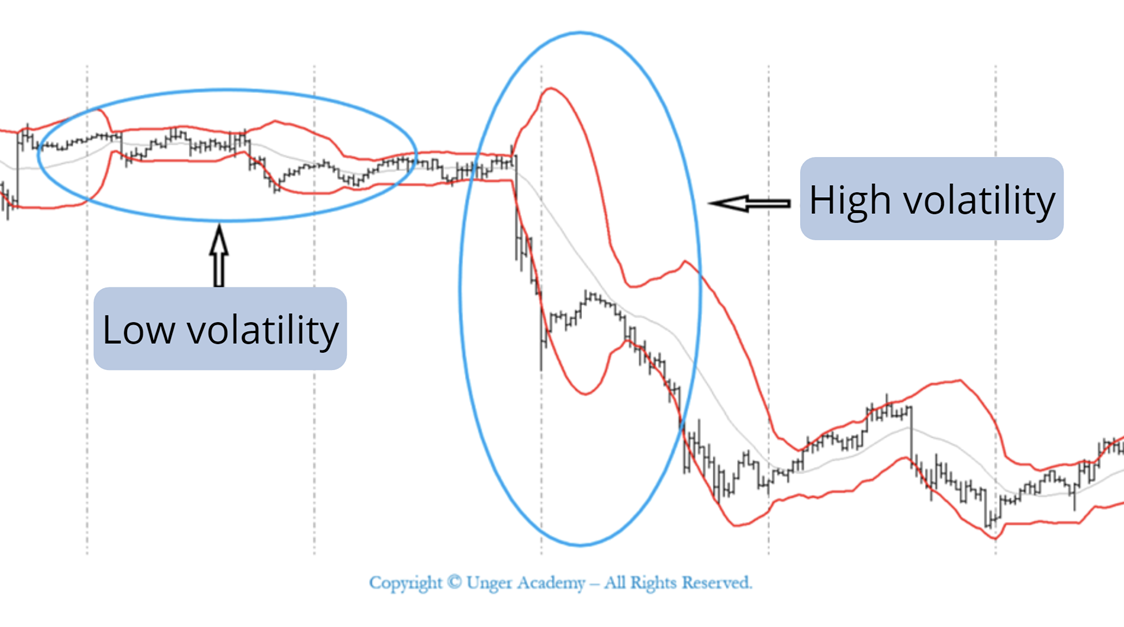

What Is Volatility and Why It Matters in Trading | Unger Academy

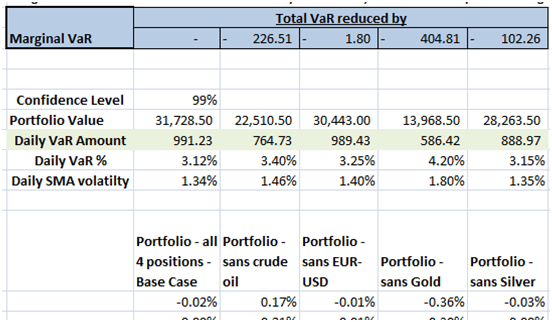

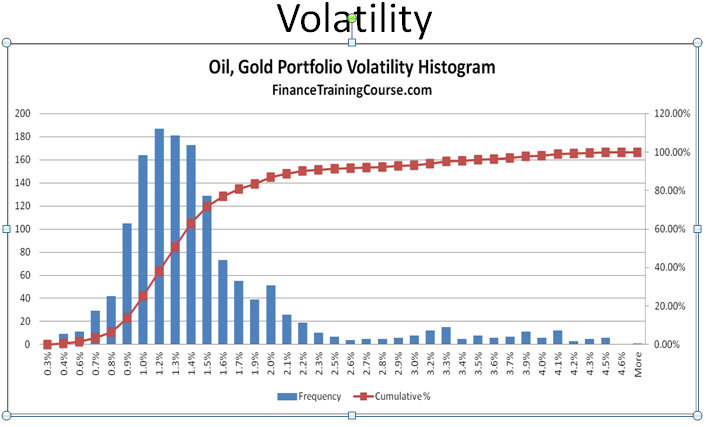

Incremental VaR & other VaR metrics - FinanceTrainingCourse.com

Advanced Volatility Modeling (Lecture Notes) — IMF - STI Risk Based ...

Quantitative approach to risk management: Applying VaR model to ...

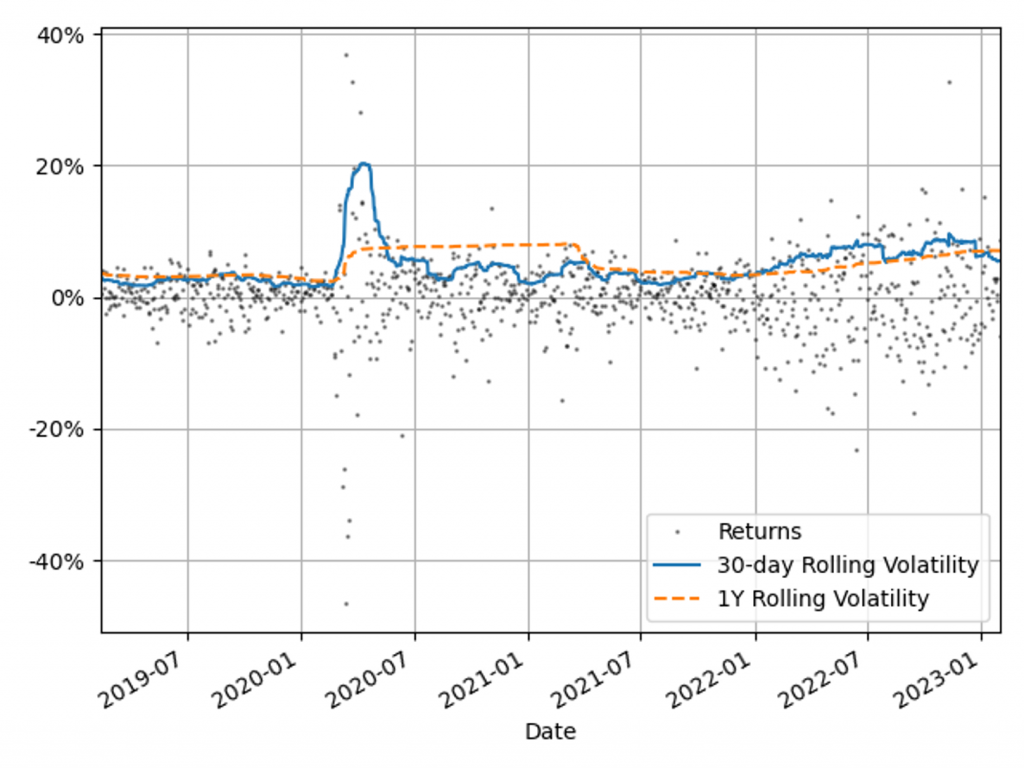

Mean, Var, and CV of S&P 500 volatility estimates for 20-day time ...

VAR model between volatilities indexes and their lagged values ...

Introduction to VaR | PDF

Information of historical VaR, conditional volatility of return, price ...

Figure 1 from Time-Varying Parameter VAR Model with Stochastic ...

(PDF) Volatility Modelling and VaR: The Case of Bitcoin, Ether and Ripple

(PDF) The Stochastic Volatility Model, Regime Switching and Value-at ...

Wavelet coherence for blockchain-based assets for DY volatility ...

Volatility Forecasting — arch 4.16 documentation

Comparison and Forecasting of VaR Models for Measuring Financial Risk ...

(PDF) Structural Compressed Panel VAR with Stochastic Volatility: A ...

Modeling and forecasting. Volatility - online presentation

VAR impulse responses of the stablecoin stability Measure (2)-The ...

Value at Risk (VaR) explained: calculation and FAQs

What is the link between VIX and VaR? | Close Mountain Advisors

Counterpart Regulatory Process - ppt download

A time-varying-parameter vector autoregression model with stochastic ...

From Risk to Value at risk in Excel.

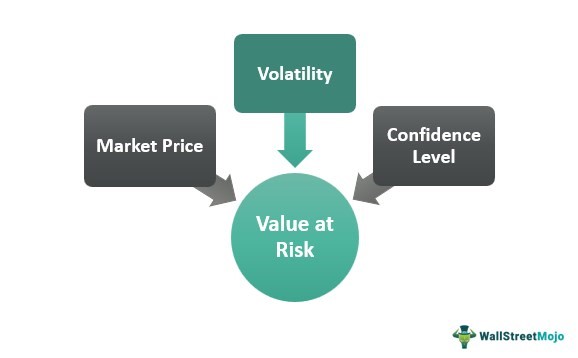

Value at Risk (VaR) | Definition, Components, & Calculation

GitHub - anhdanggit/volatility-garch-VaR: Simulate and estimate ...

Value at Risk (VaR) - What Is It, Methods, Formula, Calculate

Difference of the out-of-sample forecast errors between the VAR(1 ...

What Is A Multiset Volatile Table at Nate Hocking blog

Chapter 14 Assessing the Value of IT - ppt download

PPT - Mean-Reverting Models in Financial and Energy Markets PowerPoint ...

Risk Management Online Training Workshop

INDIAN INSTITUTE OF BANKING & FINANCE - ppt download

What is Value at Risk (VaR)?

Bank Credit and Housing Prices in China: Evidence from a TVP-VAR Model ...

Value at Risk (VaR), Intro | PPT

Figure 2 from An Improved Procedure for VaR/CVaR Estimation under ...

Calculating Value at Risk - Approach Specific Steps ...

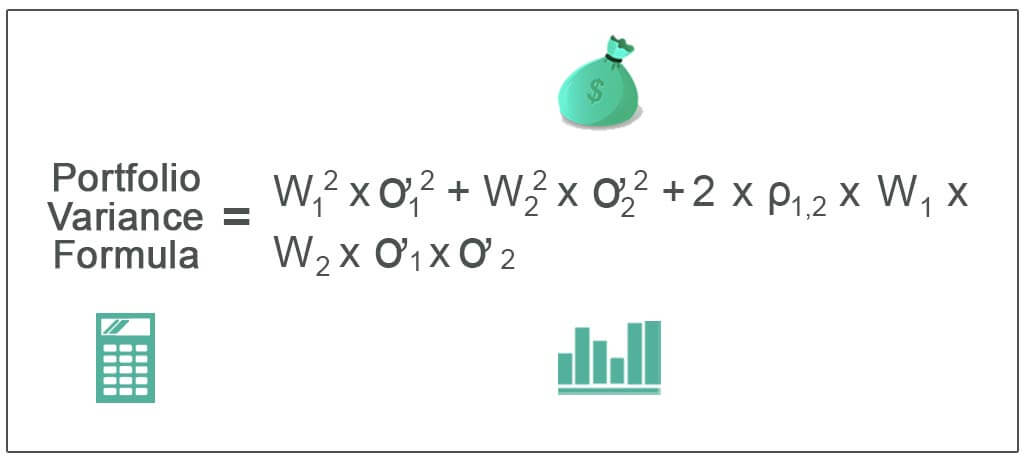

Portfolio Variance Formula (example)| How to Calculate Portfolio Variance?

Value at Risk (VaR): Definition, Models, and Applications in Portfolio Risk

Research on the Time-Varying Relationship between Macroeconomic ...

Figure 6 from An Improved Procedure for VaR/CVaR Estimation under ...

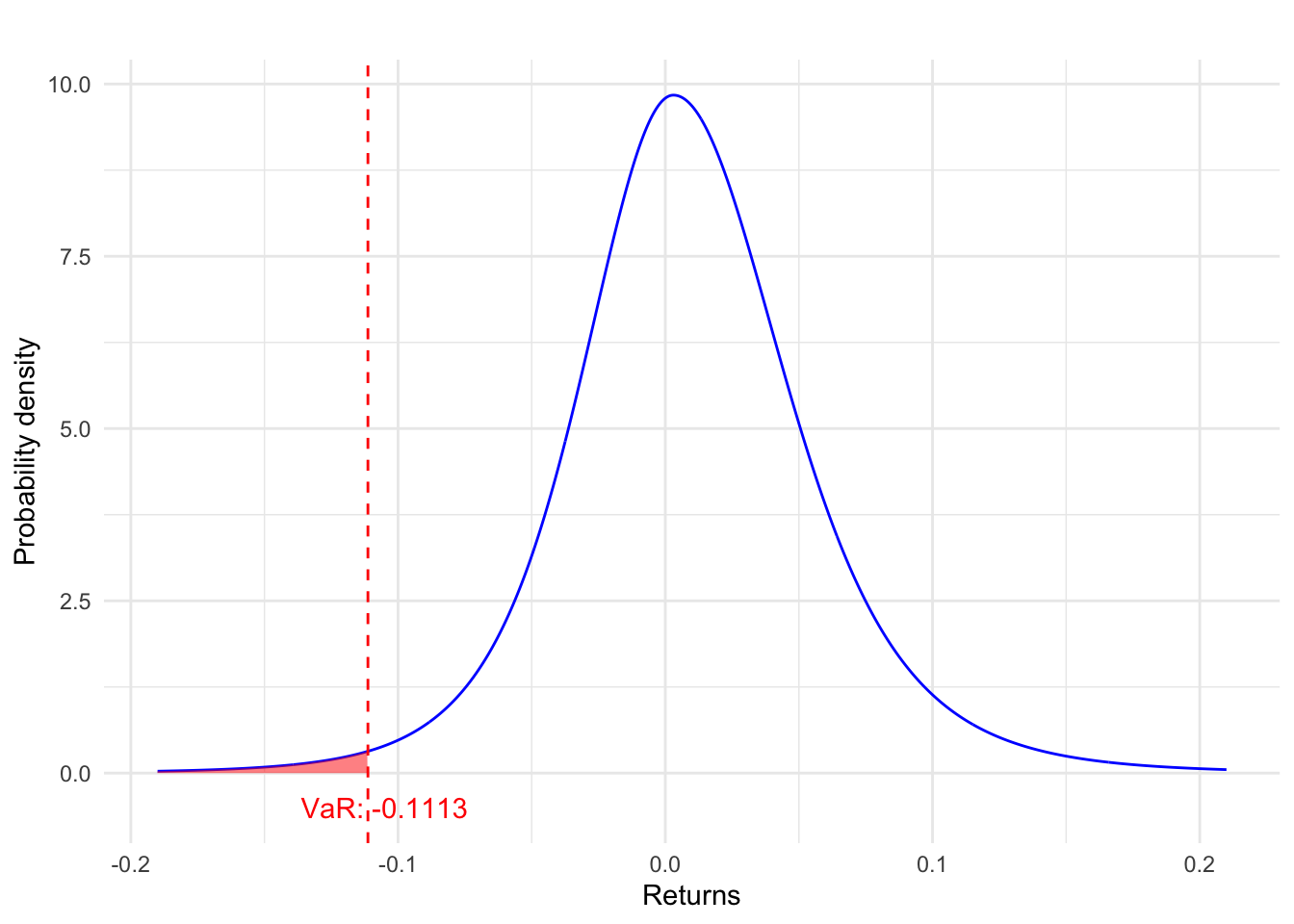

The one-step-ahead predictive distribution of volatility, return and ...

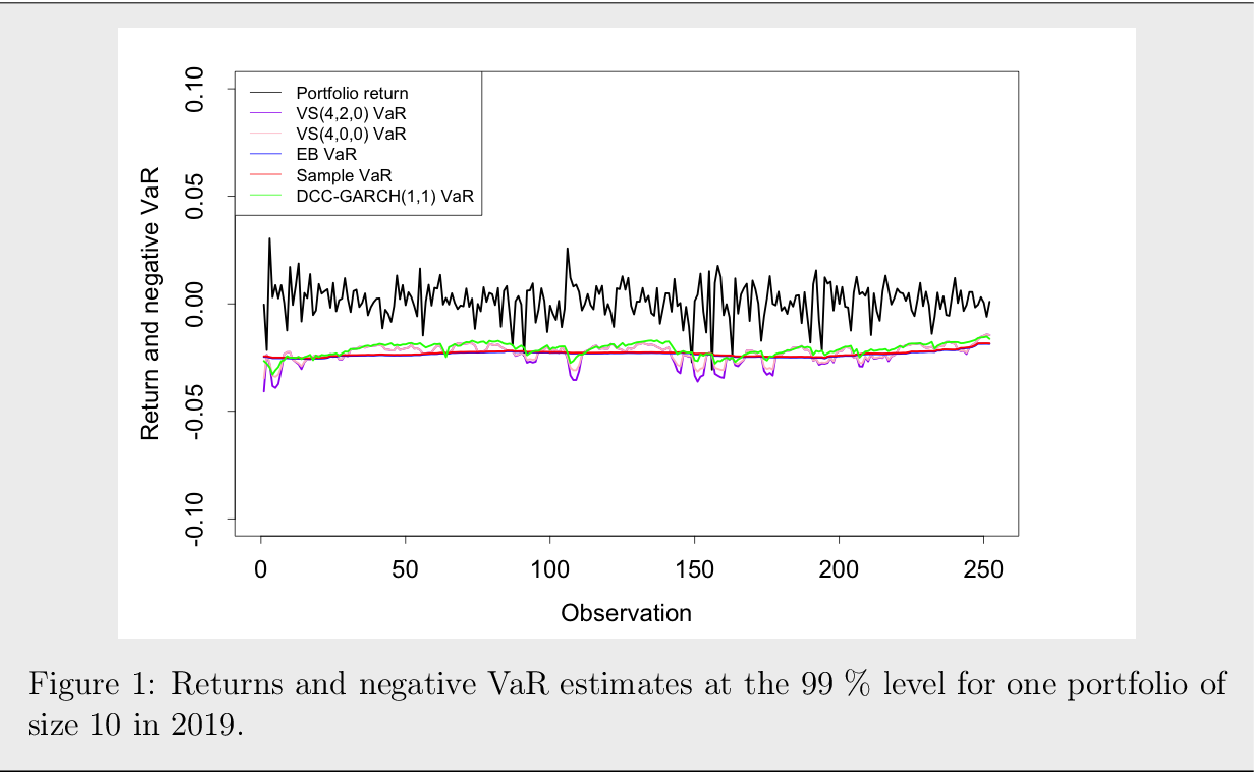

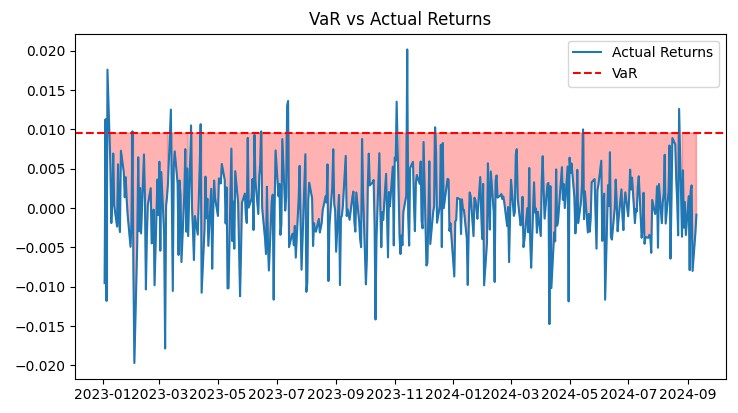

further illustrates how the models behave by showing how the returns ...