Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

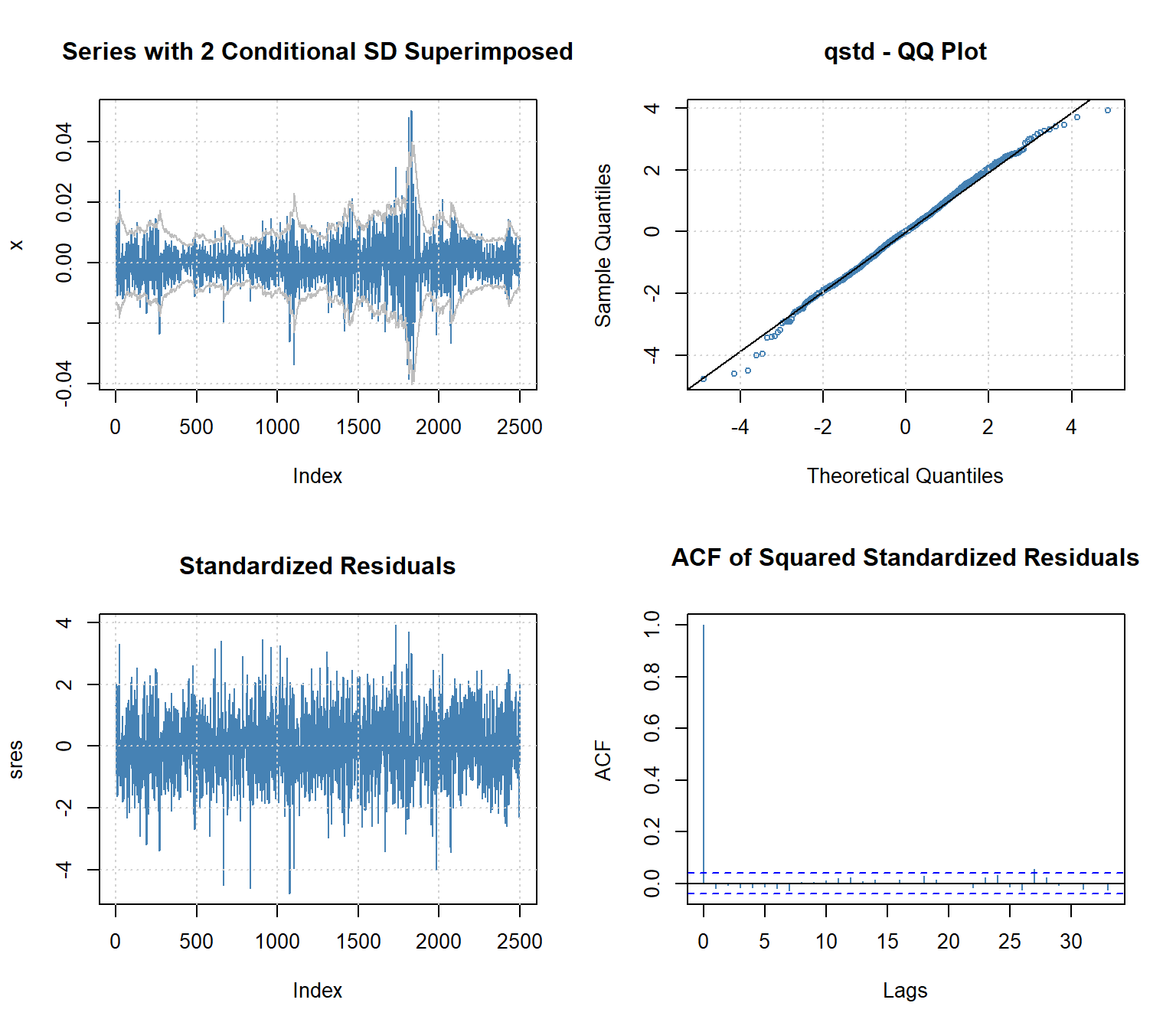

GARCH simulation and estimation from scratch

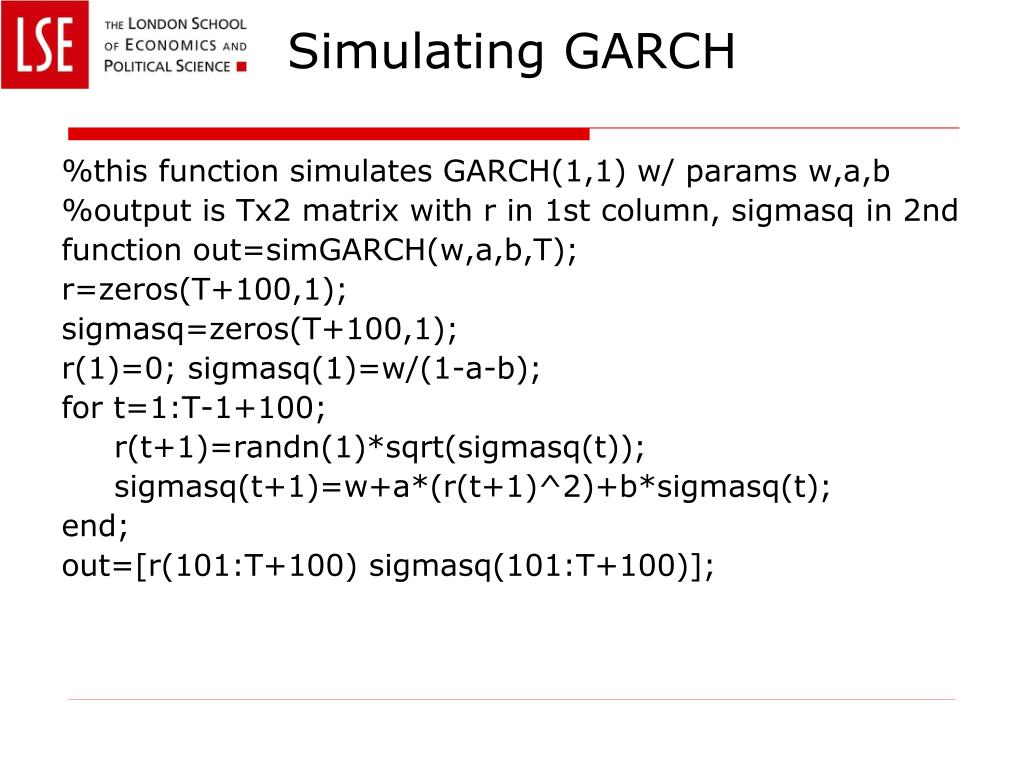

Detailed framework of Monte Carlo simulation based GARCH model ...

GARCH model simulation | Download Table

Innovation of the Component GARCH Model: Simulation Evidence and ...

(PDF) Innovation of the Component GARCH Model: Simulation Evidence and ...

(PDF) The smooth transition GARCH model for simulation of highly ...

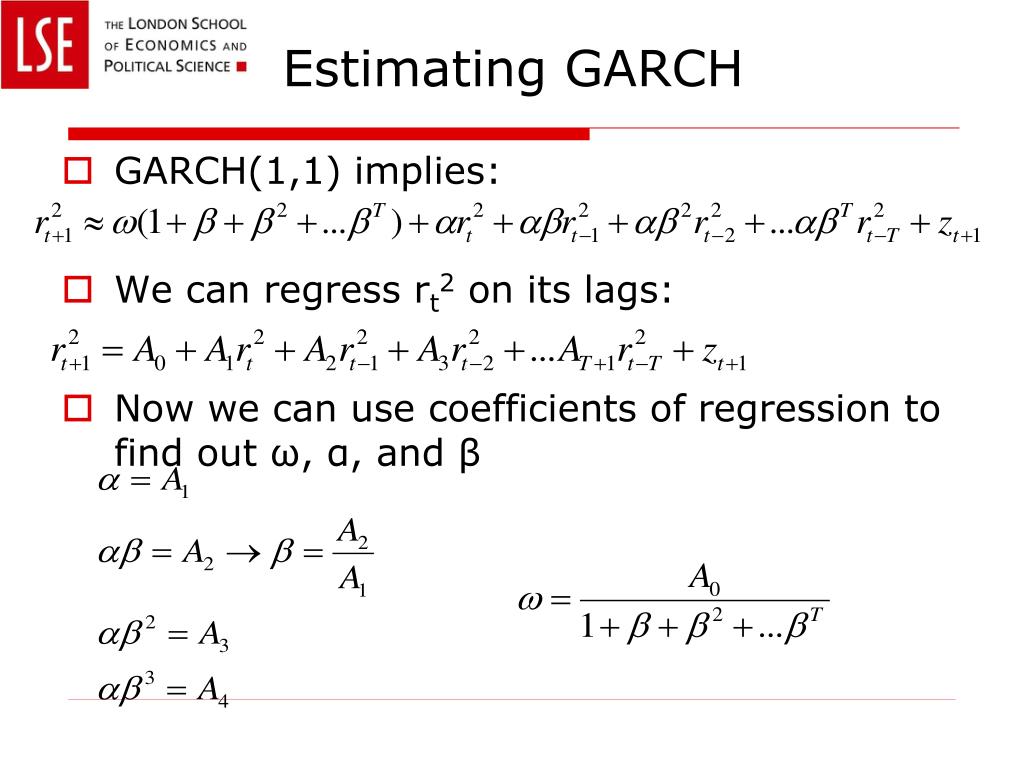

Talk Garch 11 | PDF | Statistical Analysis | Teaching Mathematics

Arima Garch 11 Modelling and Forecasting For A Ge Stock Price Using R ...

(PDF) A GARCH option pricing model with filtered historical simulation

(PDF) MCMC Simulation of GARCH Model to Forecast Network Traffic Load

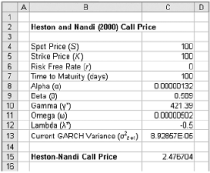

16 The parameters in a GARCH 11 model are omega 0000002 alpha 004 and ...

option pricing - GARCH process simulation in R - Quantitative Finance ...

Figure 1 from MCMC simulation of GARCH model to forecast network ...

A GARCH Option Pricing Model with Filtered Historical Simulation

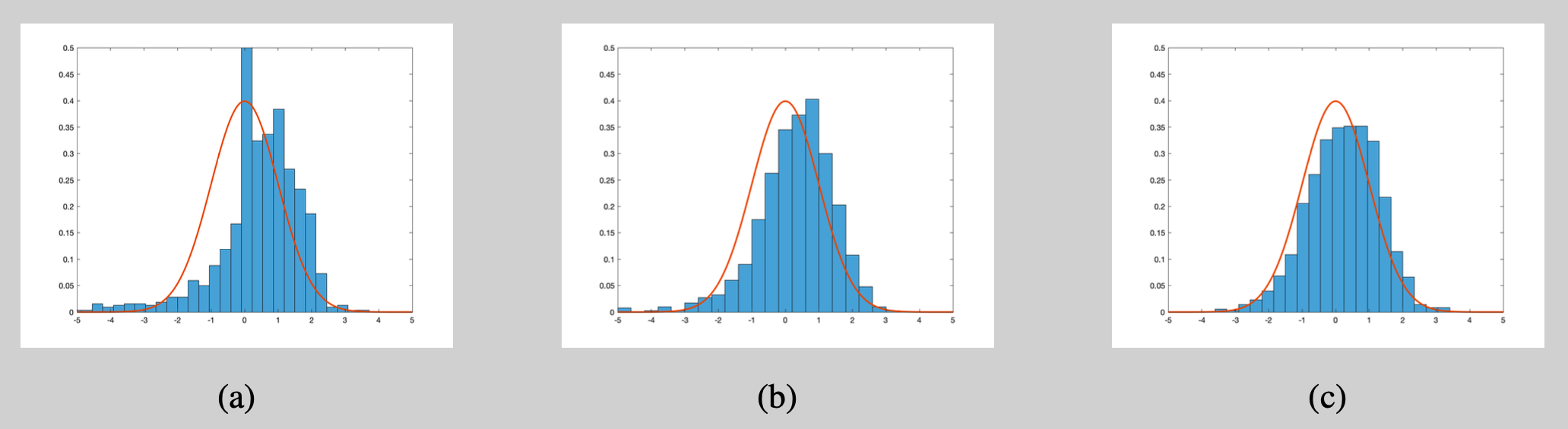

In panel (a), we show the simulation results for a GARCH-normal(1,1 ...

Financial econometrics xiii garch

Simulation results for the Student-t AR(1)-Asymmetric Power GARCH(1,1 ...

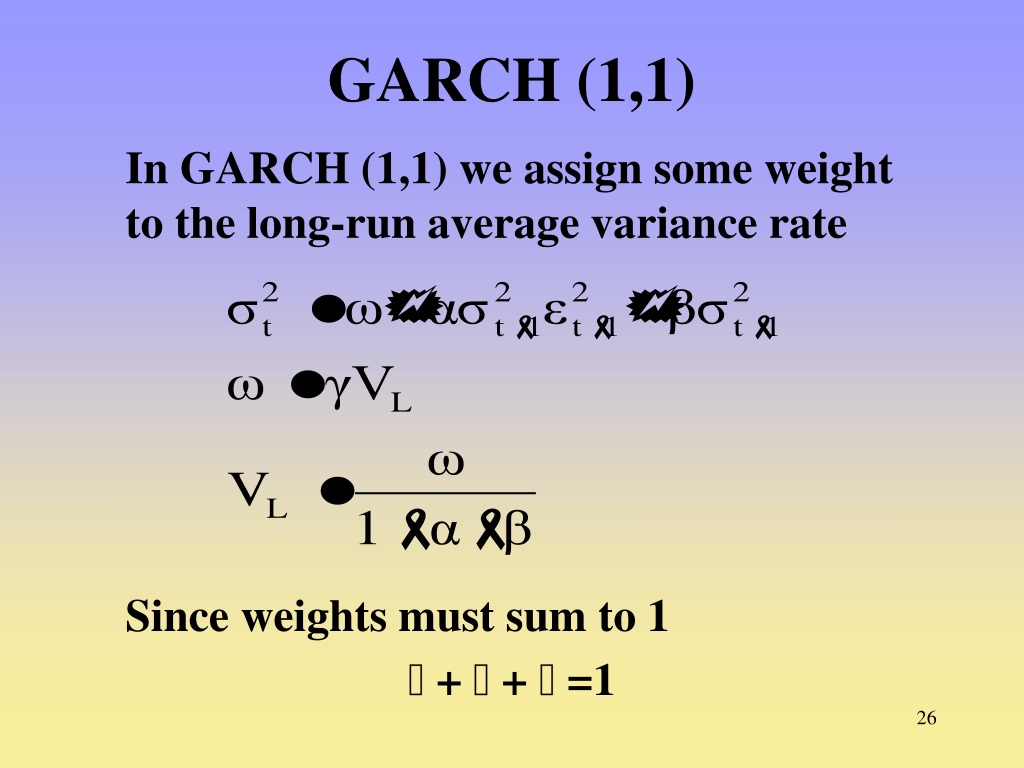

PPT - GARCH and VaR PowerPoint Presentation, free download - ID:6961496

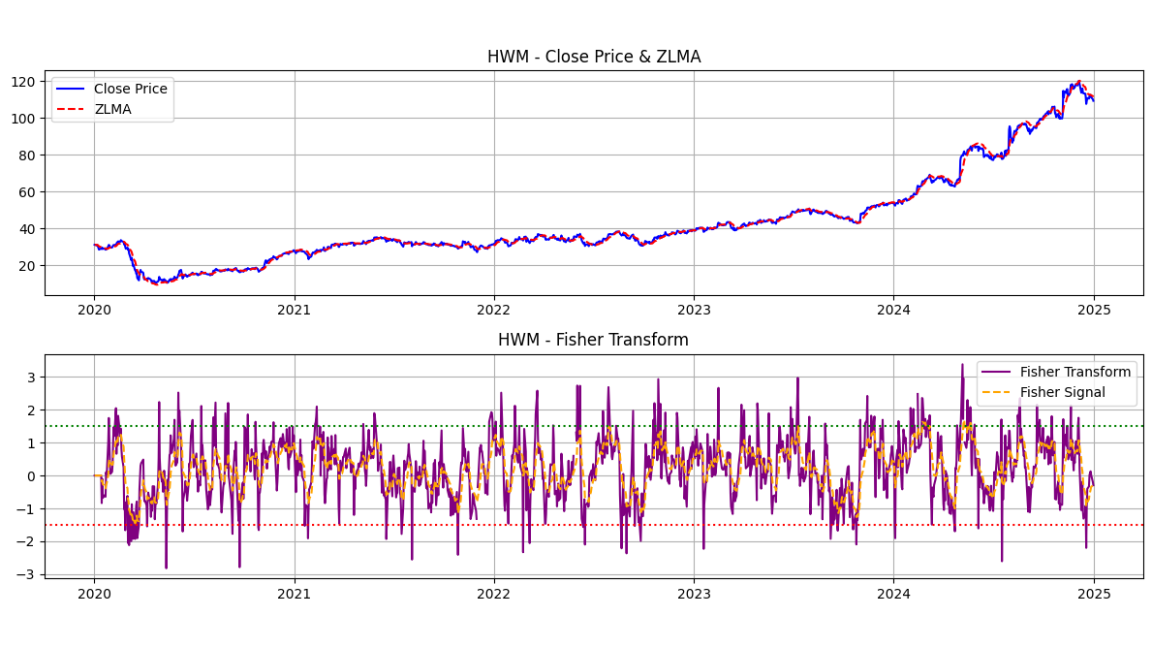

GARCH Indicator

PPT - Week 10: VaR and GARCH model PowerPoint Presentation, free ...

GARCH vs. GJR-GARCH Models in Python for Volatility Forecasting

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

Chapter 10 GARCH models | Volatility modelling and market risk analysis ...

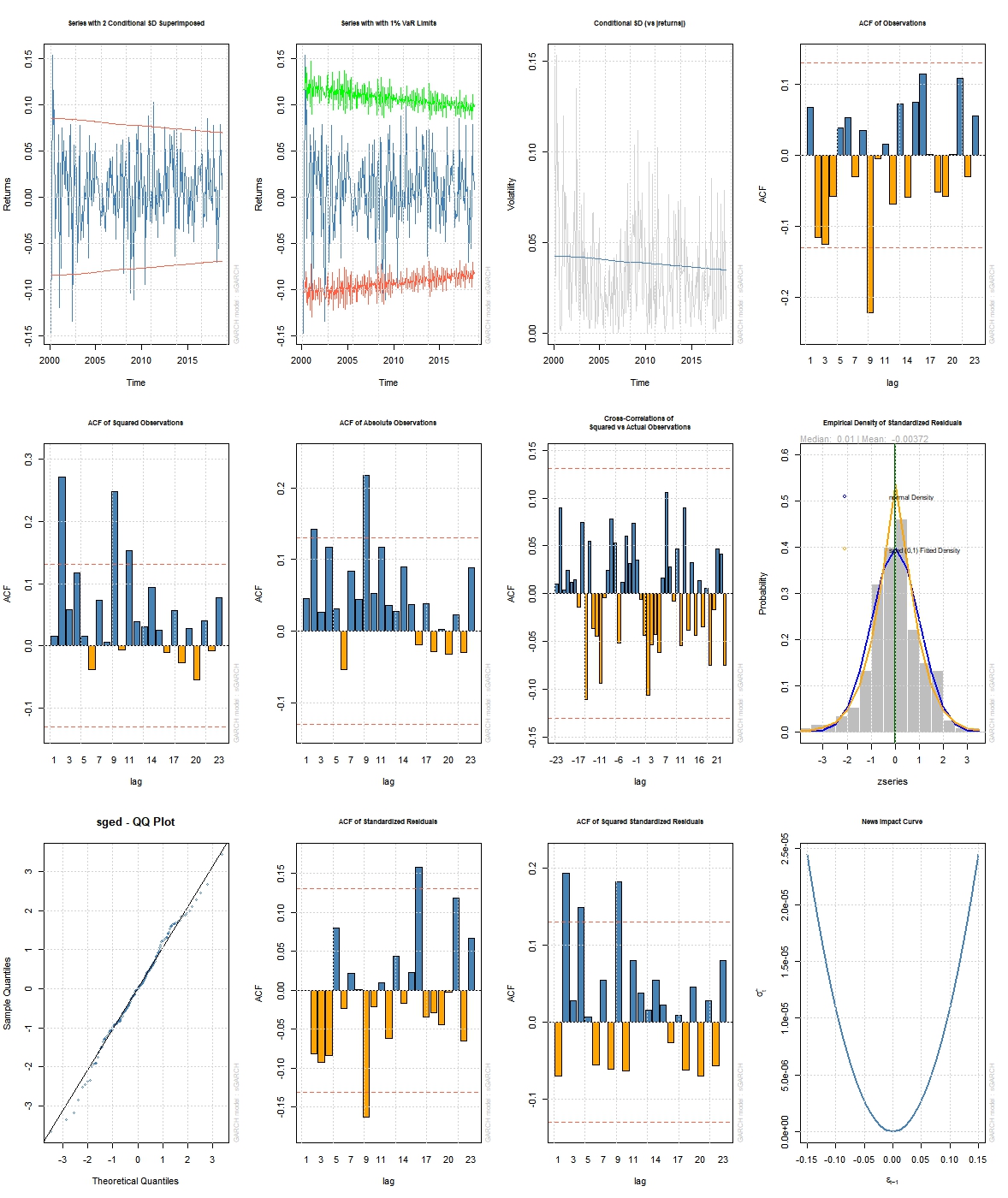

Garch (1, 1) the Figure As can be seen from the Figure 5 above, the ...

Financial econometrics xiii garch | PPT

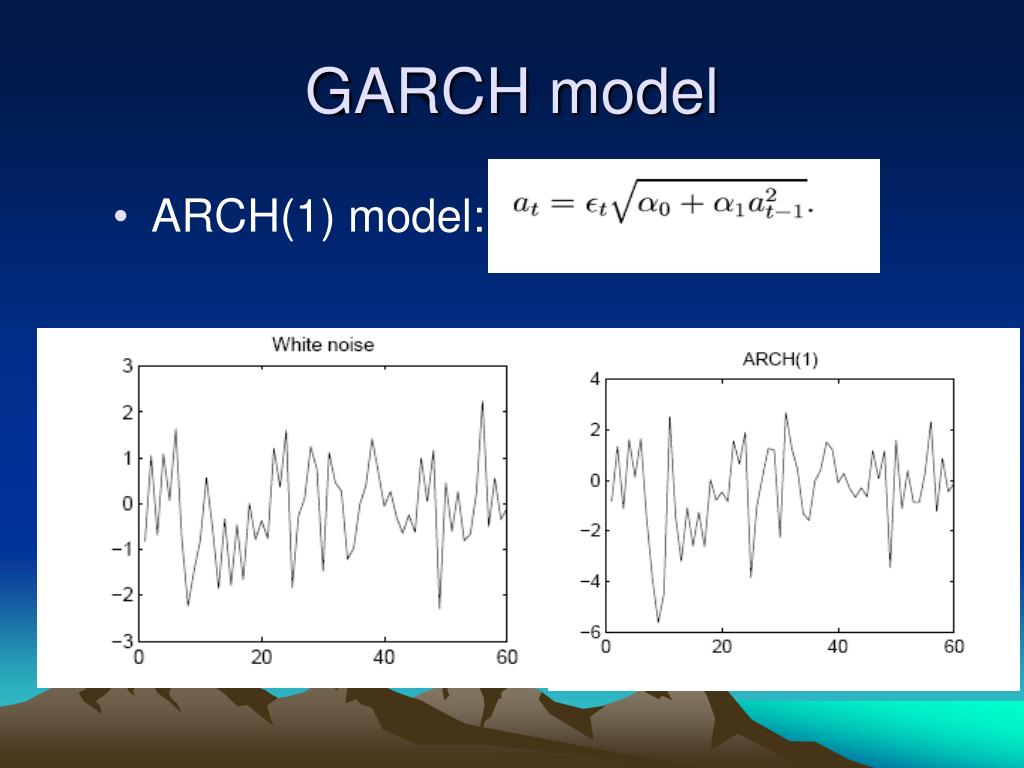

Arch & Garch Processes | PDF

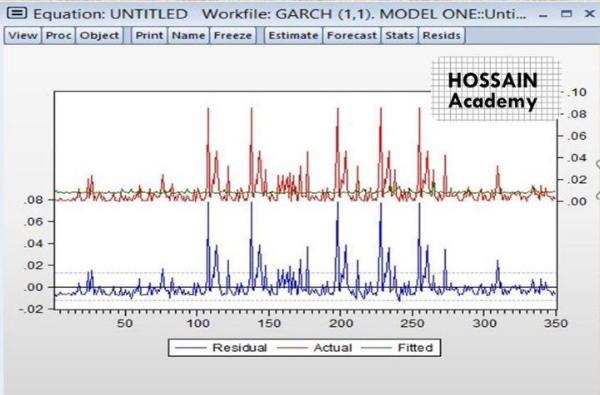

The USD/ALL exchange rate forecasted data through GARCH (1;1) Source ...

PPT - OPTIONS PRICING AND HEDGING WITH GARCH PowerPoint Presentation ...

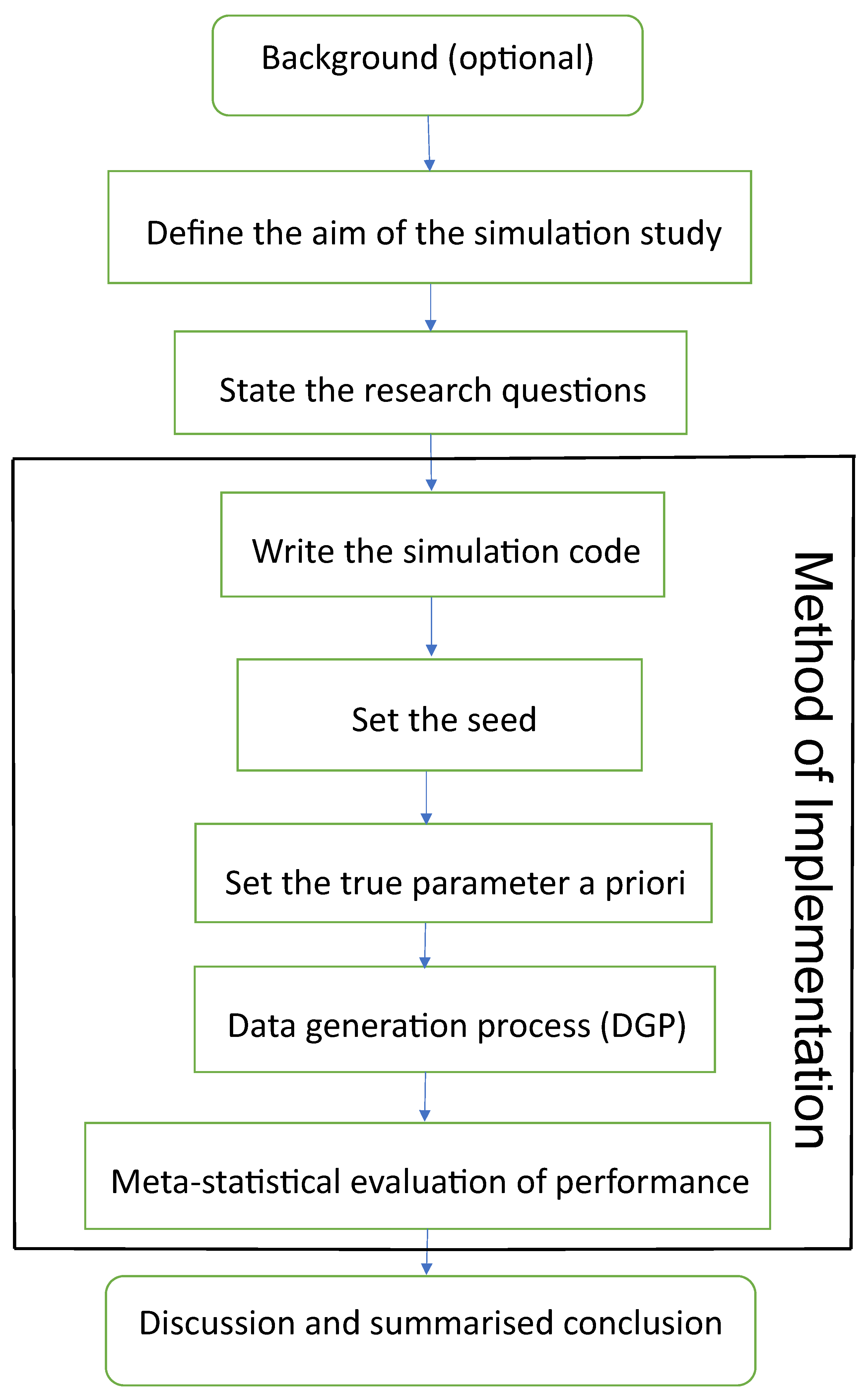

Framework for Simulation Study Involving Volatility Estimation: The ...

GARCH model comprehensive modeling flow chart 3. Example analysis ...

Empirical Safety Stock Estimation Using GARCH Model, Historical ...

GARCH Models for Volatility Forecasting: A Python-Based Guide | by The ...

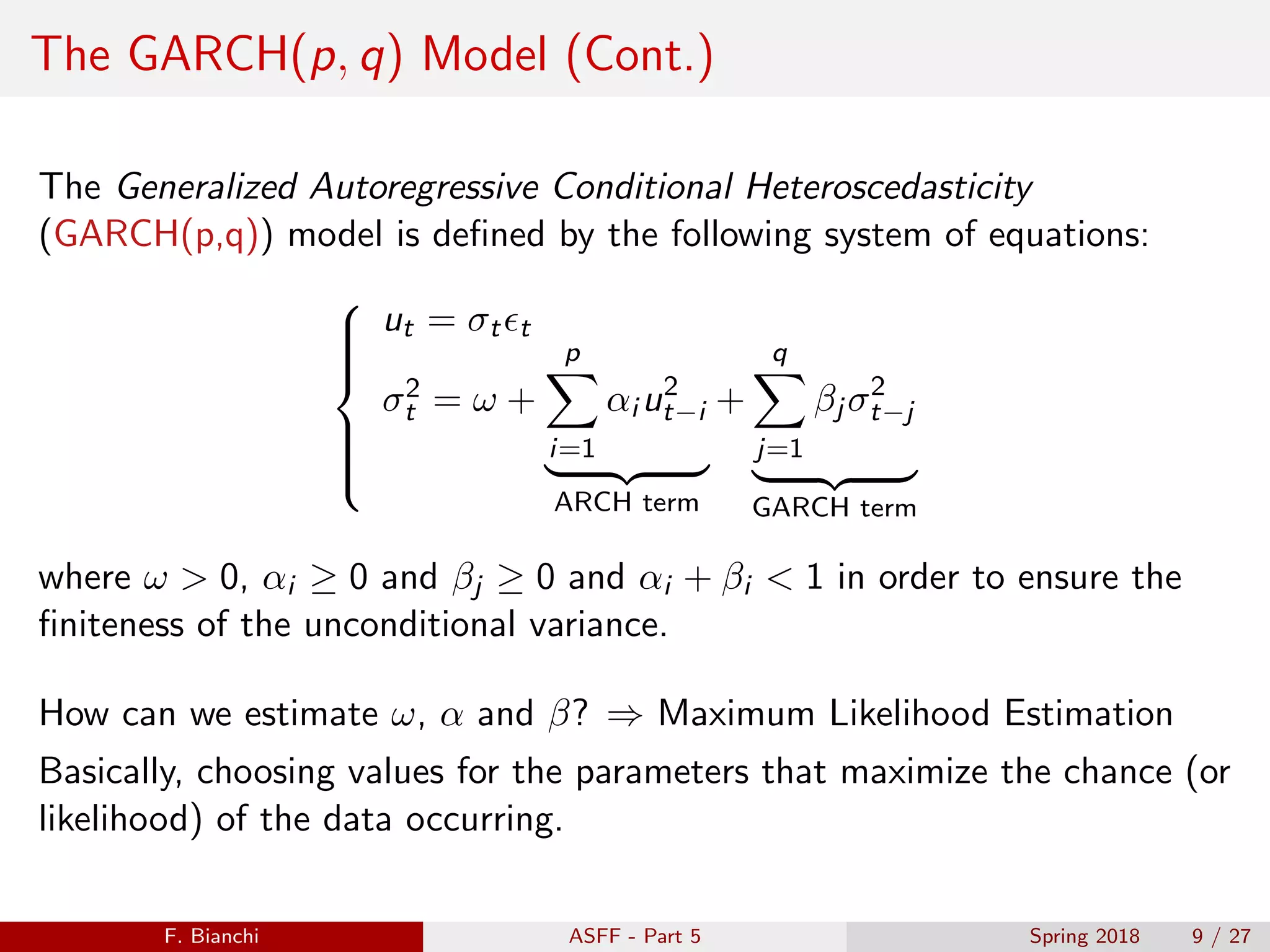

volatility-modeling-arch-and-garch-handout.13 - GARCH Definition ...

(PDF) Framework for Simulation Study Involving Volatility Estimation ...

Long-term asset allocation strategies based on GARCH models - a ...

(PDF) M-Estimation in Garch Models

Simulation Framework to Determine Suitable Innovations for Volatility ...

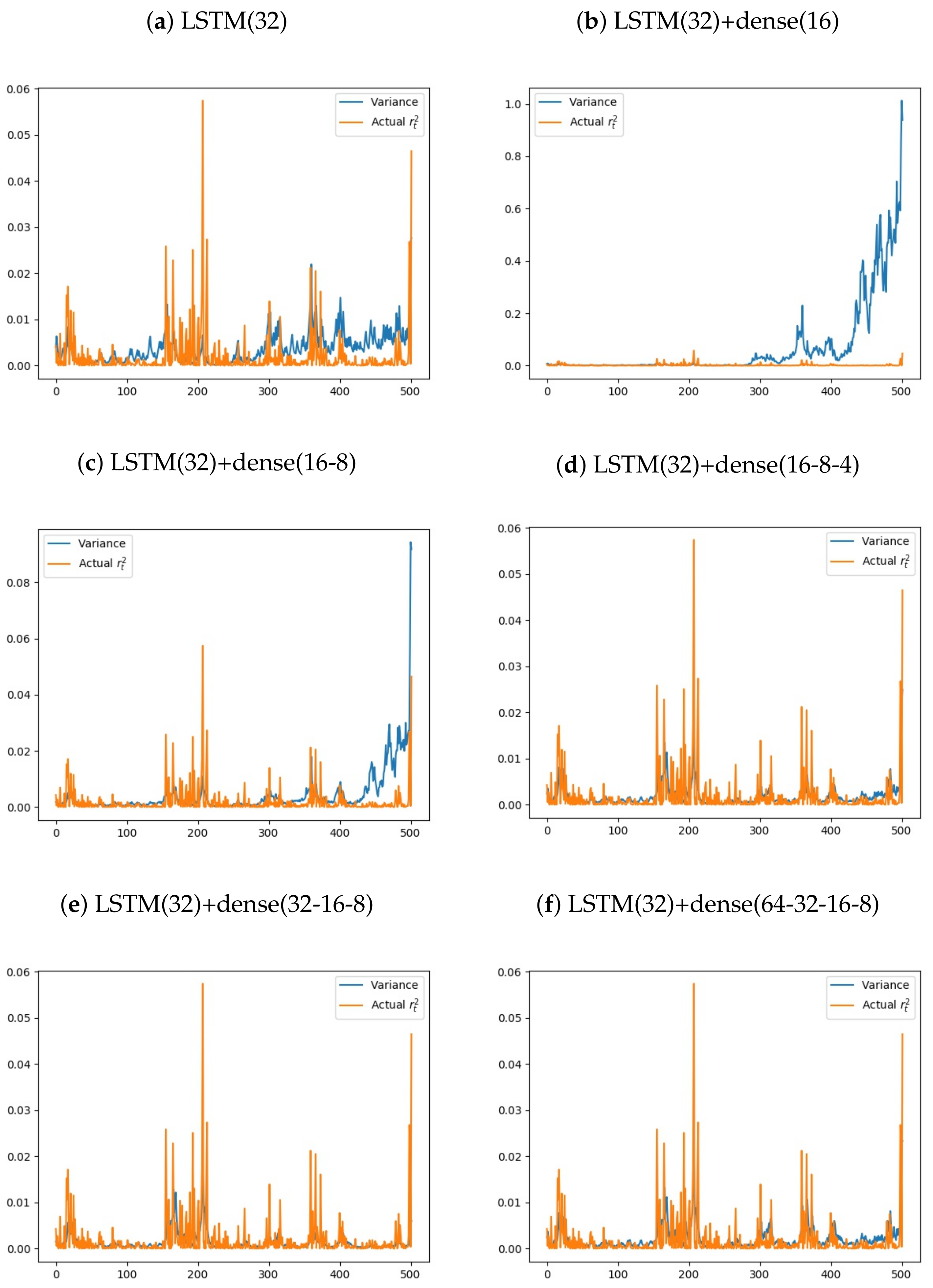

A GARCH Model with Artificial Neural Networks

Simulation results from the GARCH(1,1)-M models. | Download Scientific ...

GARCH Option pricing(Simulation) : 네이버 블로그

Forecasting Volatility: Deep Dive into ARCH & GARCH Models | by Daniel ...

Build a GARCH Simulator - Next Level Backtesting - YouTube

(PDF) Estimates and Forecasts of GARCH Model under Misspecified ...

Engle 2010 Garch 101 The Use of Arch Garch Models in Applied ...

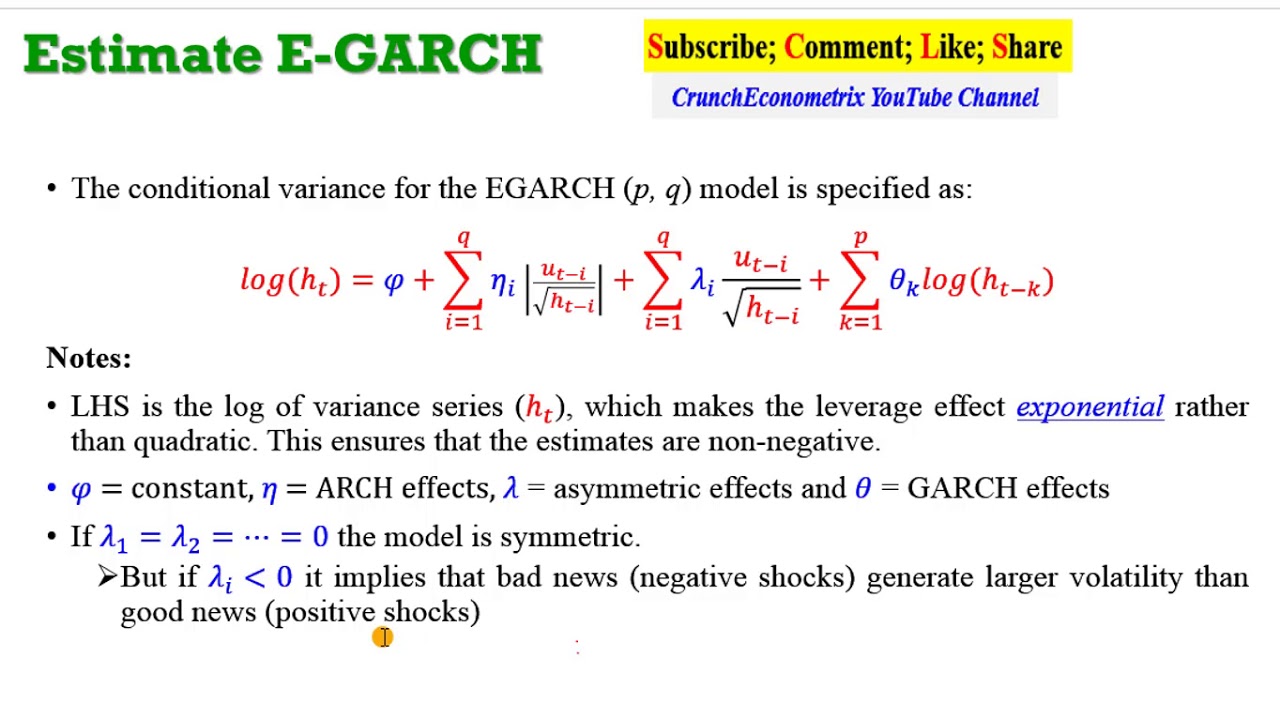

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch # ...

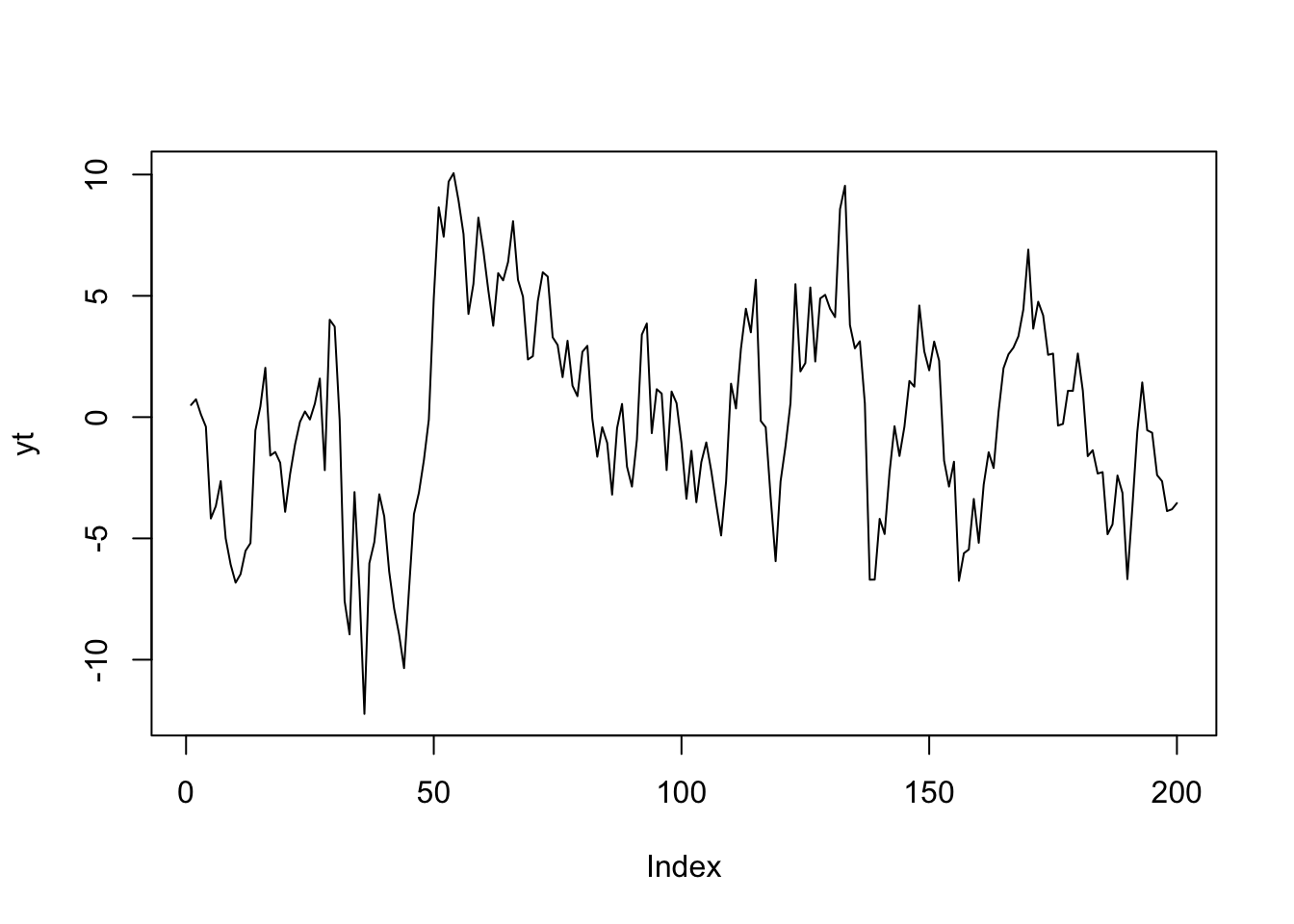

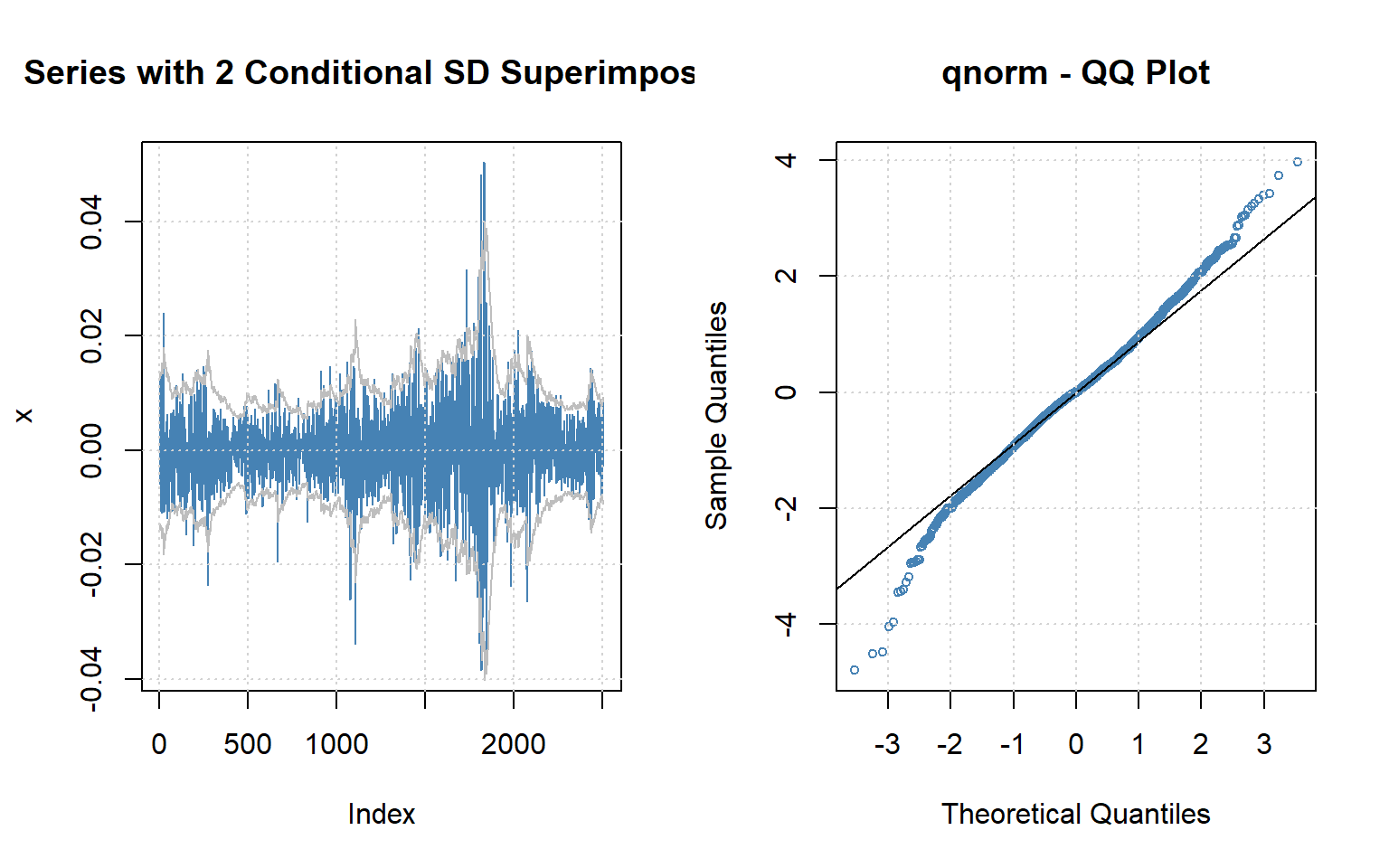

GARCH(1,1) Process Analysis and Simulation | PDF

Estimating parameters of GARCH (1.1) model with normal distribution ...

GARCH Analysis on Volatility Patterns | EODHD APIs Academy

GARCH Models: Identifying the Correct Model

Long-term asset allocation strategies based on GARCH models — a ...

GARCH Models - MATLAB & Simulink

Volatility Forecasting - A Performance Measure of Garch Techniques With ...

11. ARCH vs GARCH - YouTube

Modelling Volatility with the GARCH Model • Economics.Town

Simulate GARCH Models - MATLAB & Simulink

GitHub - LinhNguyen-MyLi/GARCH-model-forecast: Apply GARCH (1,1) model ...

Portfolio Optimization on Multivariate Regime-Switching GARCH Model ...

PPT - Module 3 GARCH Models PowerPoint Presentation, free download - ID ...

What Is GARCH Model In Python? - AskPython

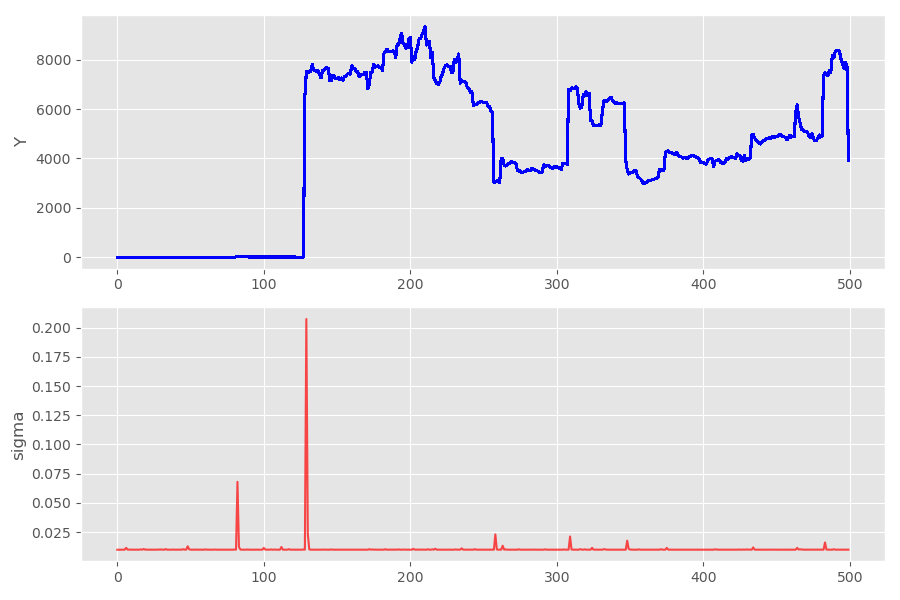

4 -A GARCH(1, 1) process with 2 breaks (K * = 3) following the scenario ...

The figure shows the estimated GARCH(1,1) processes used in the ...

garch11_model · InferHub

GitHub - DavidAlexanderMoe/Financial-Time-Series-Analysis-and ...

Time Series Analysis - 6 Generalized Autoregressive Conditional ...

3: EURUSD forecast methods (GJR-GARCH-simulation Vs. VAR) - YouTube

11.1 ARCH/GARCH Models - India Dictionary

Model GARCH(1,1) AR(1) | Download Scientific Diagram

How to Build ARMA-GARCH Models Correctly? | by Charlie Lai | Medium

PPT - Volatility PowerPoint Presentation, free download - ID:9413319

The GARCH(1,1) model and its extensions | Hanno Reuvers

ARIMA和ARIMA-GARCH模型预测股票价格-R语言 - 知乎

ARMA-GARCH for Time Series — phat-tails 0.0.11 documentation

(PDF) Coordinate gradient descent algorithm in adaptive LASSO for pure ...

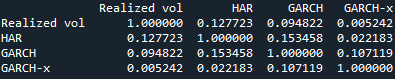

GitHub - KinH8/Realized-GARCH: Incorporating a realized measure of ...

(PDF) Empirical performance of GARCH, GARCH-M, GJR-GARCH and log-GARCH ...

(PDF) [enter Paper Title]Simulation-Based Approach to Persistence in ...

Simulated samples from the GARCH(1,1) model (24), cases 1 and 2 ...

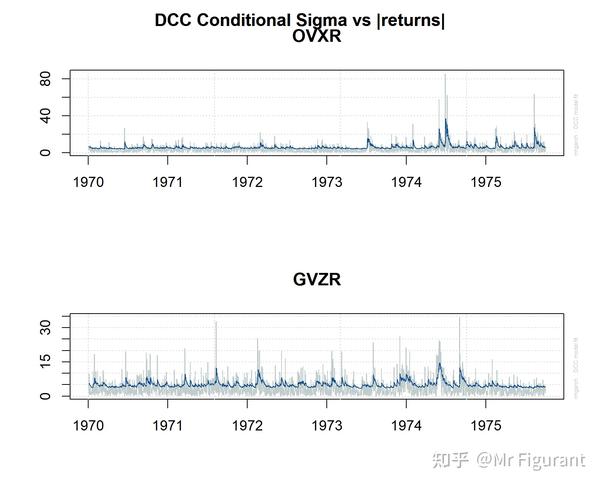

R语言学习:如何构建DCC-GARCH模型? - 知乎

(PDF) A closed-form estimator for the GARCH(1,1)-model

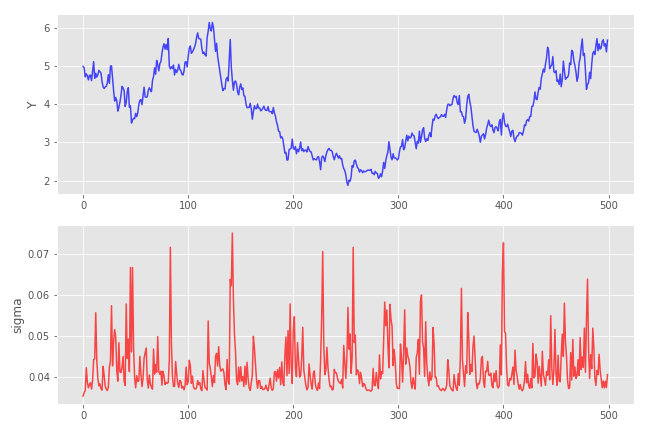

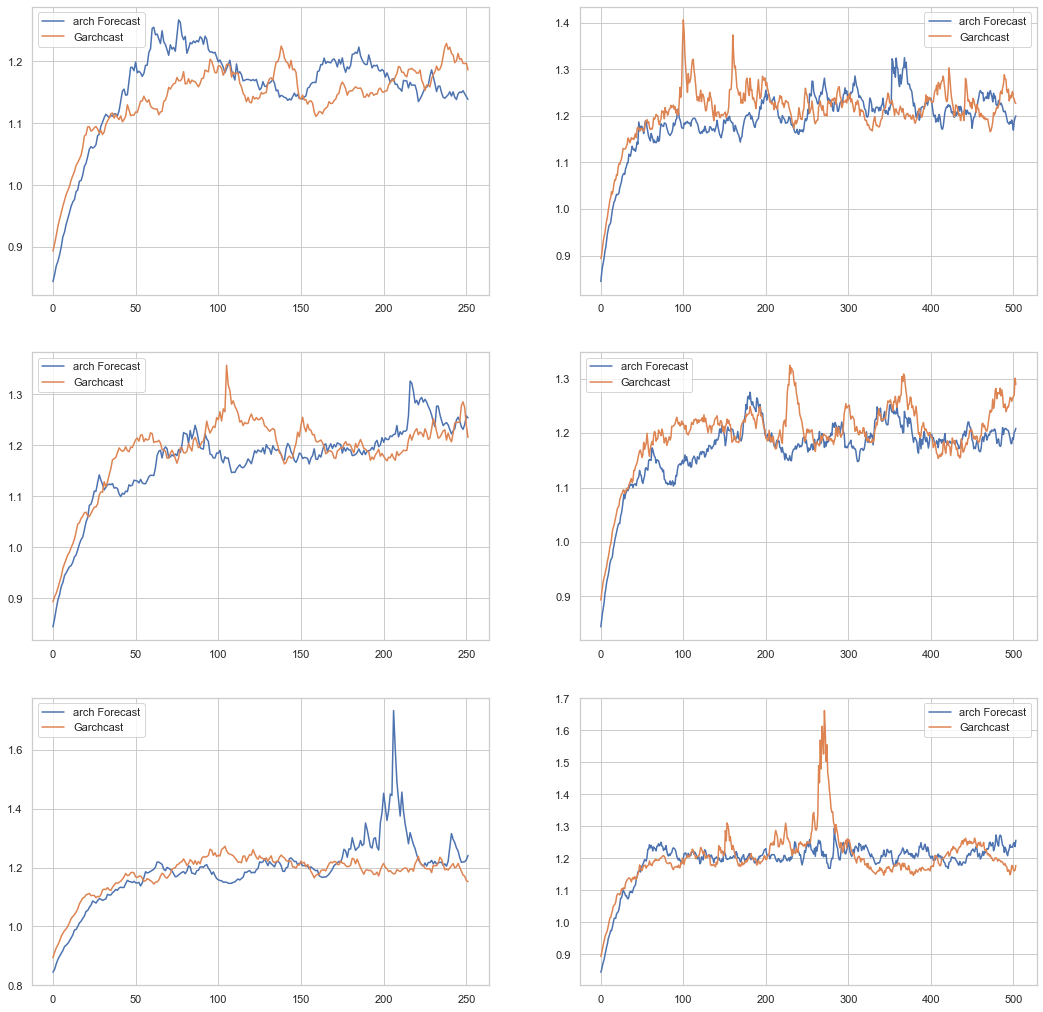

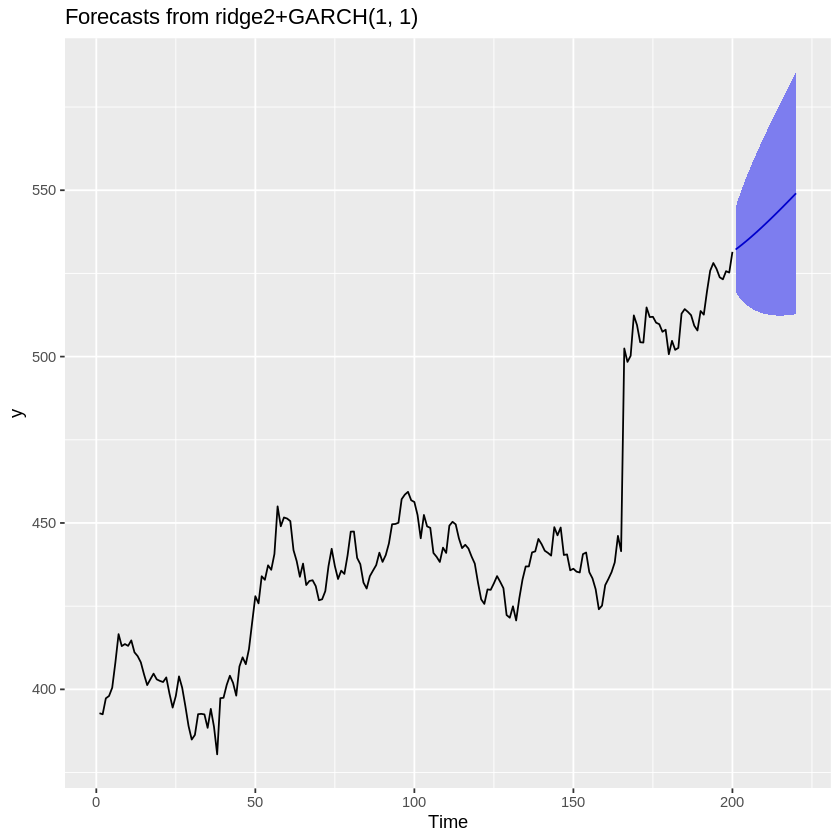

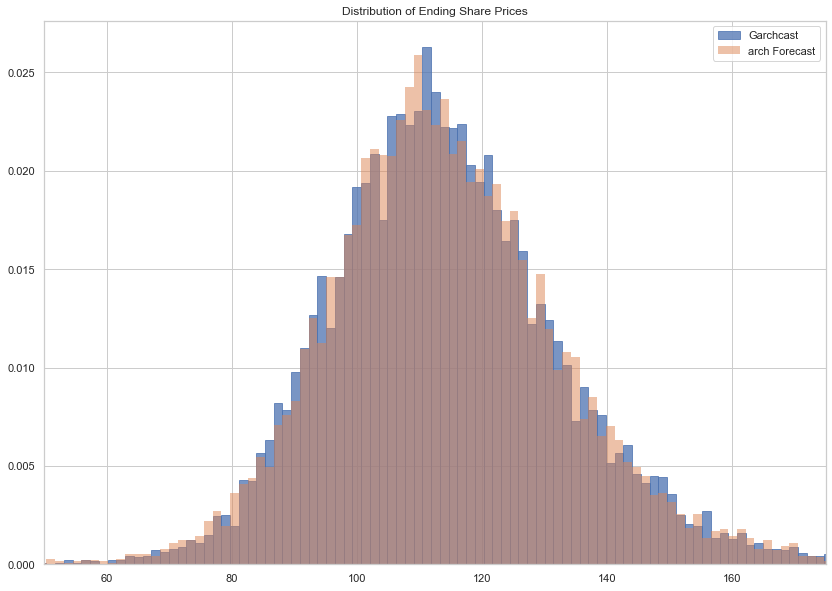

Combining any model with GARCH(1,1) for probabilistic stock forecasting

(PDF) Comparative Analysis of Bilinear Time Series Models with Time ...

GARCH模型-零基础入门教程

(PDF) Properties and estimation of GARCH(1,1) model