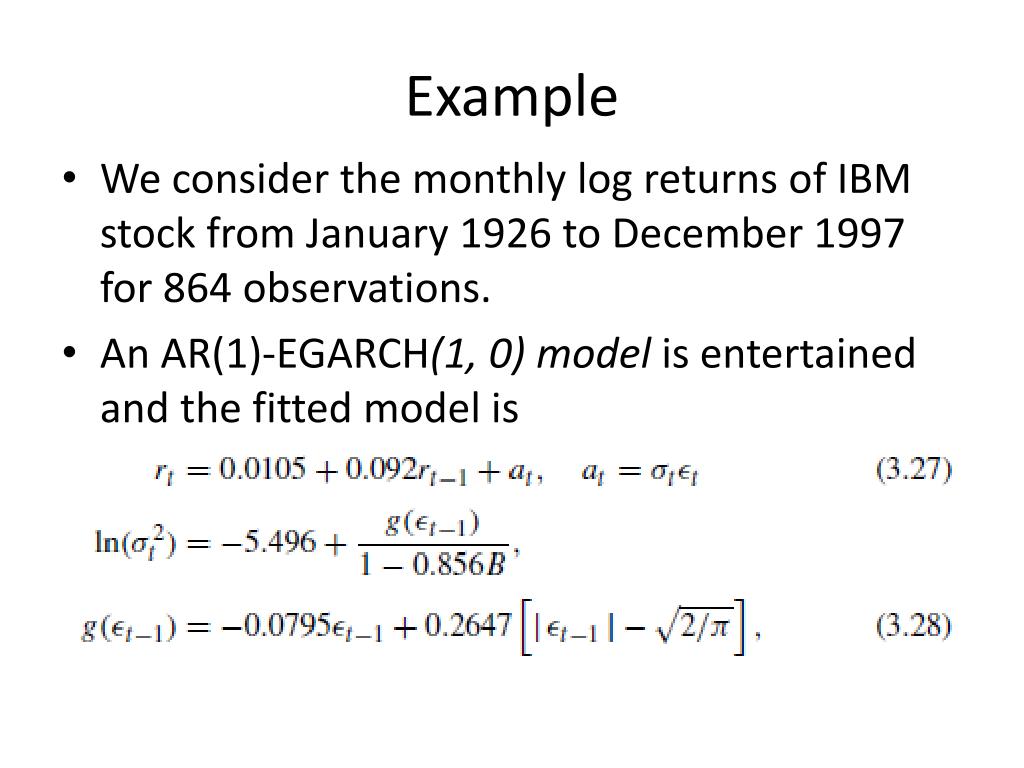

Showing 119 of 119on this page. Filters & sort apply to loaded results; URL updates for sharing.119 of 119 on this page

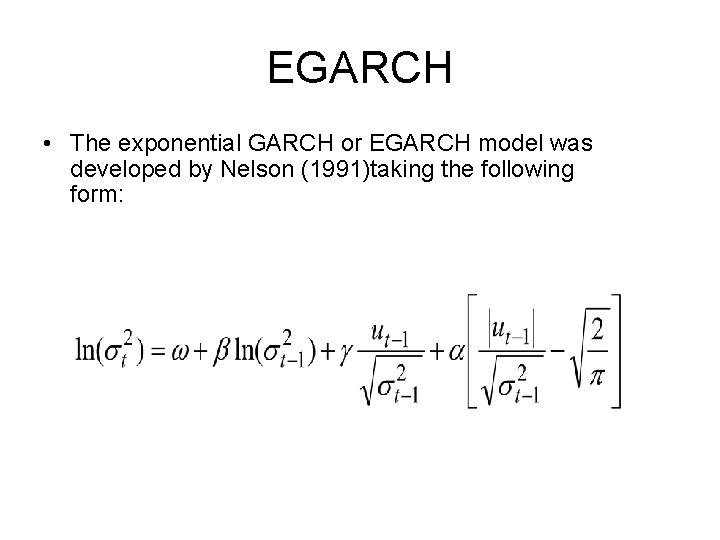

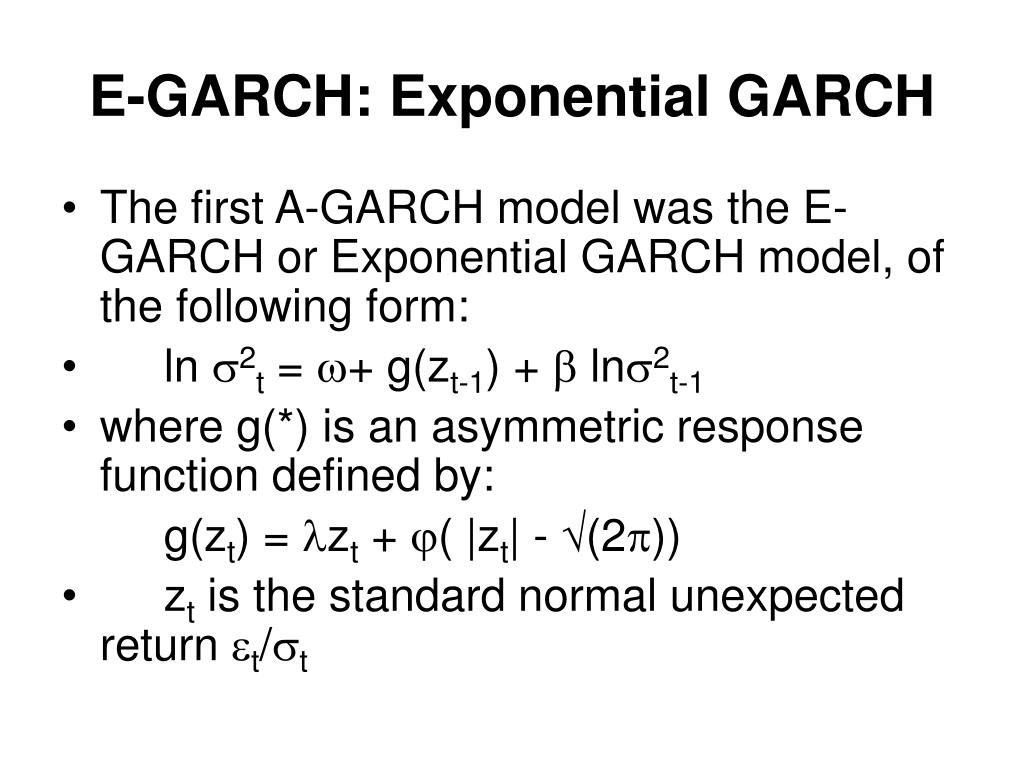

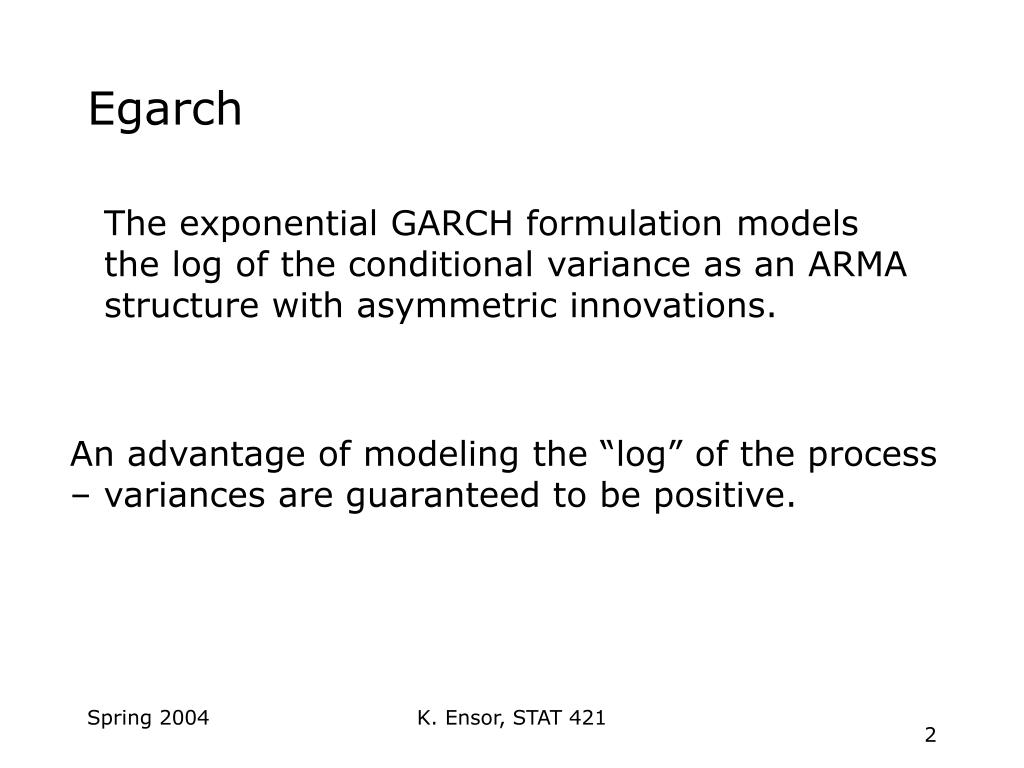

PPT - THE EXPONENTIAL GARCH MODEL PowerPoint Presentation, free ...

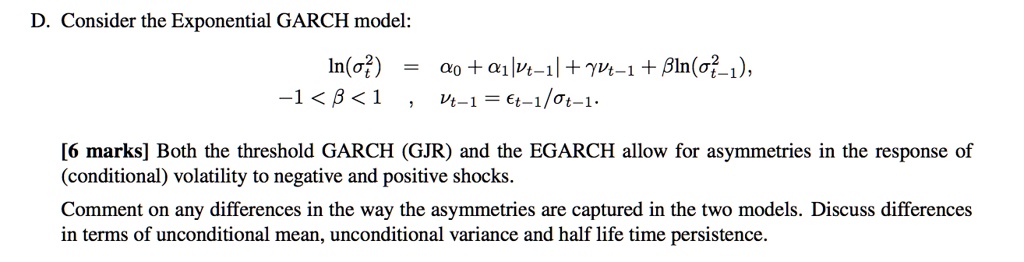

SOLVED: Consider the Exponential GARCH model: -1

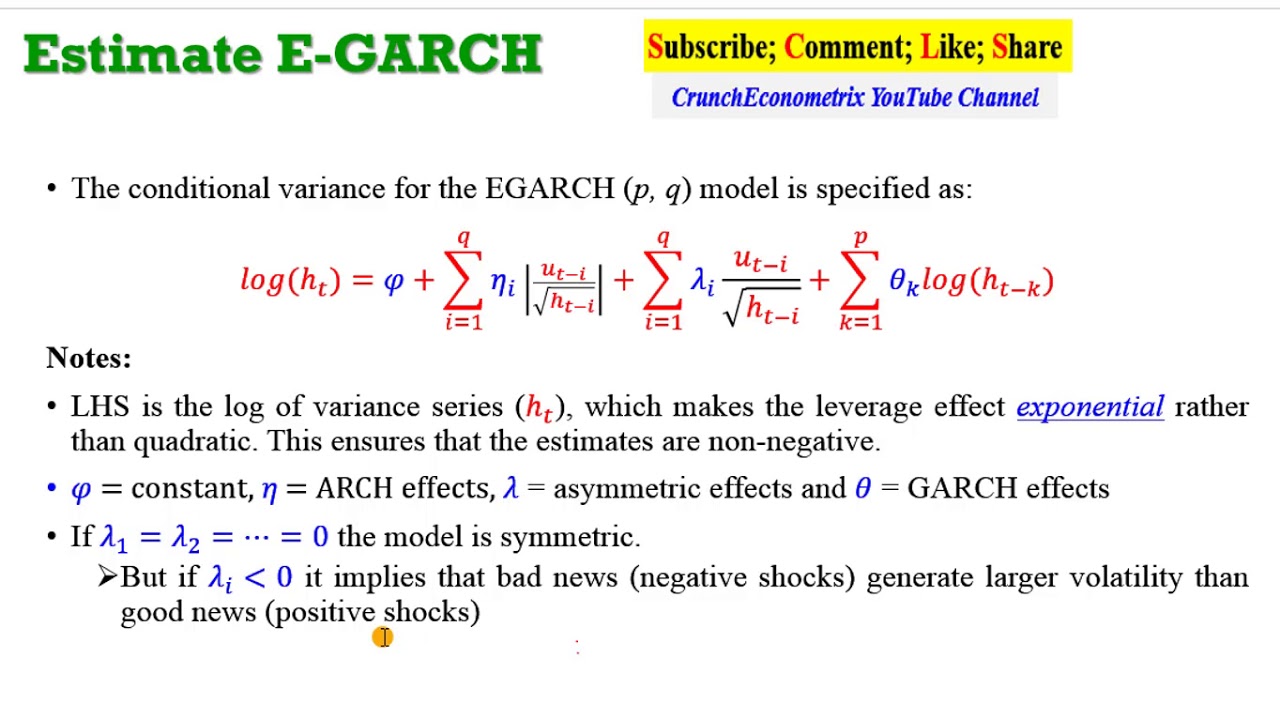

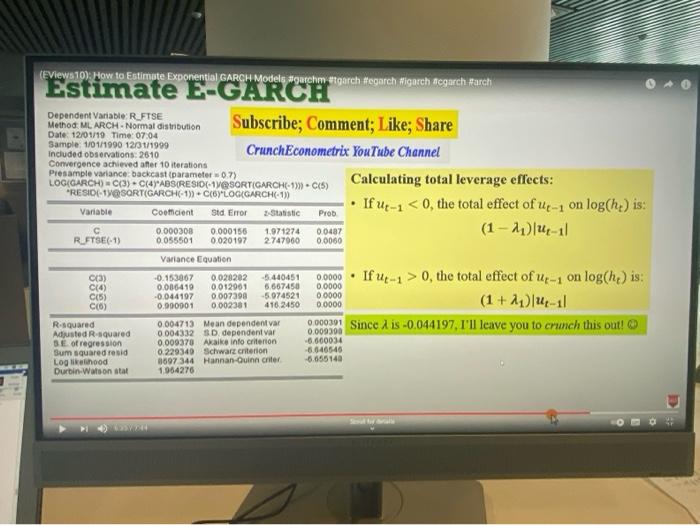

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch # ...

Figure 1 from Gaussian and Exponential GARCH models | Semantic Scholar

Solved Problem 4. (EGARCH(1,1) model)The exponential GARCH | Chegg.com

(EViews 10). How to Estimate Exponential GARCH Models | Chegg.com

Estimated Exponential GARCH (EGARCH) Model | Download Scientific Diagram

Table 3 from Evaluating exponential GARCH models | Semantic Scholar

Exponential GARCH results for interbank market volatility analysis ...

Bi-Variate Exponential Garch Coefficient With Dummy Variable | Download ...

Figure 2 from Gaussian and Exponential GARCH models | Semantic Scholar

Coefficients of BI-VARIATE Exponential GARCH | Download Scientific Diagram

Table 1 from Evaluating exponential GARCH models | Semantic Scholar

(PDF) Exponential GARCH Modelling of the Inflation-Inflation ...

Estimated Exponential GARCH -Mean Results | Download Table

Exponential GARCH Model with Exogenous Covariate for South Sudanese ...

(PDF) An exponential continuous-time GARCH process

Exponential GARCH Modelling of the Inflation-Inflation Uncertainty ...

(PDF) Peramalan Volatilitas Saham Menggunakan Model Exponential Garch ...

(PDF) Exponential GARCH Modeling With Realized Measures of Volatility ...

EViews10 How to Estimate Exponential GARCH Models - YouTube

(PDF) Quasi Maximum Exponential Likelihood Estimation of GARCH Model ...

Table 13 from Application of fractional exponential feature to GARCH ...

Figure 20 from Application of fractional exponential feature to GARCH ...

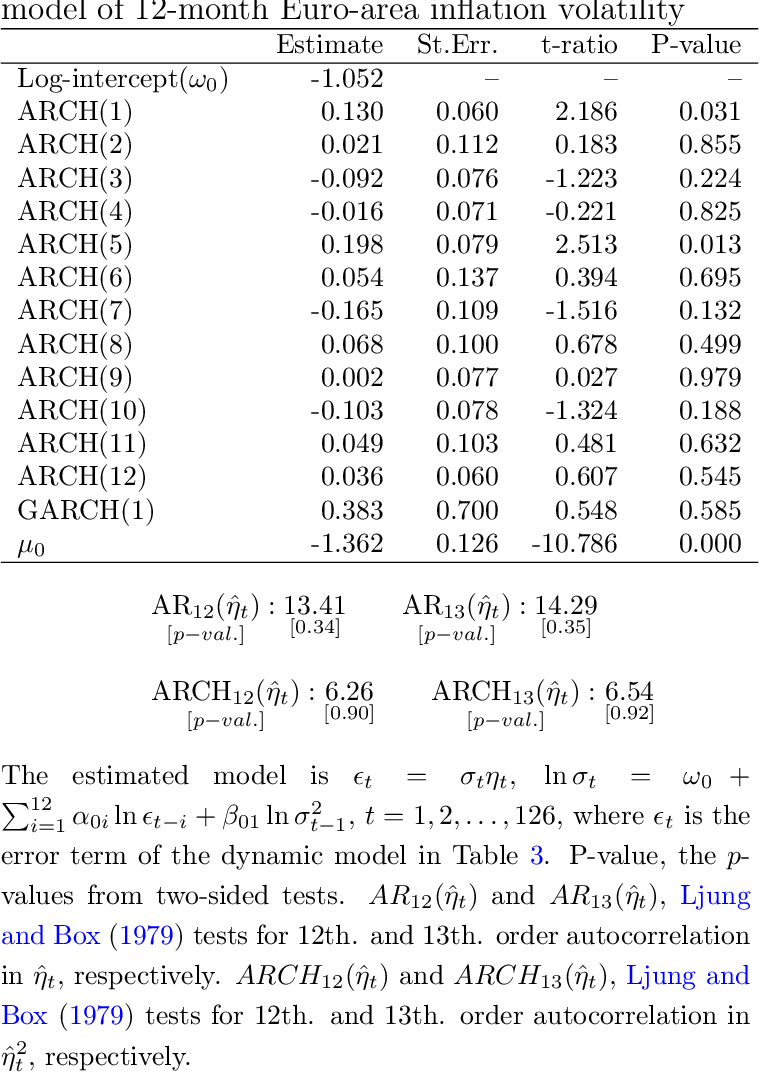

Table 1 from Exponential GARCH Modelling of the Inflation-Inflation ...

Table 2 from Application of fractional exponential feature to GARCH ...

Table 7 from Application of fractional exponential feature to GARCH ...

(PDF) Garch models without positivity constraints: exponential or log ...

Figure 17 from Application of fractional exponential feature to GARCH ...

PENERAPAN MODEL EXPONENTIAL GARCH PADA PERAMALAN DATA SAHAM BLUECHIP DI ...

ANALISIS MODEL THRESHOLD GARCH DAN MODEL EXPONENTIAL GARCH PADA ...

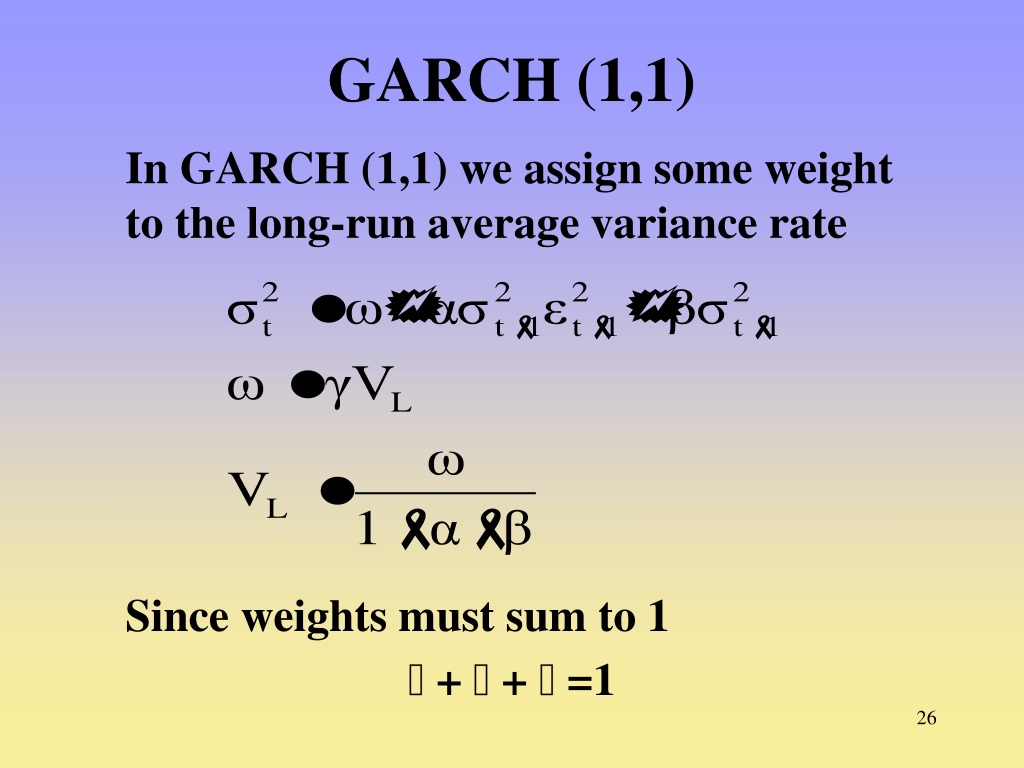

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

GARCH Models and Asymmetric GARCH models VECM Review

PPT - Analisi delle serie storiche: modelli ARCH e GARCH PowerPoint ...

Figure 2 from Global self-weighted and local quasi-maximum exponential ...

(PDF) Exponential GARCH-Ito Volatility Models

(PDF) Exponential-Type GARCH Models With Linear-in-Variance Risk Premium

(PDF) Bayesian Analysis of Realized Matrix-Exponential GARCH Models ...

Bayesian Analysis of Realized Matrix-Exponential GARCH Models | Request PDF

(PDF) Bayesian Analysis of Realized Matrix-Exponential GARCH Models

EGARCH model: exponential asymmetric volatility persistence (Excel ...

(PDF) Modeling Foreign Exchange Rate Pass-Through using the Exponential ...

Table 4 from An Exponential Chi-Squared QMLE for Log-GARCH Models Via ...

(PDF) Dynamical Approach in Studying Stability Condition Of Exponential ...

(PDF) Quasi‐maximum exponential likelihood estimation for double ...

Estimates of exponential ACD, LogACD and Log-ARMA-GARCH models for ...

GARCH vs. GJR-GARCH Models in Python for Volatility Forecasting

Asymmetric Shocks and Pension Fund Volatility: A GARCH Approach with ...

r - How to model a GARCH with explanatory variables in mean and ...

Building a GARCH Volatility Model in Python: A Step-by-Step Tutorial ...

GARCH model estimation, GARCH Model Extensions

(PDF) A Study on Effect of Exponential Smoothing CoefficientValue with ...

What is a GARCH Model?

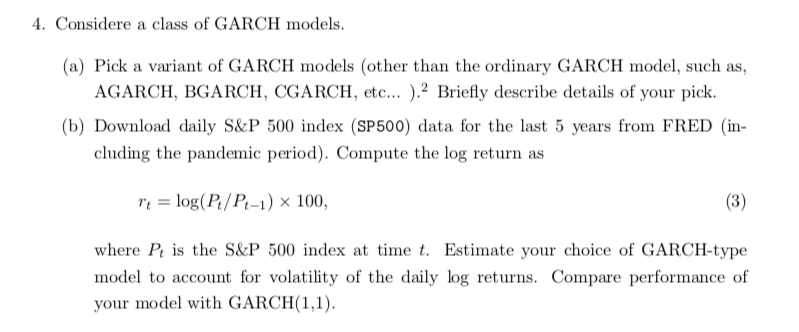

Solved Considere a class of GARCH models. (a) Pick a variant | Chegg.com

(PDF) Global self-weighted and local quasi-maximum exponential ...

Figure 1 from Global self-weighted and local quasi-maximum exponential ...

4.ARCH and GARCH Models.pdf

Frequency of GARCH models used. Source: Authors' calculation ...

Figure 4 from Global self-weighted and local quasi-maximum exponential ...

(PDF) A general framework for spatial GARCH models

PPT - Predicting volatility: a comparative analysis between GARCH ...

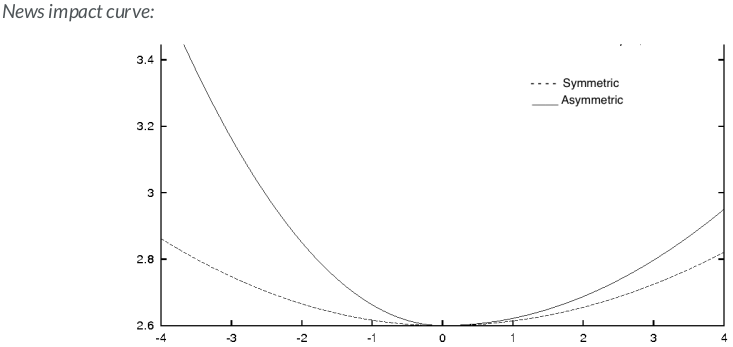

Asymmetric GARCH models, GJR Threshold GARCH model

Understanding Asymmetric GARCH Models in Financial Econometrics ...

Estimated statistics-comparative distribution density GARCH model ...

PPT - Stock Price Modeling for Option Valuation PowerPoint Presentation ...

PPT - Correlation Measures PowerPoint Presentation, free download - ID ...

PPT - Ka-fu Wong University of Hong Kong PowerPoint Presentation, free ...

(PDF) Stock Market Volatility and the COVID-19 Pandemic in Emerging and ...

(PDF) OIL PRICE VOLATILITY AND INFLATION LEVEL IN NIGERIA: AN ...

Stock Market Volatility and Macro Economic Variables Volatility in ...

PPT - Leveraging PowerPoint Presentation, free download - ID:657831

Determining the return volatility of the Ghana stock exchange before ...

(PDF) Exchange Rate and Interest Rate Exposure of UK Industries Using ...

Estimation results of GJR-GARCH and EGARCH models with contemporaneous ...

【上财课程作业】基于GARCH、TARCH和EGARCH的中国平安股价波动分析与预测 - 知乎

Figure 1 from Modeling and Forecasting Stock Market Volatility by ...

Figure 1 from Time series forecasting using functional partial least ...

GitHub - DavidAlexanderMoe/Financial-Time-Series-Analysis-and ...

Chapter 14 - ARCH-GARCH Models | PDF | Coefficient Of Determination ...

Full article: Return and volatility spillovers in equity markets: An ...

PPT - VOLATILITY MODELS PowerPoint Presentation, free download - ID:6789600

20 GARCH模型 | 金融时间序列分析讲义

Time Series Analysis - 6 Generalized Autoregressive Conditional ...

Module 8 - Forecasting – Help center

PPT - Volatility PowerPoint Presentation, free download - ID:9413319

Conditional variance of inflation rate | Download Table

ARCH_GARCH Volatility Forecasting

Option pricing performances and VIX predictability (see section 5.3) of ...

Time series plot of GSE-CI. Source: Authors’ estimation | Download ...

Statistical Analysis on the Impact of Macroeconomic Variables on Stock ...

GitHub - KinH8/Realized-GARCH: Incorporating a realized measure of ...

Sarveshwar Inani's Blog

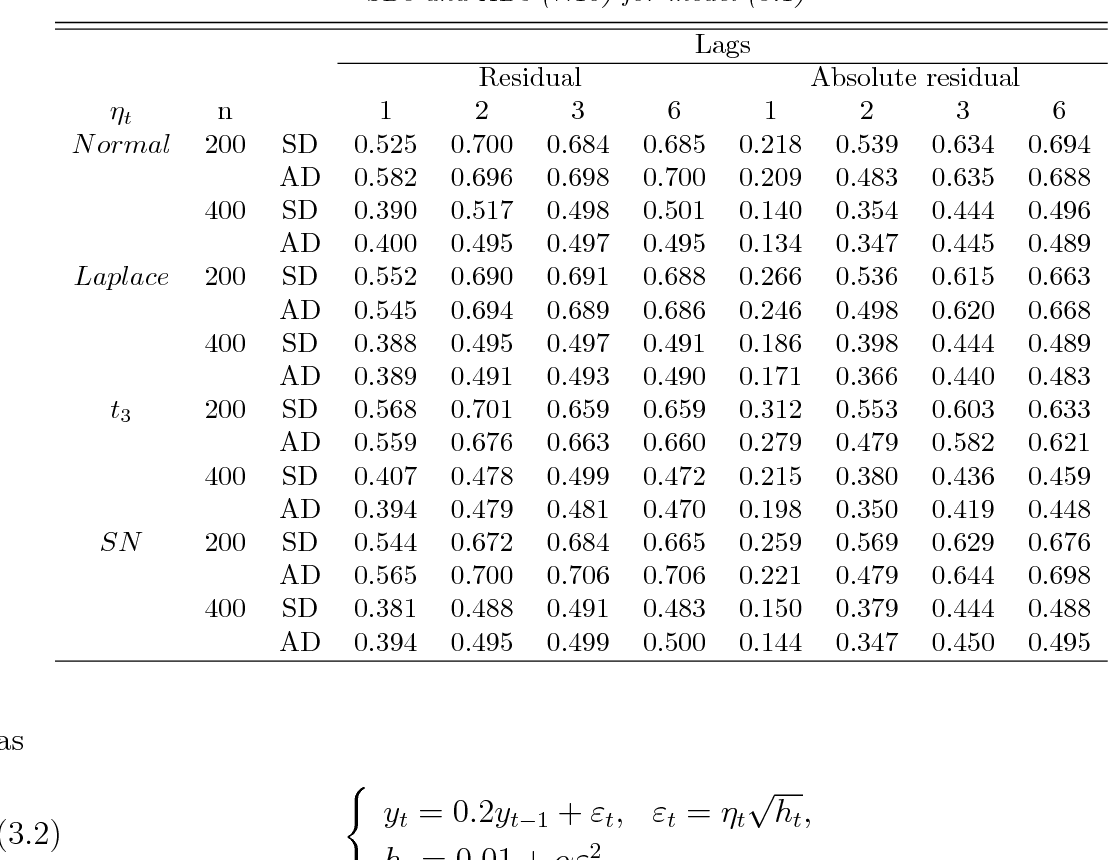

Table 1 from A mixed portmanteau test for ARMA-GARCH model by the quasi ...

PPT - Introduction to Volatility Models PowerPoint Presentation, free ...

Mastering R for Quantitative Finance

PPT - HKUST CSE Dept. PowerPoint Presentation, free download - ID:3288908

【2025】最强总结!十大时间序列模型 !!-CSDN博客