Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

PPT - GREAT SALT LAKE SURFACE LEVEL FORECASTING USING FIGARCH MODELING ...

FIGARCH model can be expressed as: ) , , ( q d p | Download Scientific ...

Parameter estimation of GARCH and FIGARCH model GARCH for Volume ...

The outcome of FIGARCH for the daily returns of NSE. | Download ...

MSHG results of FIGARCH and FARIMA | Download Scientific Diagram

Measures of performance of TV-HGARCH, HGARCH and FIGARCH models on S &P ...

Figure 1 from Modeling volatility with time-varying FIGARCH models ...

FIGARCH Models: Stationarity, Estimation Methods and The Identification ...

Estimations of an FIGARCH model | Download Table

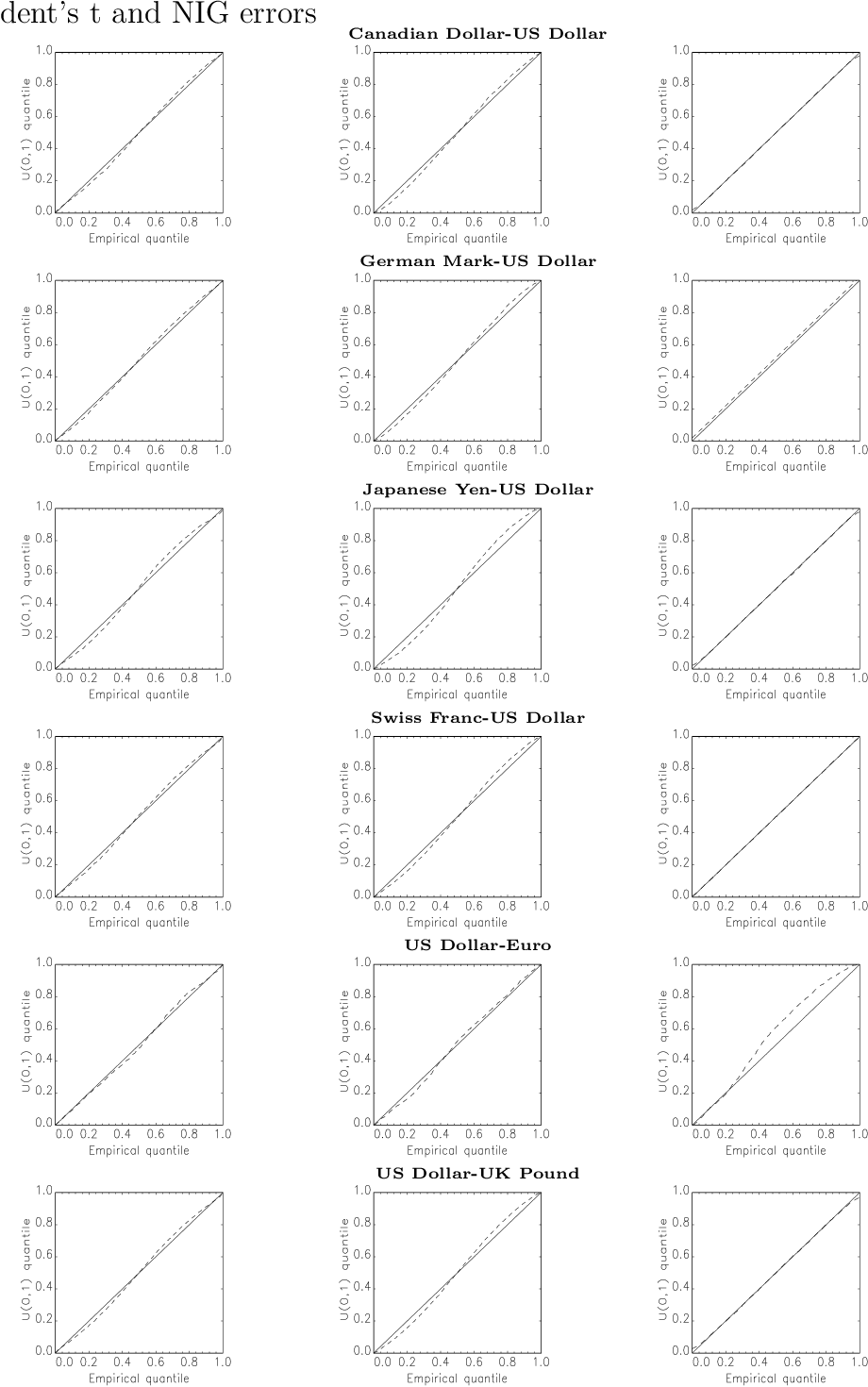

Estimated FIGARCH models with t and NIG distributions for the three ...

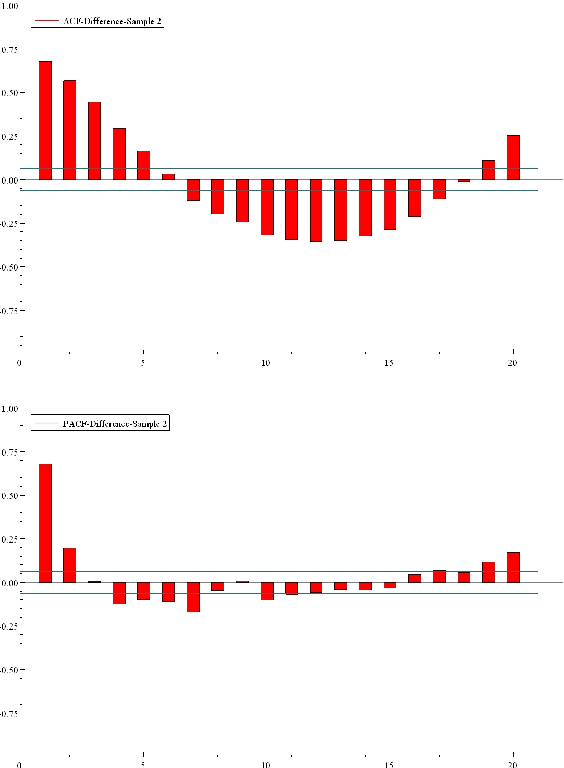

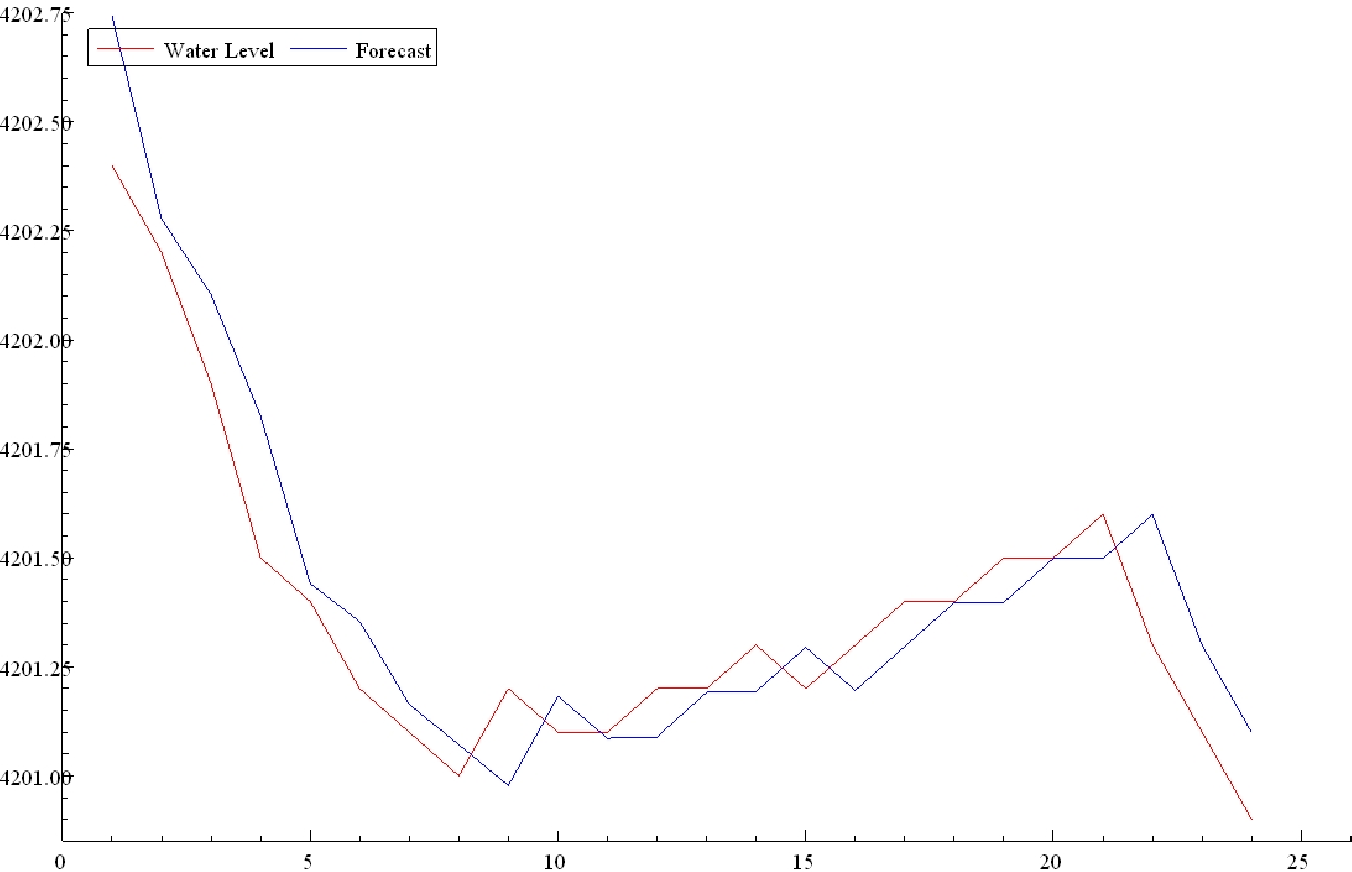

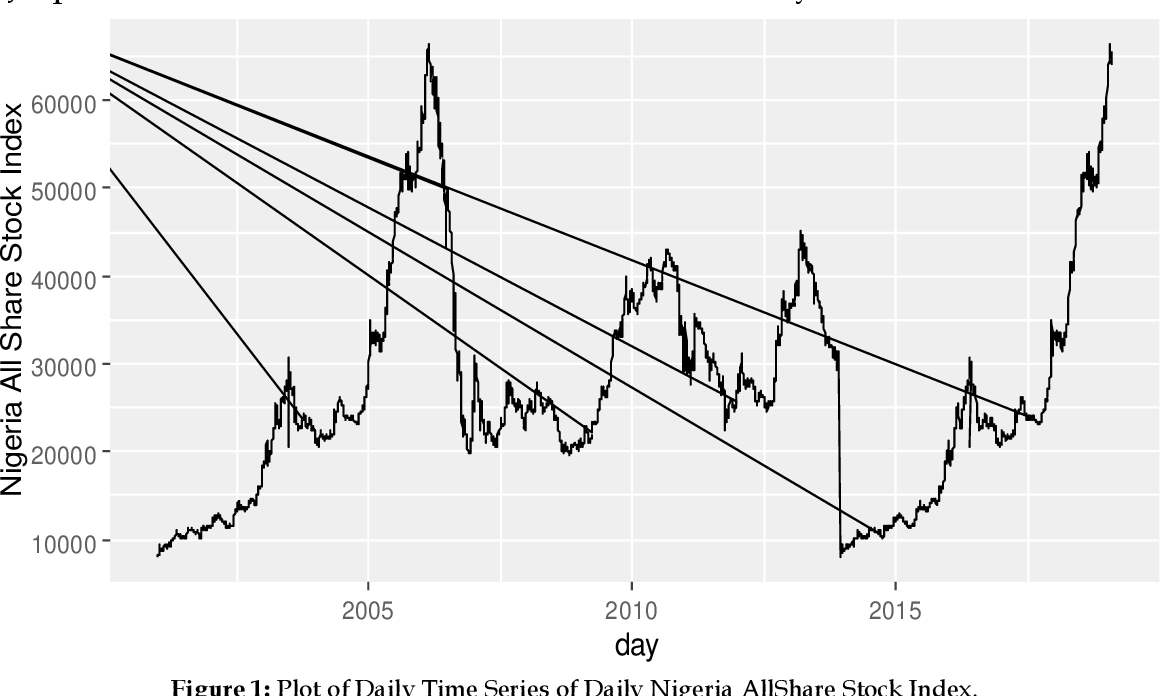

Figure 5 from Great Salt Lake Surface Level Forecasting Using FIGARCH ...

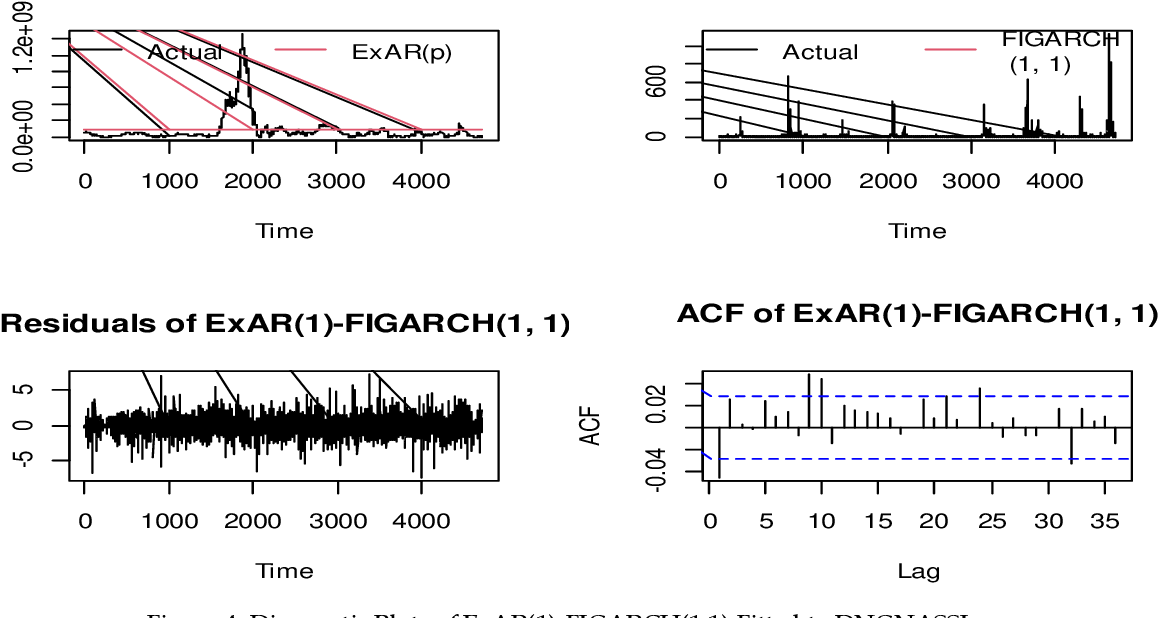

Figure 3 from Great Salt Lake Surface Level Forecasting Using FIGARCH ...

Figure 8 from Great Salt Lake Surface Level Forecasting Using FIGARCH ...

FIGARCH (1.1) parameters of the log returns of the original series ...

Quantile predictions VaR for FIGARCH models and Lijung-Box test for ...

FigArch (1,d,1): t-distribution and normal distribution | Download Table

FIGARCH (1, d, 1) parameters with and without dummy variables for ...

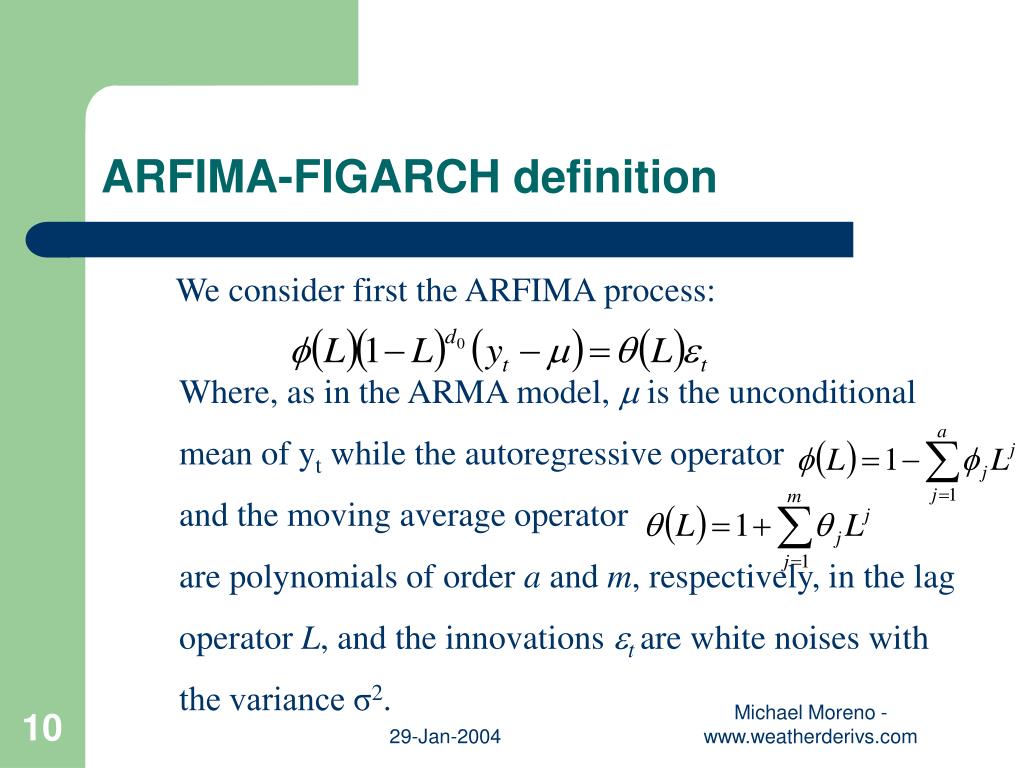

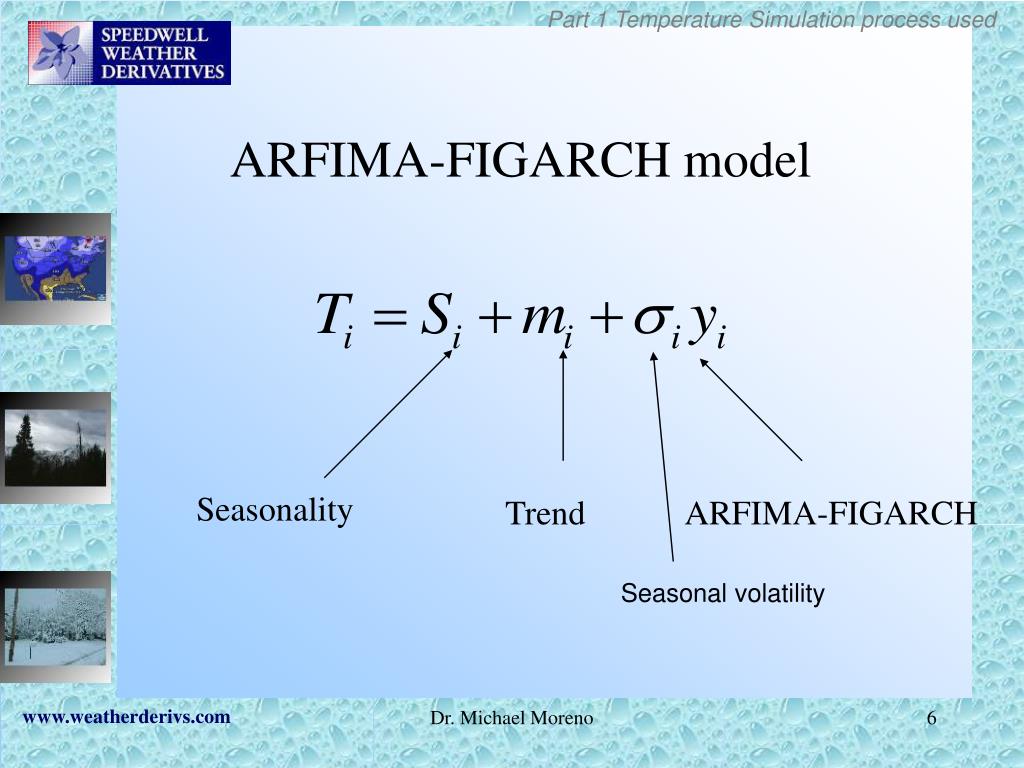

(PDF) An overview of FIGARCH and related time series models

Estimates of the GARCH, CGARCH and FIGARCH models for crude oil returns ...

FIGARCH model estimation results | Download Scientific Diagram

The Results of FIGARCH and FIAPARCH Models | Download Table

d and H values for BECI UB, LB and Average- FIGARCH method. | Download ...

The Results of FIGARCH Model | Download Table

FIGARCH modellemesi aşamasına geçilmiştir. Tüm veri kümeleri için ...

Rolling Window FIGARCH Forecast - File Exchange - MATLAB Central

(PDF) The effects of aggregation on FIGARCH variances

(PDF) DEVELOPING THE HYBRID ARIMA- FIGARCH MODEL FOR TIME SERIES ANALYSIS

(PDF) A Note on the Asymptotic Inference for FIGARCH (p, d, q) Models

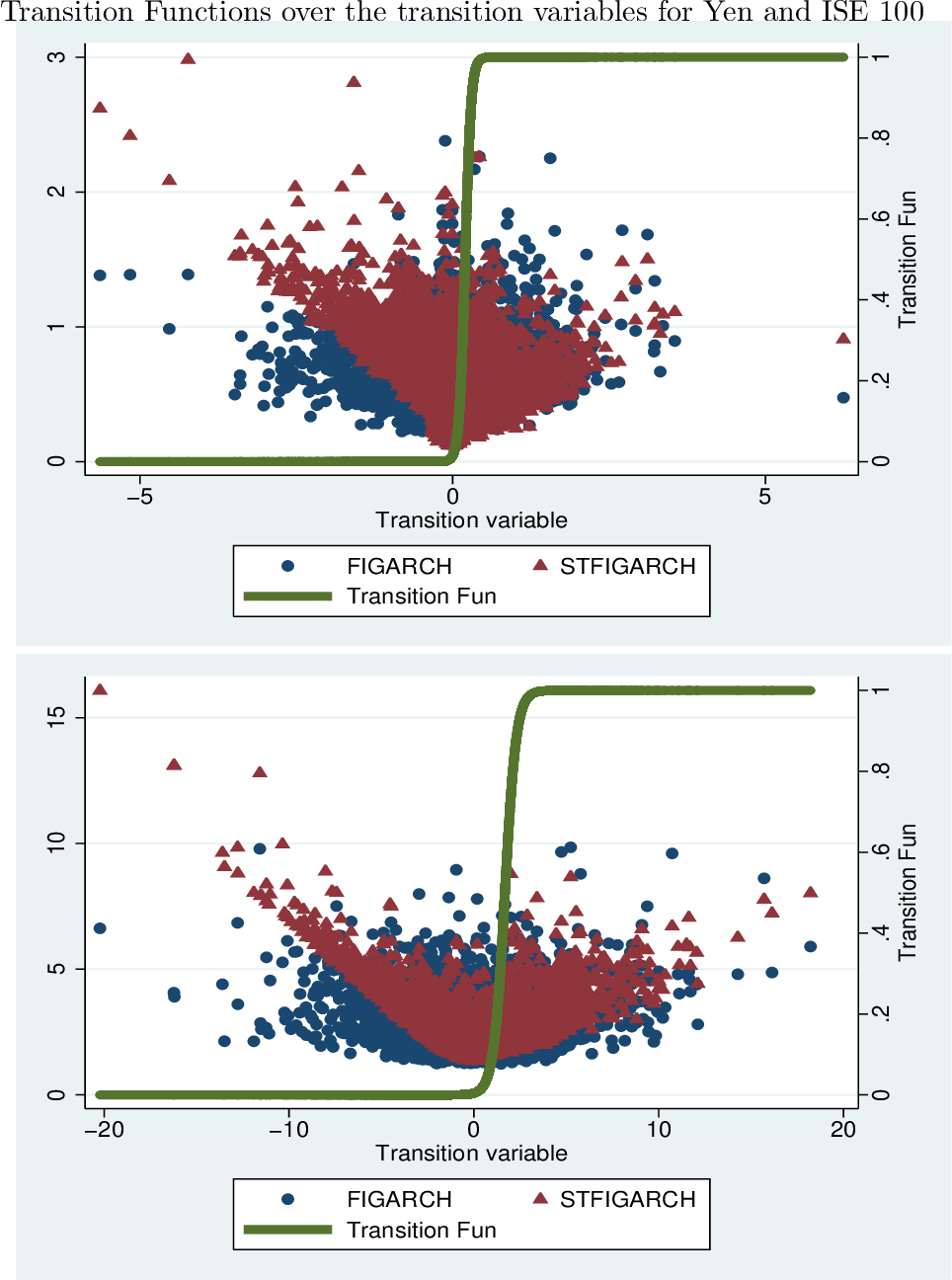

A Smooth Transition FIGARCH Model

FIGARCH models and ARFIMA-FIAPARCH models confirmed this finding for ...

Table 1 from Modeling volatility with time-varying FIGARCH models ...

(PDF) Stochastic equilibrium of free trade under a FIGARCH volatility

Copula estimates of return-volume dependence with GARCH and FIGARCH ...

Table 1 from Bivariate Error Correction FIGARCH and FIAPARCH Models on ...

Maximum likelihood estimation of FIGARCH processes | Download Table

Estimates of d in the FIGARCH model. | Download Table

BDS test of residuals of FIGARCH and FIEGARCH model | Download Table

Figure 1 from DEVELOPING THE HYBRID ARIMA- FIGARCH MODEL FOR TIME ...

(PDF) Analytic Hessian matrices and the computation of FIGARCH estimates

Estimation results of FIGARCH models | Download Table

Maximal Lyapunov Exponent result for FIGARCH d=0.90. | Download ...

FIGARCH (1, d, 1) QMLE estimates (10.2009-03.2012) | Download Table

Table 2 from DEVELOPING THE HYBRID ARIMA- FIGARCH MODEL FOR TIME SERIES ...

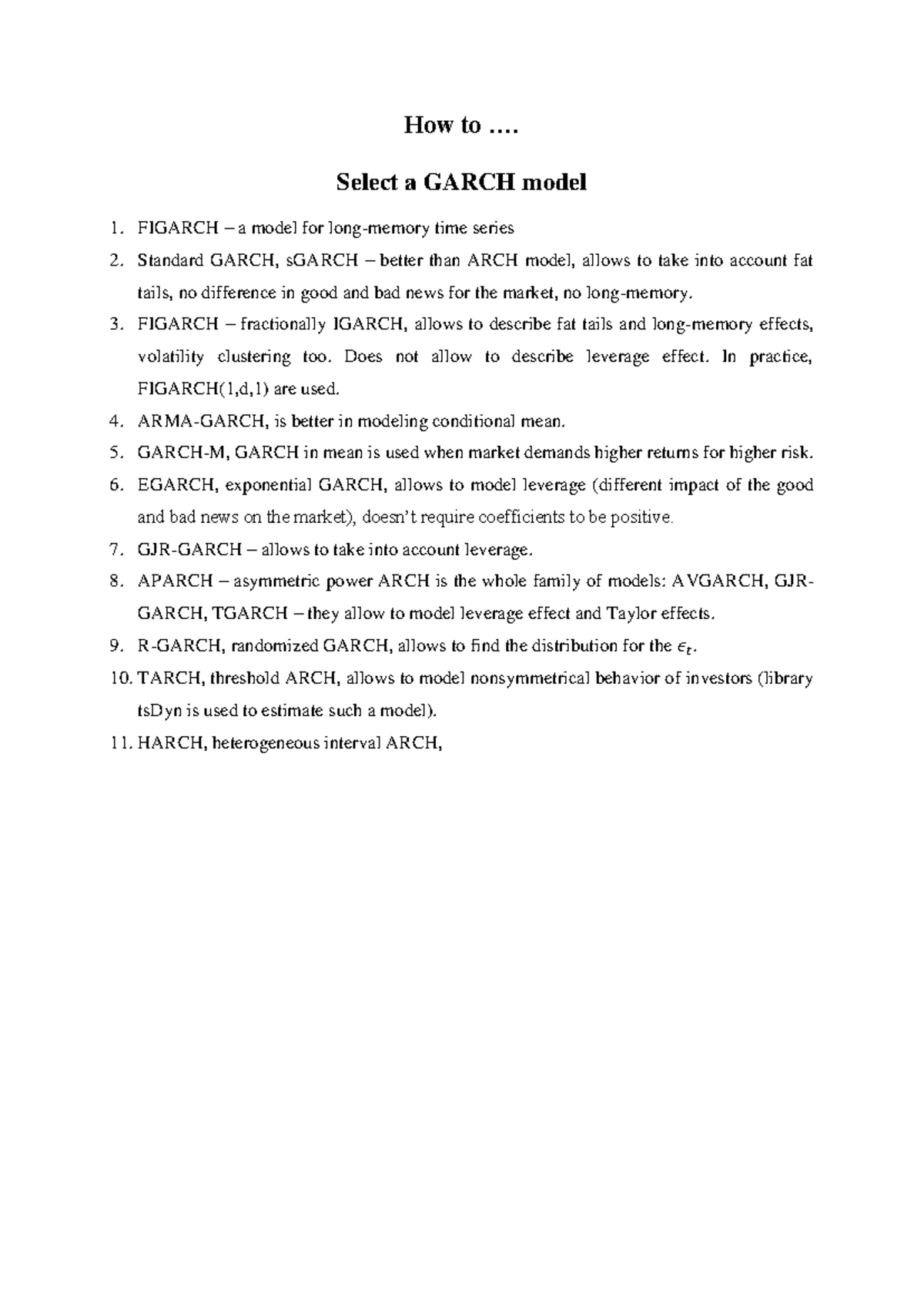

Garch models - How to .... Select a GARCH model FIGARCH – a model for ...

PPT - 人工智慧演算法於時間序列模型之整合 PowerPoint Presentation - ID:3463947

Figure 4 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

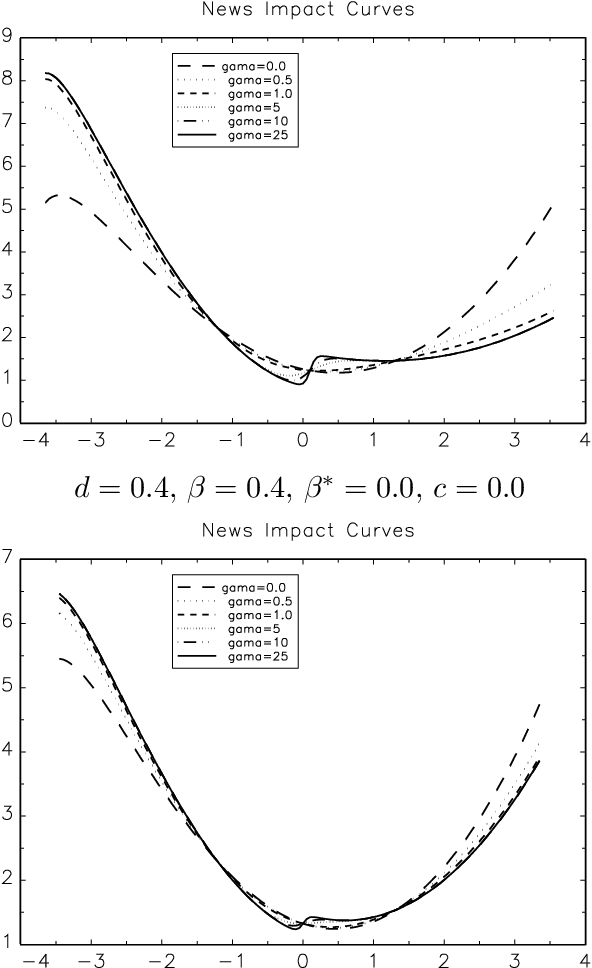

Figure 2 from Long memory and nonlinearity in conditional variances: A ...

Selected FIGARCH-calculated dynamic correlations between WTI volatility ...

Figure S19: For Ethereum, fluctuation test comparing the 5% VaR and ES ...

Figure S20: For Ethereum, fluctuation test comparing the 5% VaR and ES ...

339 Estimation of |ARCH| |GARCH| |TARCH |PARCH| |FIGARCH| and |FIEGARCH ...

Conditional variances of the univariate FIGARCH(1,d,1) model | Download ...

FIGARCH-calculated conditional correlation by sector, daily data (1 ...

Eviews软件教程--New GARCH, including FIGARCH, in EViews 12 P1 Eviews软件教程 ...

(PDF) Investigating Volatility Dynamics of the Portugal Stock Market ...

Conditional covariances of the fourvariate FIGARCH(1,d,1)-cDCC model ...

Table 7 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

Figure 1 from Modelling High-Frequency Volatility with Three-State ...

Figure 3 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

Estimation results (in-sample simulation data) of FIGARCH(1,d,1) model ...

Figure 2 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

Estimation results and diagnostic tests for FIGARCH, HYGARCH and ...

Conditional covariances of the bivariate FIGARCH(1,d,1)-cDCC model ...

Table 2 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

Quantification of the stock market value at risk by using FIAPARCH ...

Dynamic Conditional Correlations of the Fourvariate FIGARCH(1,d,1)-cDCC ...

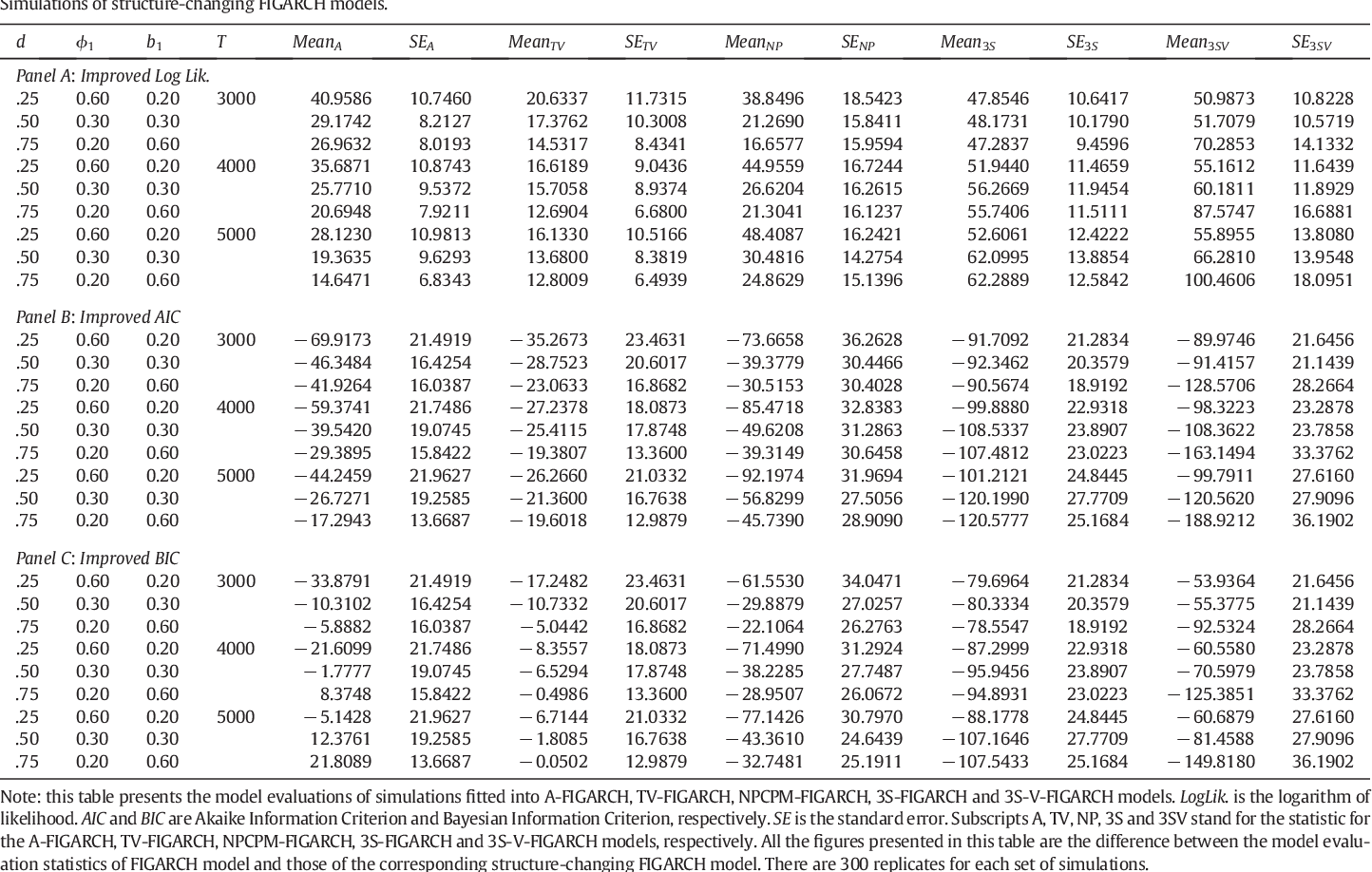

Summary of Simulated Results of the ARIMA-FIGARCH model. | Download ...

Estimation Results of the ARFIMA-FIGARCH Type Models for Turkey ...

Full sample parameter estimates of the FIGARCH-skT model, for the 10 ...

Conditional variances of the univariate AR(1)-FIGARCH(1,d,1) model ...

Figure 1 from Modeling Long Memory and Structural Breaks in Conditional ...

Cryptocurrencies' volatility structure (FIGARCH estimation) | Download ...

Figure 2 from Modeling Long Memory and Structural Breaks in Conditional ...

Conditional covariances of the fourvariate AR(1)-FIGARCH(1,d,1)-cDCC ...

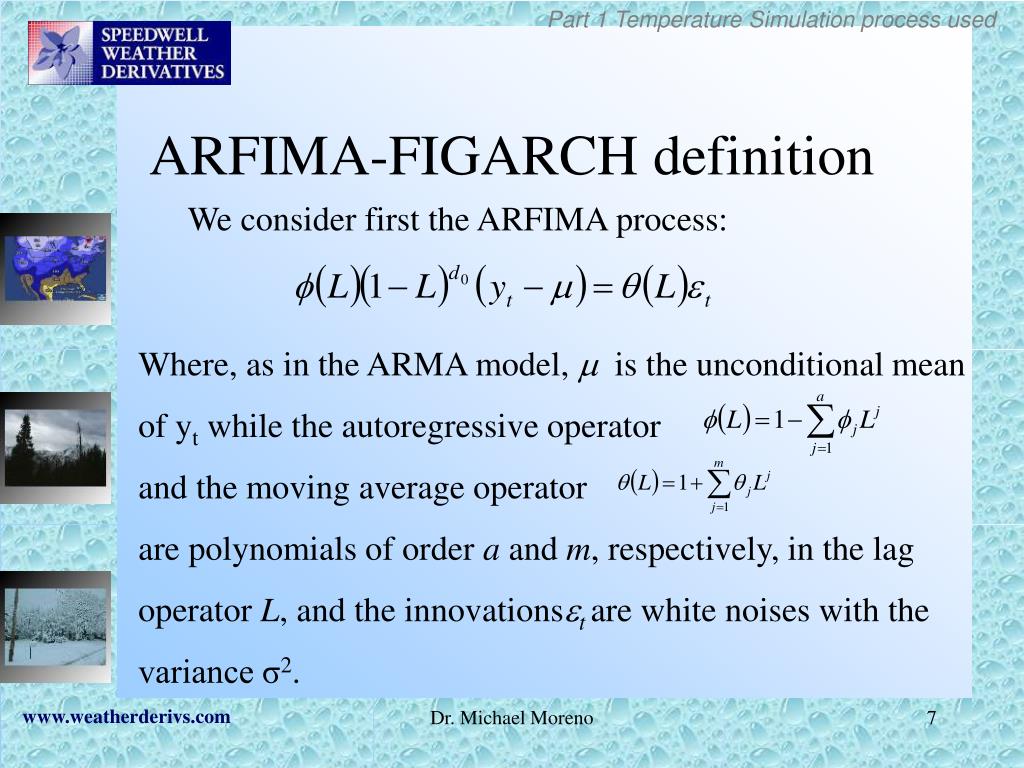

PPT - Weather Derivatives Trading and Structuring The Forecast ...

PPT - Weather derivative hedging & Swap illiquidity PowerPoint ...

Figure 1 from Modeling high-frequency volatility with three-state ...

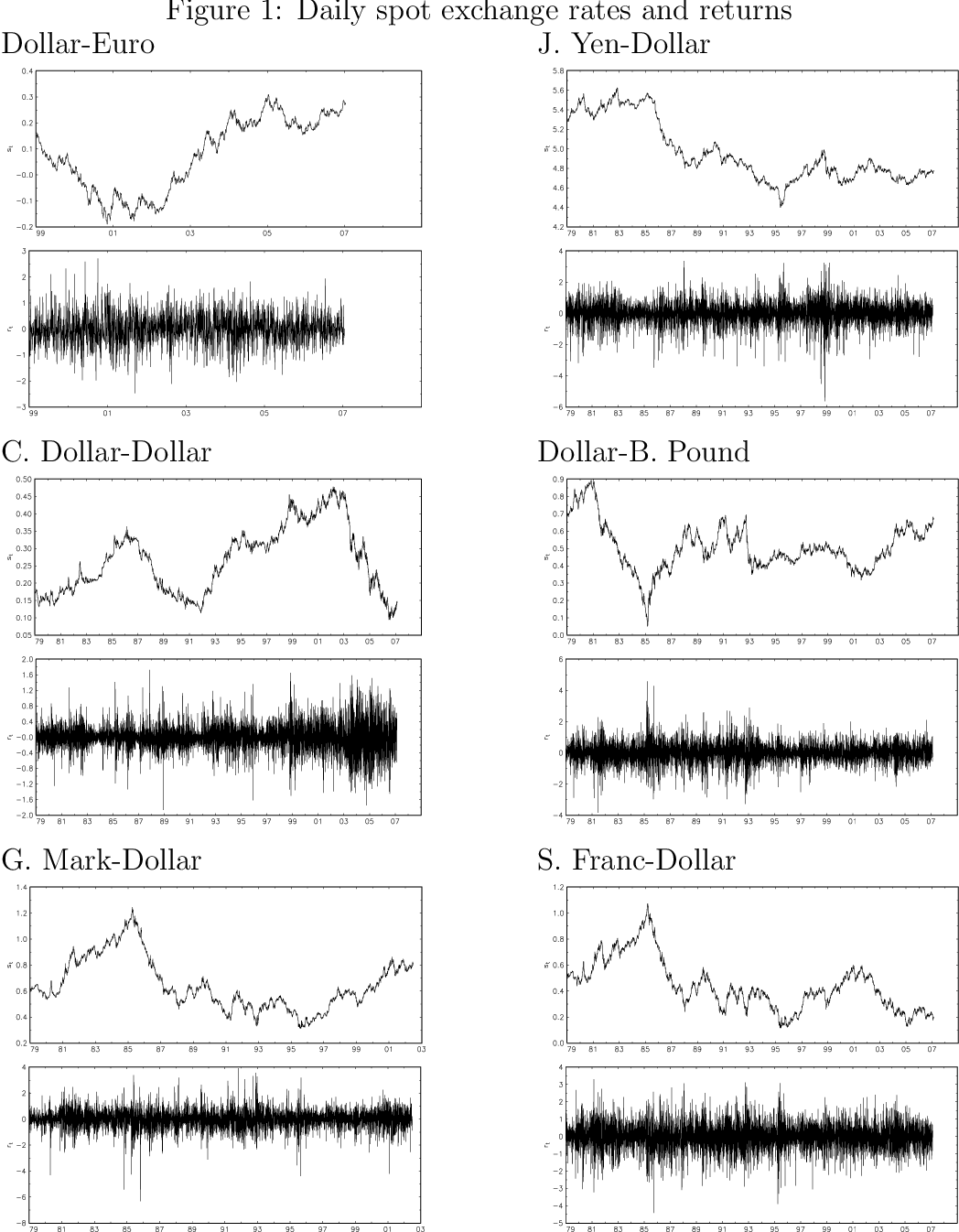

Figure 1 from Conditional Volatility and Distribution of Exchange Rates ...

Block Trading Based Volatility Forecasting: An Application of VACD ...

(PDF) n ° 14 The Impact of Foreign Exchange Interventions: New Evidence ...

Estimation of FIGARCH-M processes (mean equation) | Download Table

Estimated ARFIMA-FIGARCH model | Download Scientific Diagram

ARCH/GARCH or FIARCH/FIGARCH test | Download Scientific Diagram

Table 1 from Modeling high-frequency volatility with three-state ...

Figure 1 from Long memory and nonlinearity in conditional variances: A ...

Table 4 from Developing Exp-FIGARCH Hybrid Models for Time Series ...

Estimated MA-FIGARCH model for Filtered High Frequency Futures Returns ...

(PDF) Estimating the Value-at-Risk for some stocks at the capital ...

Estimation results of the ARFIMA-FIGARCH model. | Download Scientific ...

Estimates of the applications of long memory (FIGARCH) models in ...

DCC-FIGARCH (1,1) parameter estimation results for the relationship ...

Asymmetry and Persistence of Energy Price Volatility