Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

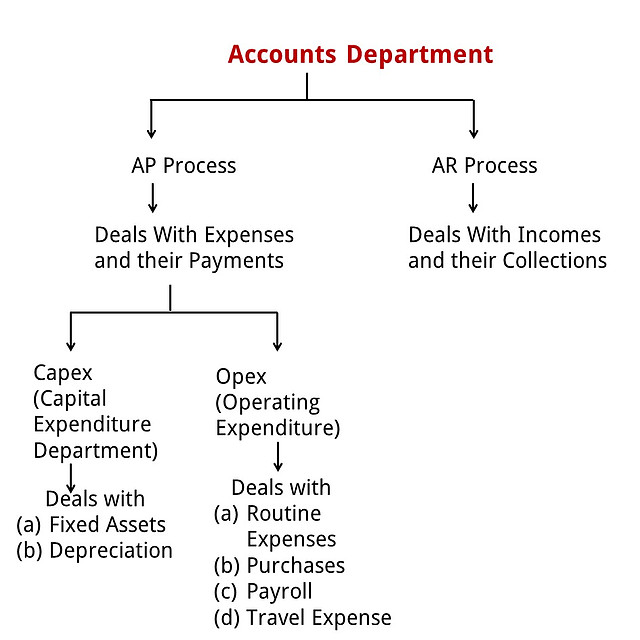

Example of AR Process in Companies - AR Process (O2R Process)

AR Process Flow | PDF

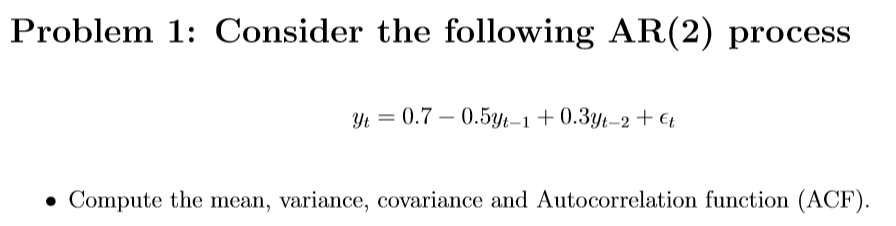

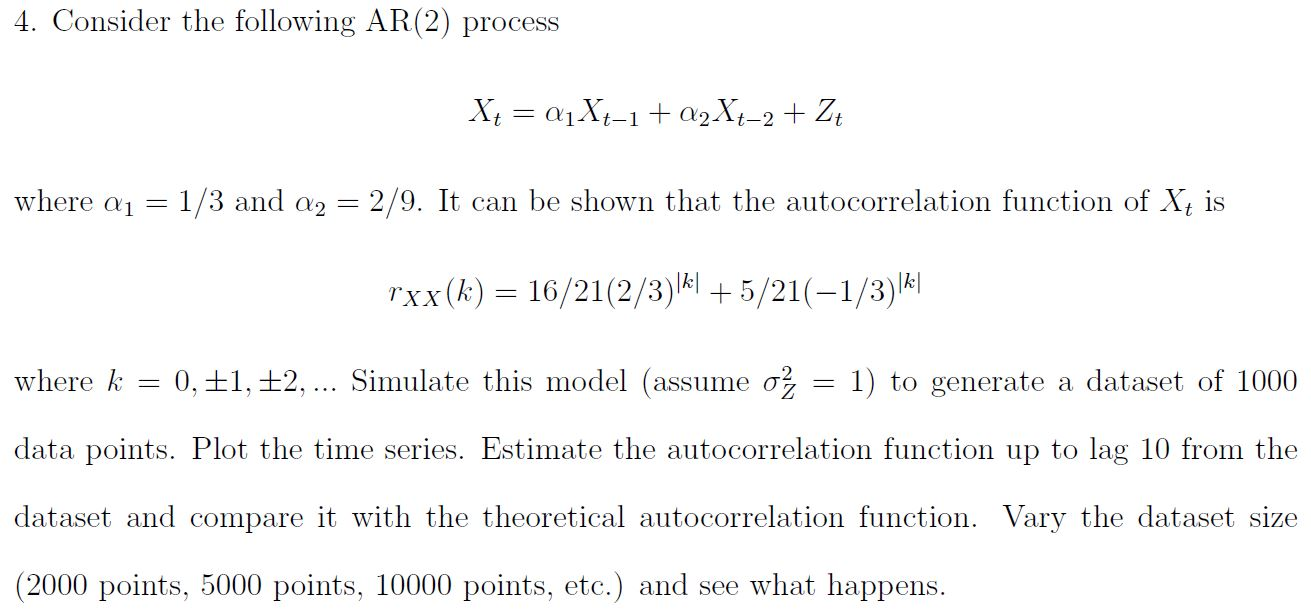

Solved Problem 1: Consider the following AR (2) process | Chegg.com

AR Process Flow Chart | PDF

Stationarity of AR (2) process - YouTube

AR Process Ppt PowerPoint Presentation Complete With Slides

What is AR Process - AR Process (O2R Process)

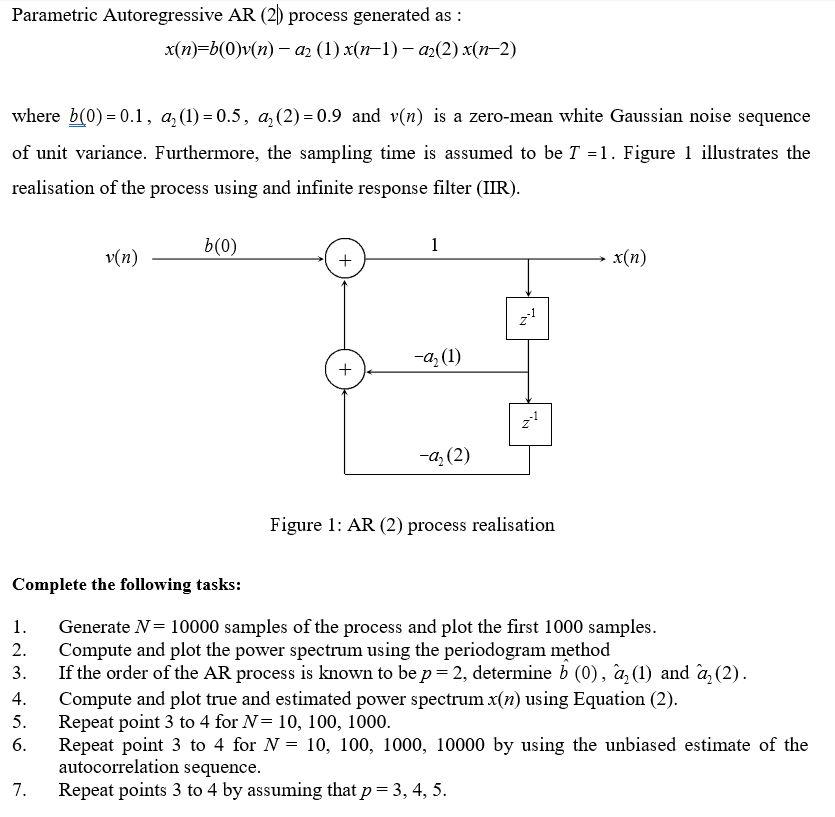

Parametric Autoregressive AR (2) process generated as | Chegg.com

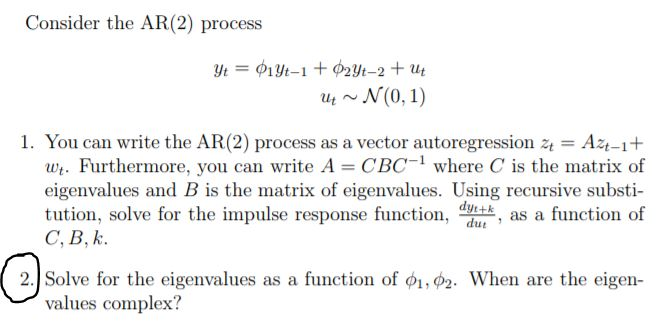

Consider the AR (2) process uN(0, 1) 1. You can write | Chegg.com

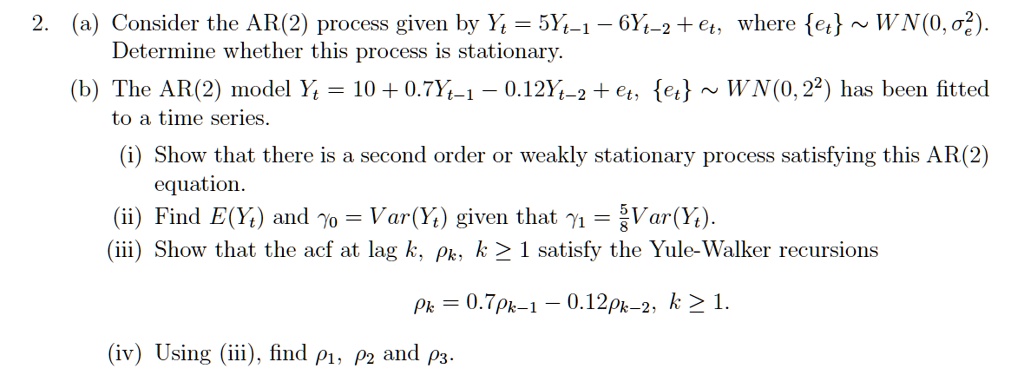

Consider the ar2 process given by yt syt 1 6yt 2 et where et...

AR Payments Data Flow Process | Oracle Experience Blog

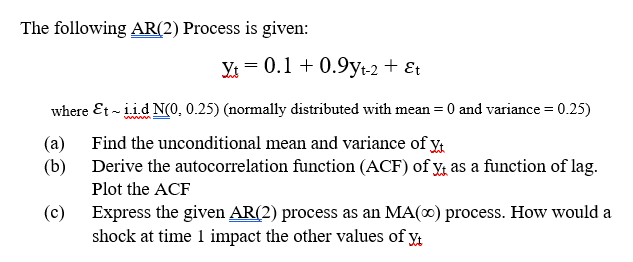

Solved The following AR(2) Process is given: y = 0.1 | Chegg.com

Solved Consider the AR(2) process | Chegg.com

Time Series Analysis - ARIMA models - AR(2) process

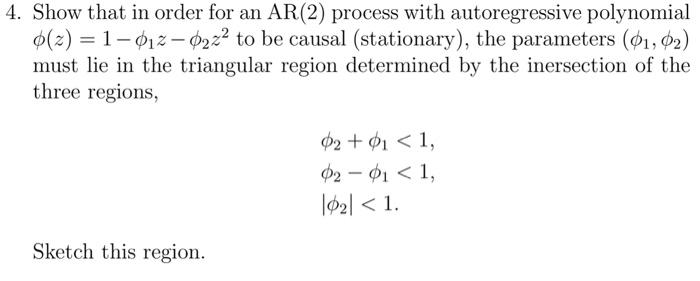

Solved 4. Show that in order for an AR(2) process with | Chegg.com

Solved Autocorrelation function of an AR(2) Process (time | Chegg.com

SOLVED: Consider the AR(2) process below: Xt = 0.8Xt-1 + 0.12Xt-2 + Zt ...

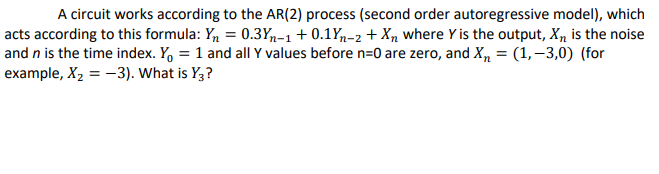

Solved A circuit works according to the AR(2) process | Chegg.com

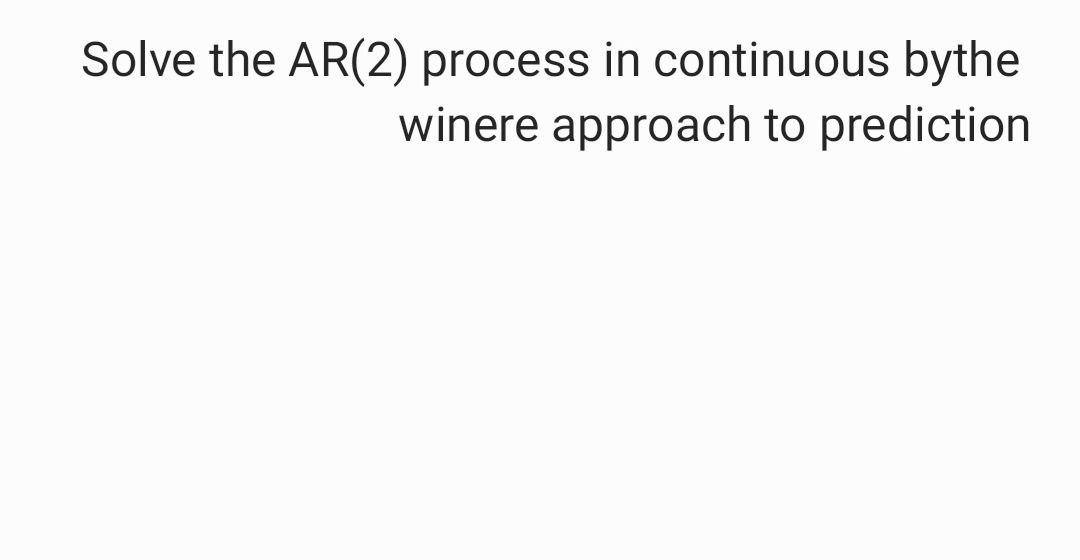

Solved Solve the AR(2) process in continuous bythe winere | Chegg.com

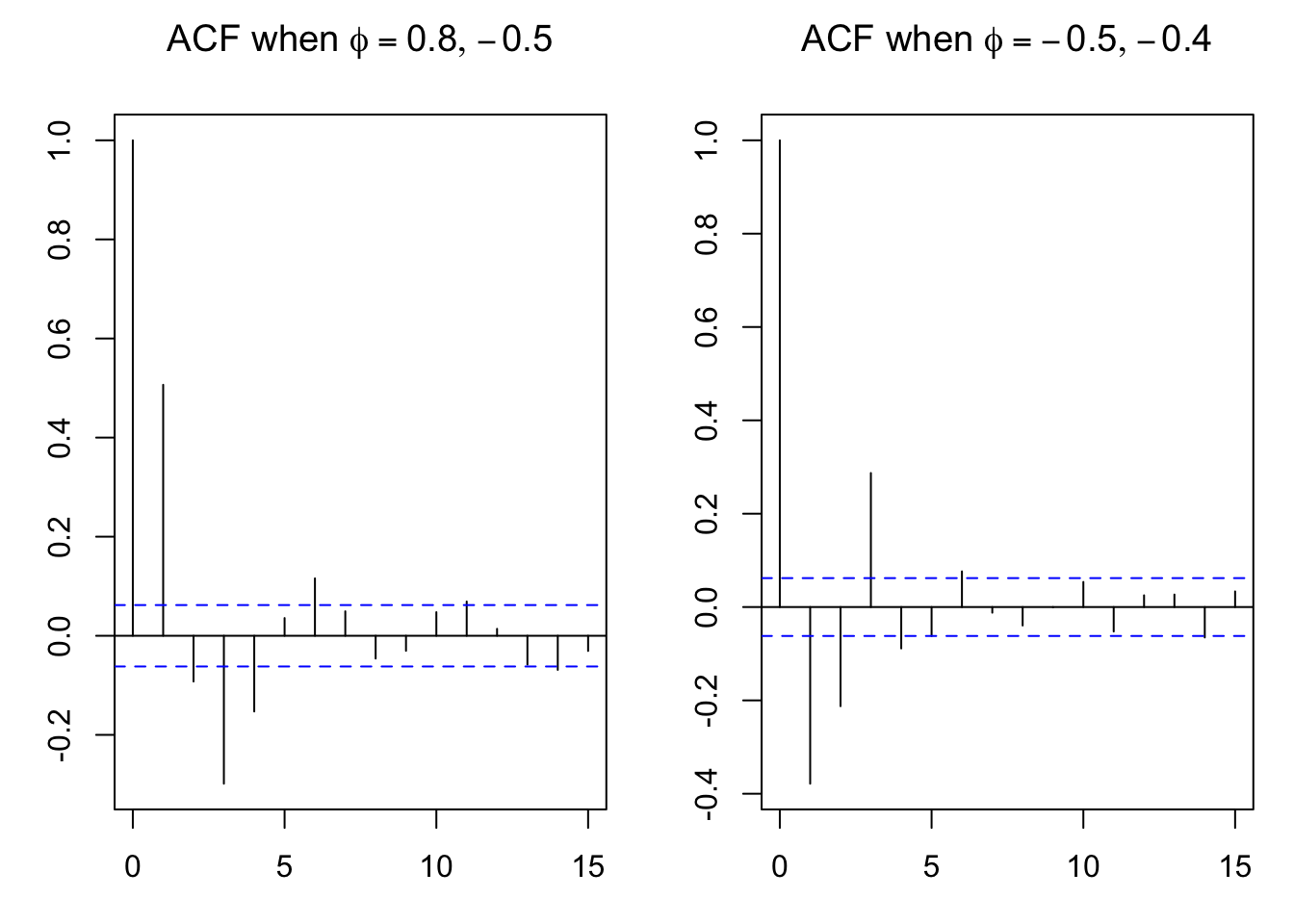

Autorcorrelations of AR (2) Model - YouTube

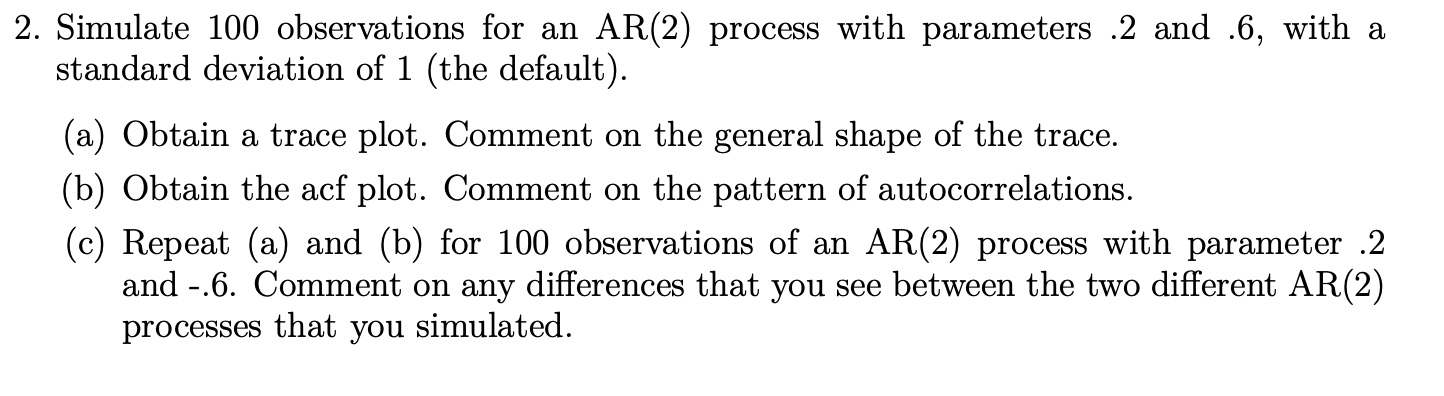

2. Simulate 100 observations for an AR(2) process | Chegg.com

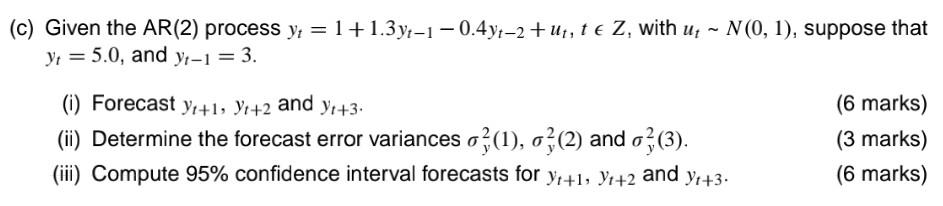

Solved (c) Given the AR(2) process | Chegg.com

AR(2) process with complex unit roots and a cycle of 100 periods ...

Example of two artifically generated time series of AR2 processes ...

Consider the following stationary AR(2) process Yt = | Chegg.com

Solved - For the AR(2) process (Xtit e Z) given below, X+ = | Chegg.com

Solved (b) Show the following AR(2) process is causal. (1 – | Chegg.com

Solved 1. Consider the AR(2) process below: | Chegg.com

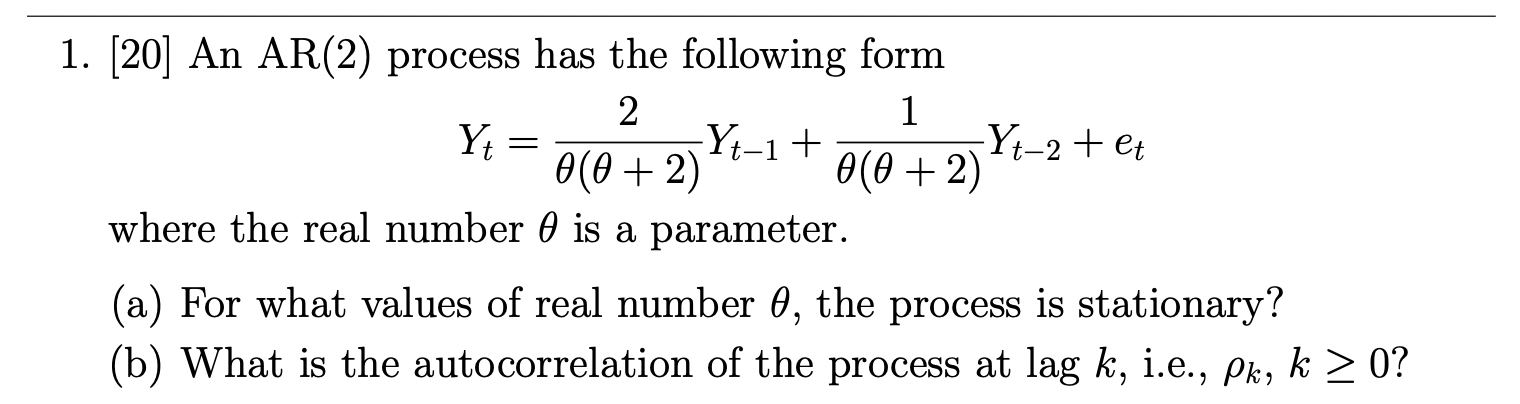

Solved : t- 1. [20] An AR(2) process has the following form | Chegg.com

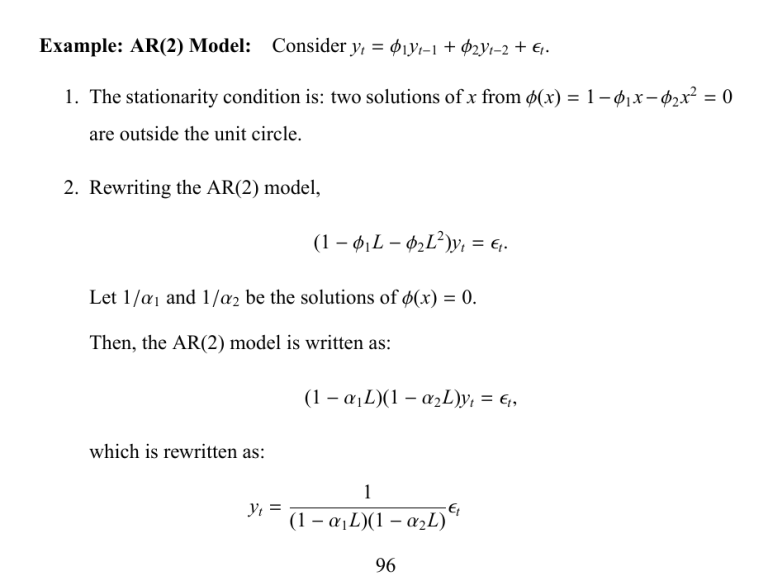

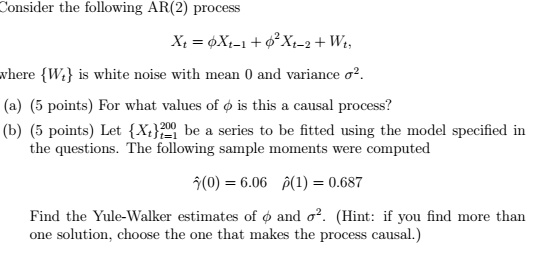

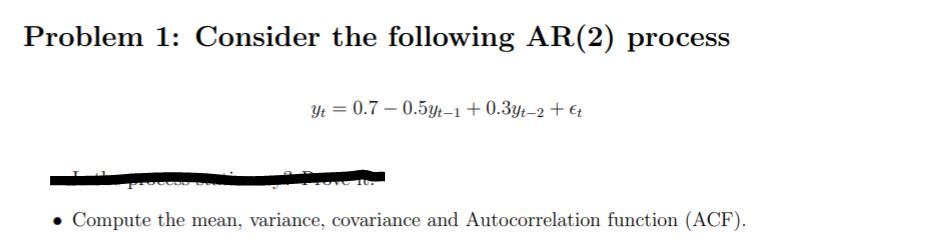

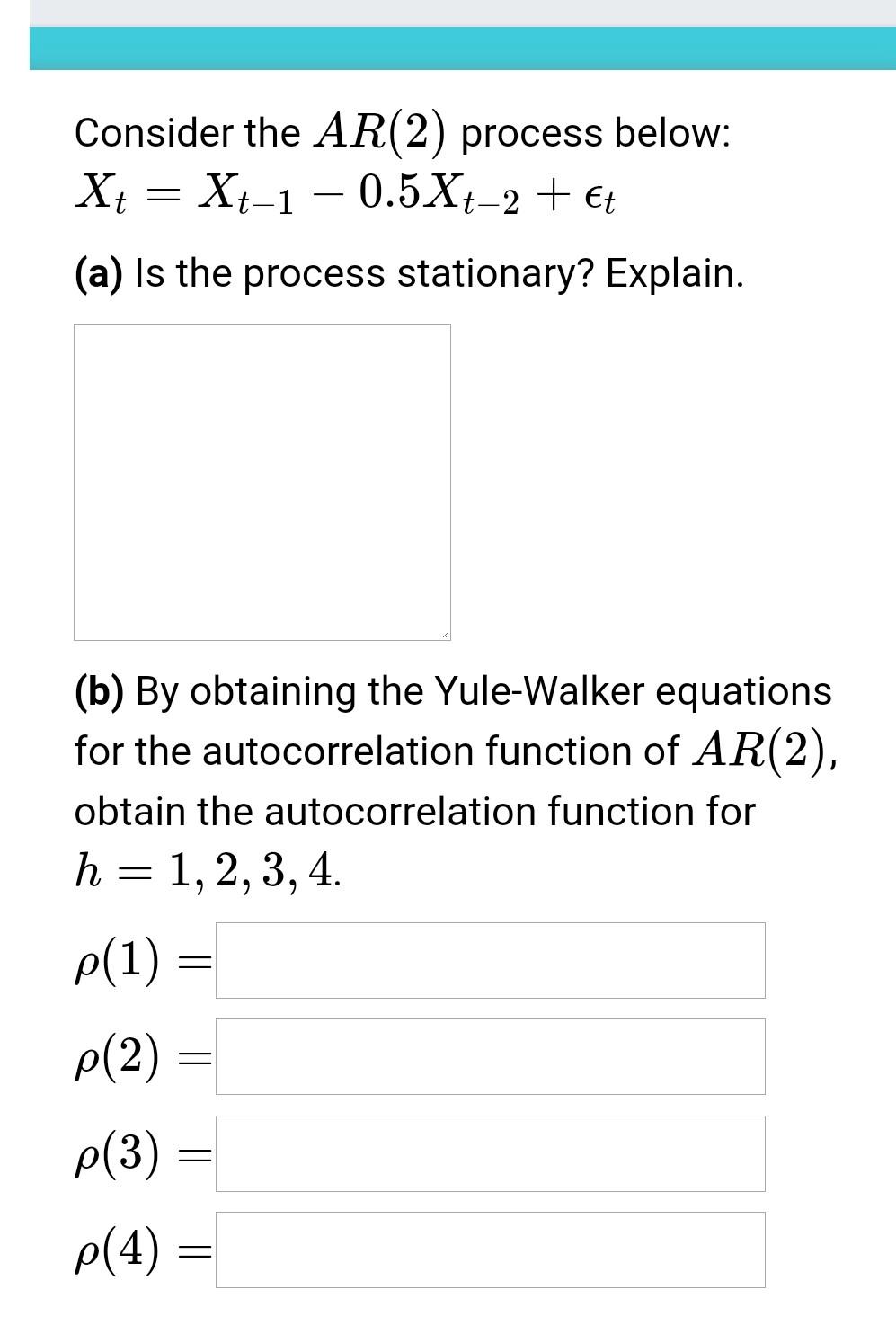

Solved Problem 1: Consider the following AR(2) process | Chegg.com

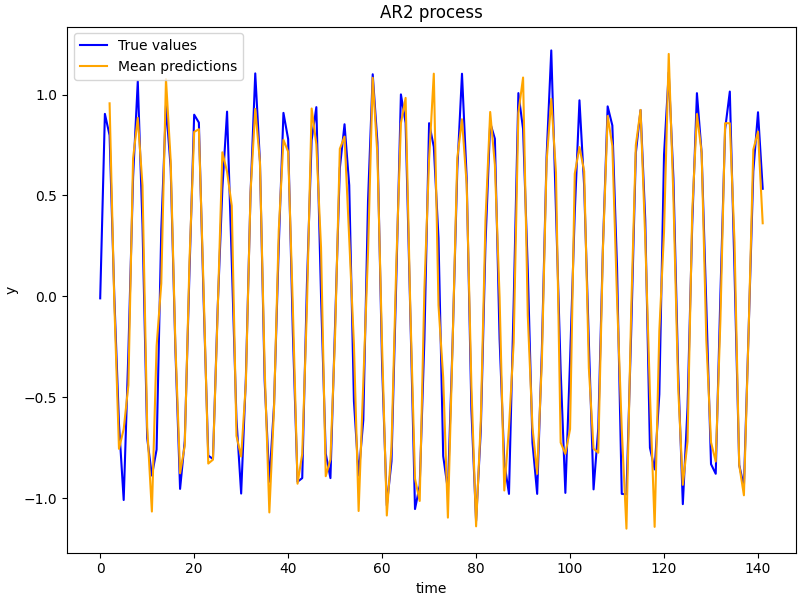

Example: AR2 process — NumPyro documentation

Solved Consider an AR(2) process X4 = 01Xt-1+02X4-2+ Zt, | Chegg.com

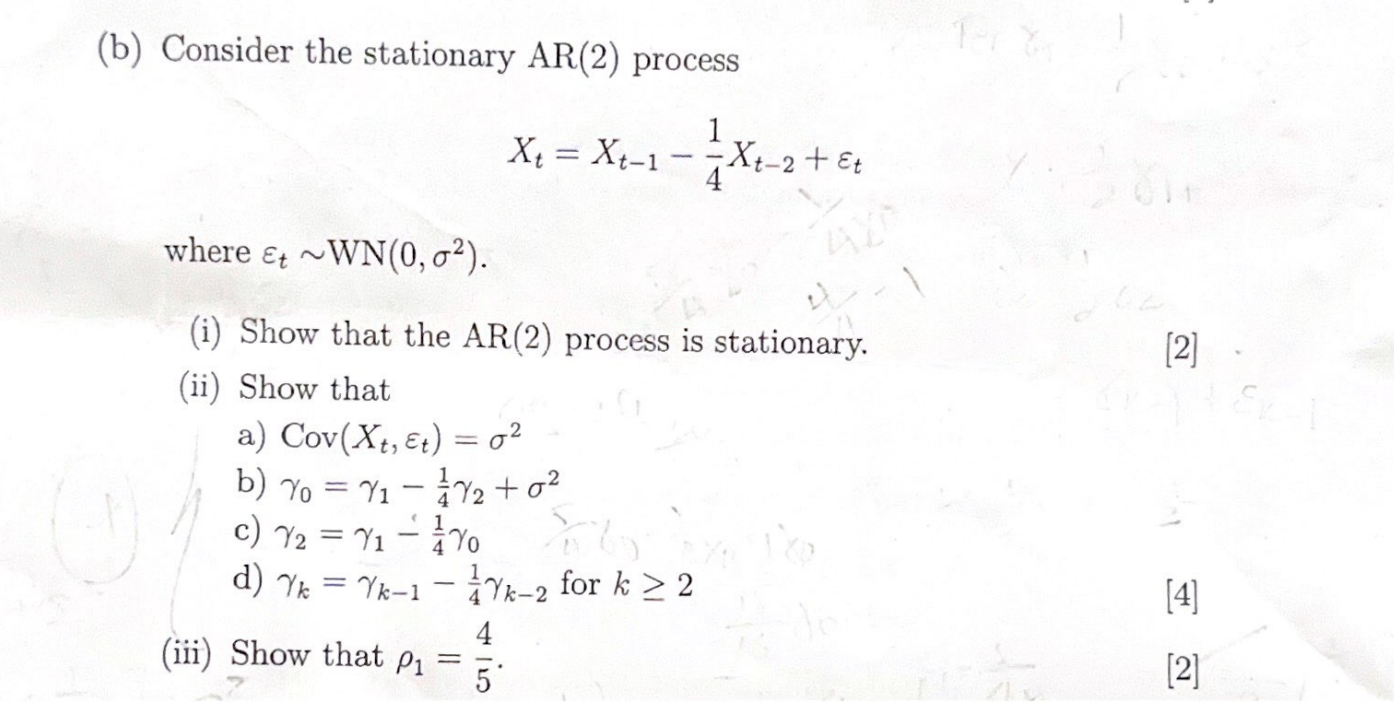

Solved (b) Consider the stationary AR(2) process | Chegg.com

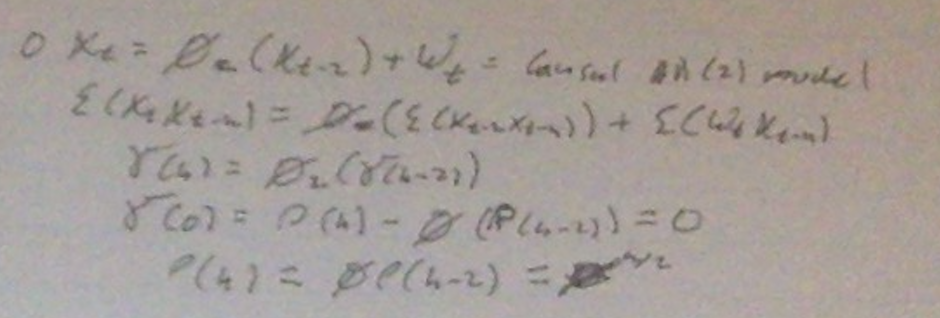

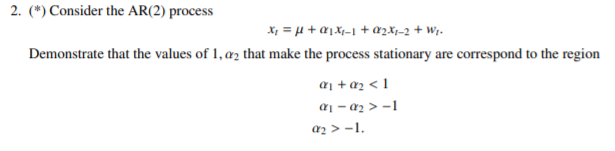

Solved 2. (*) Consider the AR(2) process X = 4 +01.X-1 + | Chegg.com

3. a. Consider a causal AR(2) process Xt - ϕ1 Xt-1 - ϕ2 Xt-2 = et where ...

Autoregressive processes. (a) time series of an AR2 process with ...

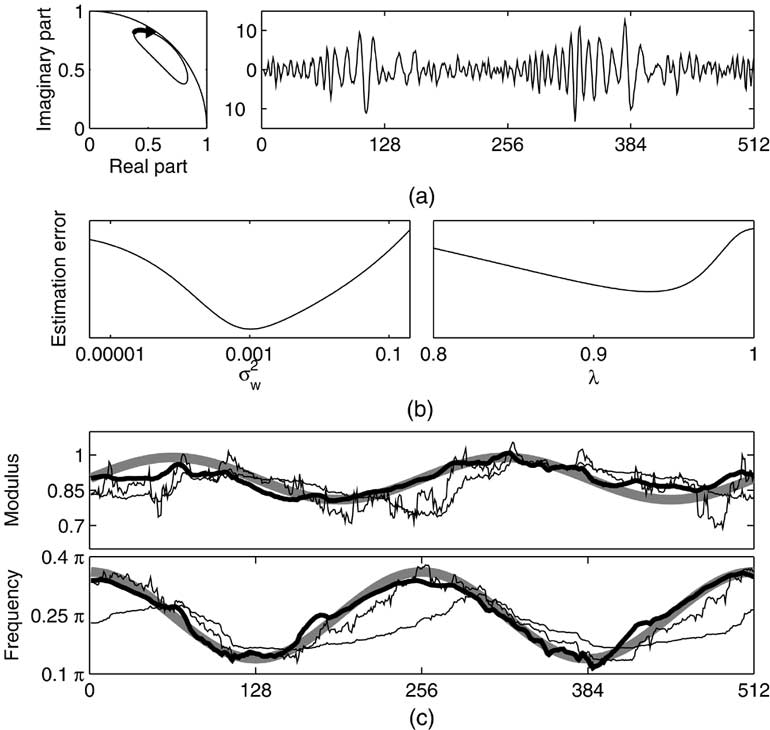

AR(2) process estimation with Kalman smoother and RLS algorithms. (a ...

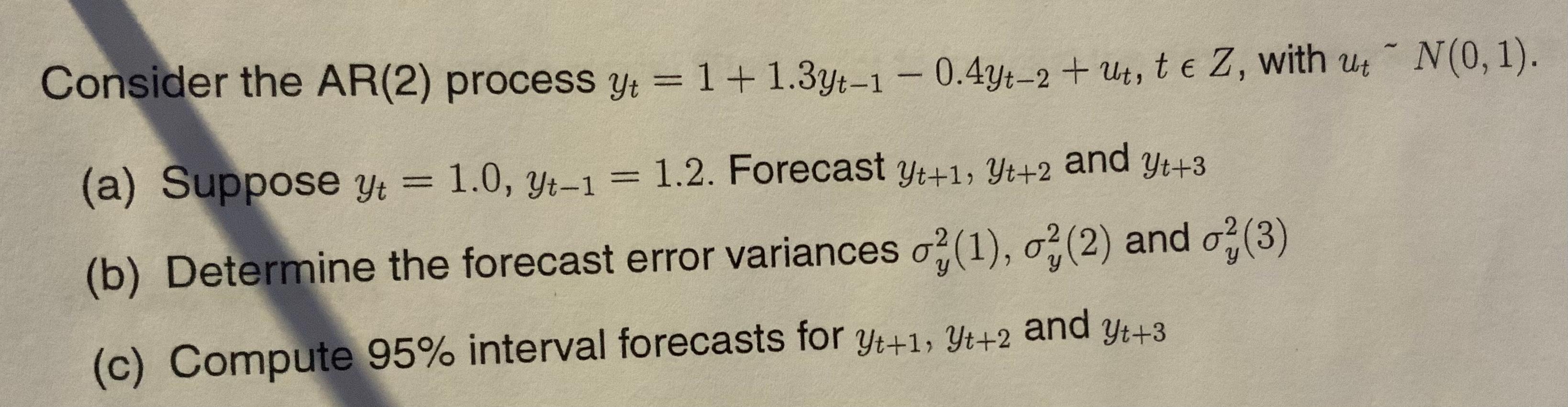

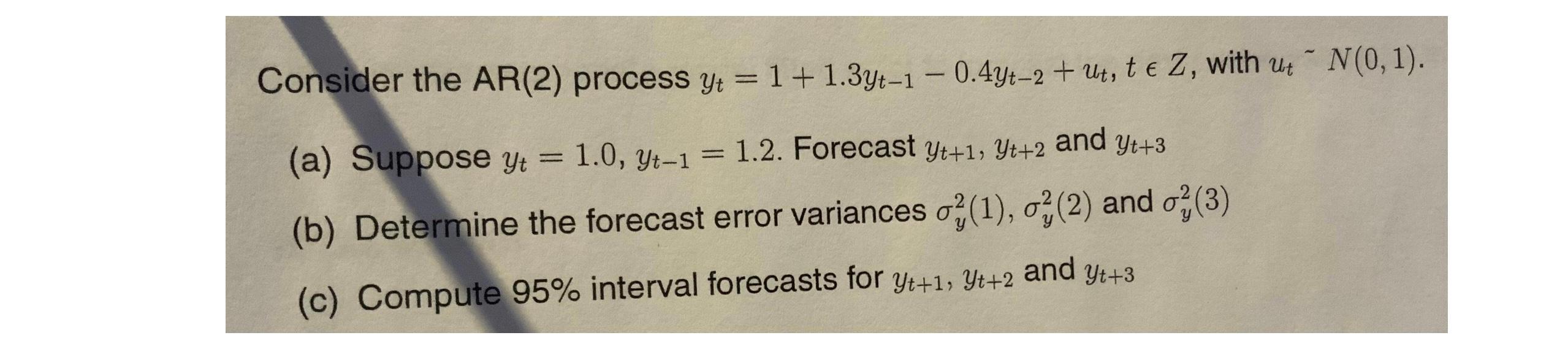

Solved - (b) Consider the AR(2) process y = 1 + 1.3yt-1 − | Chegg.com

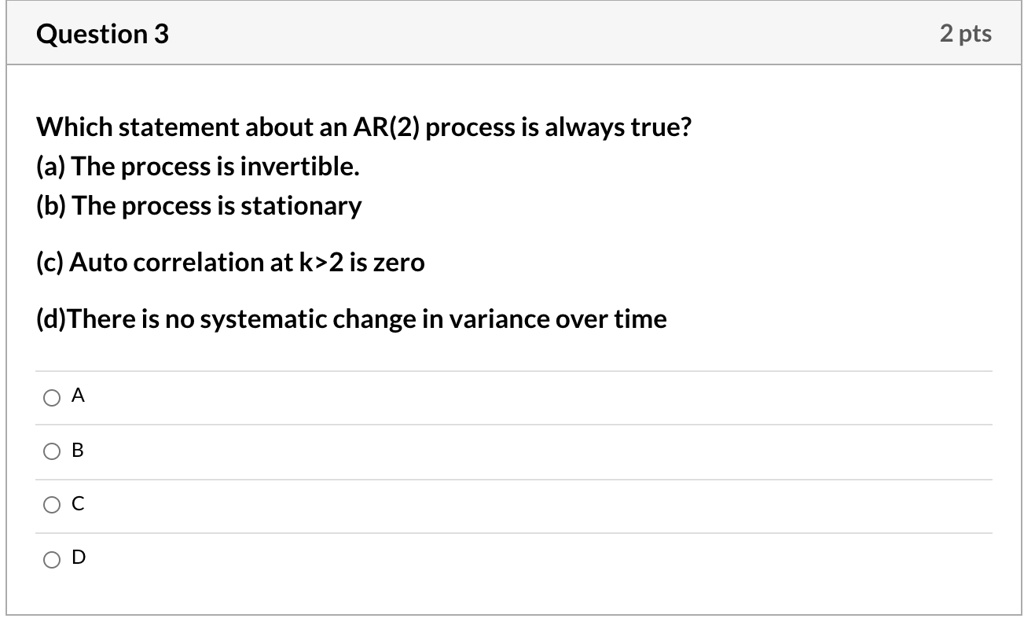

SOLVED: Which statement about an AR(2) process is always true? (a) The ...

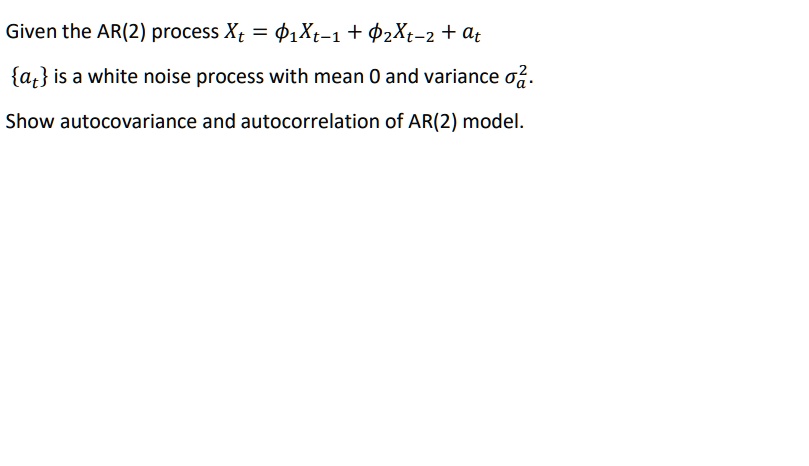

Given the AR(2) process Xt = ϕ1 Xt-1 + ϕ2 Xt-2 + at {at} is a white ...

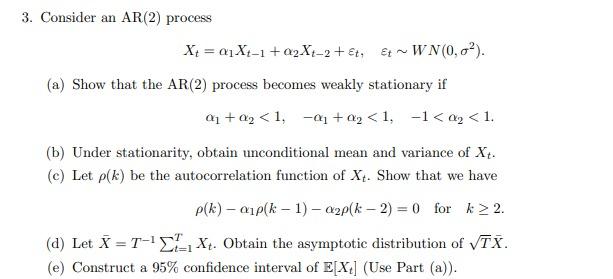

3. Consider an AR(2) process | Chegg.com

Solved Consider the following AR(2) process where {W, } is | Chegg.com

Solved 6. Consider the AR(2) process xn=a1xn−1+a2xn−2+vn. If | Chegg.com

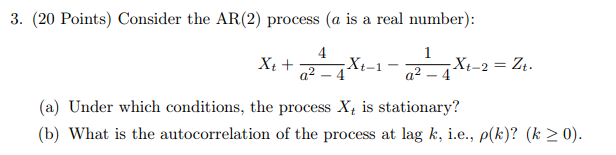

Solved 3. (20 Points) Consider the AR(2) process (a is a | Chegg.com

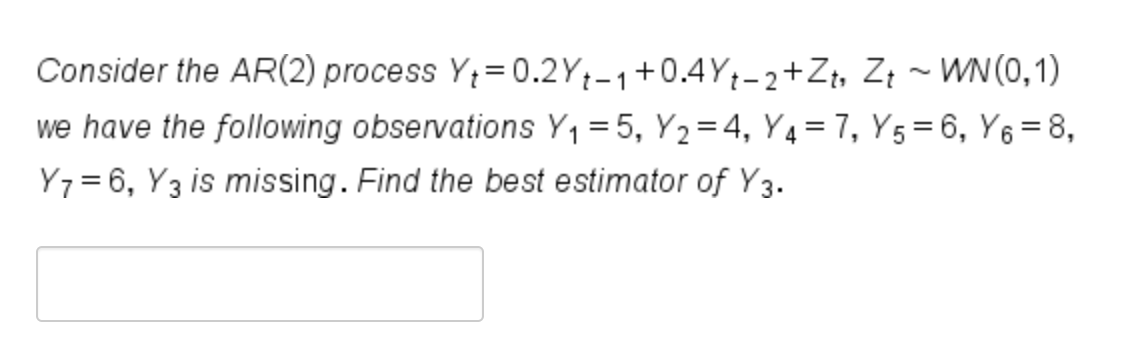

Solved Problem 1: Consider the following AR(2) process Yt = | Chegg.com

Stationary variance of AR(2) process – Physics of Risk

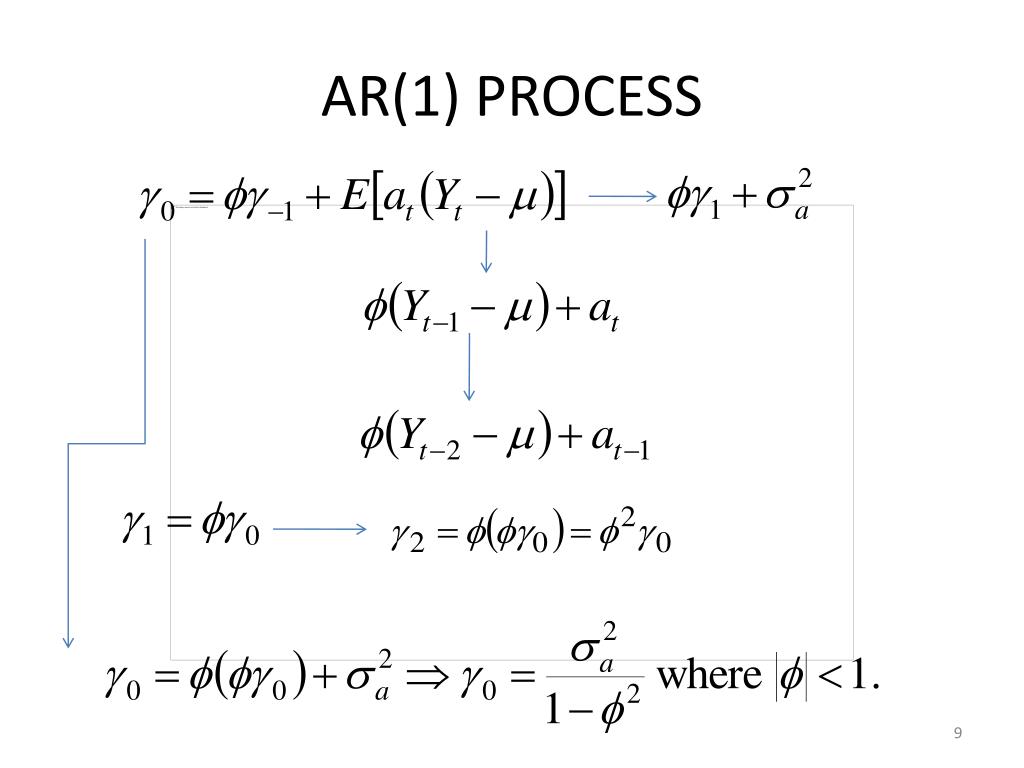

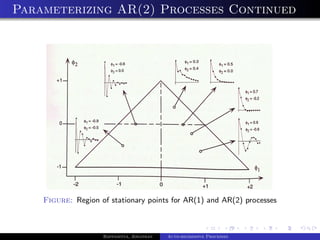

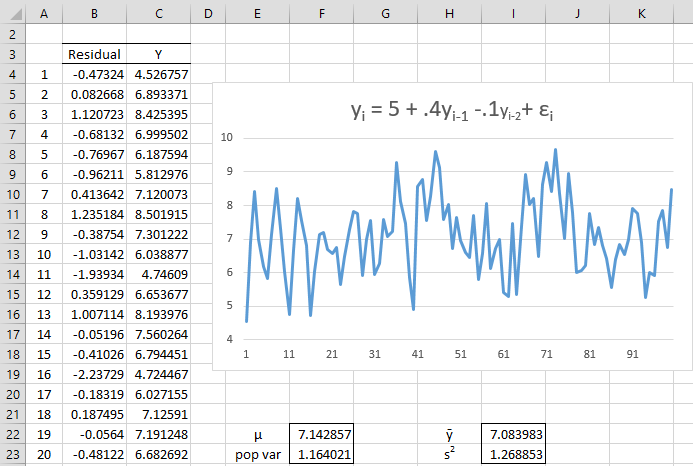

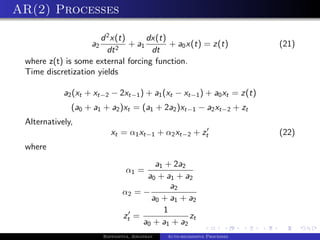

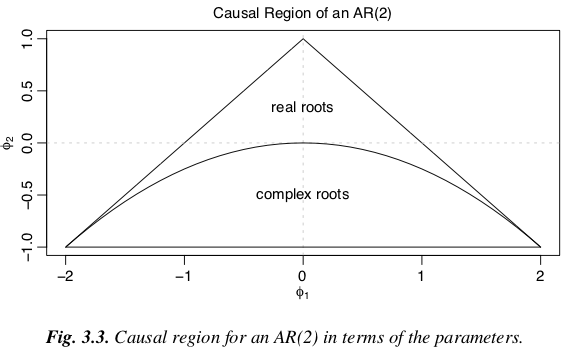

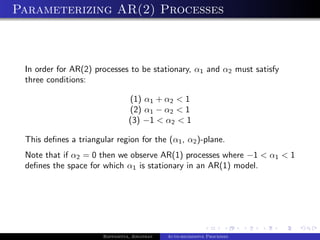

The Stationary AR(2) Process

Solved = 2. (20) Consider the following AR(2) process Y+ = | Chegg.com

Solved 5. Consider an AR(2) process X = 0,X:-1 + 2X-2+ Zt, | Chegg.com

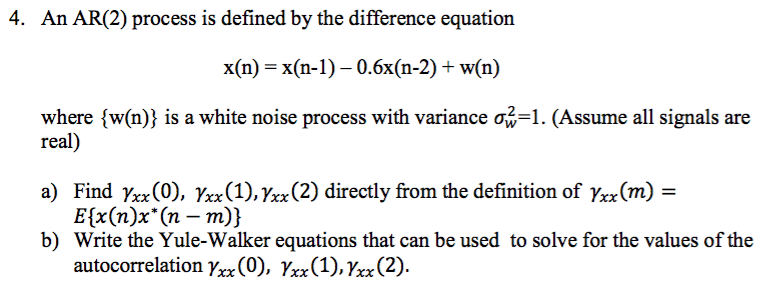

4. An AR(2) process is defined by the difference | Chegg.com

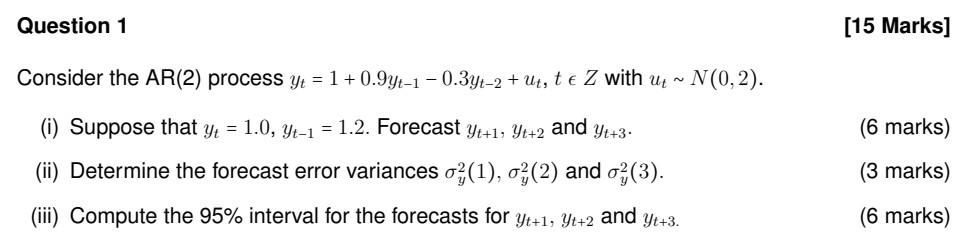

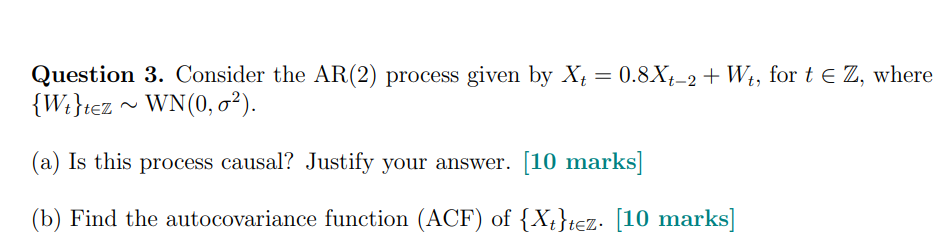

Solved Question 3. Consider the AR(2) process given by | Chegg.com

Solved 4. Consider the following AR(2) process X+ = Q_X-1 + | Chegg.com

AR models – Forecasting Essentials and Notes: Online Resource

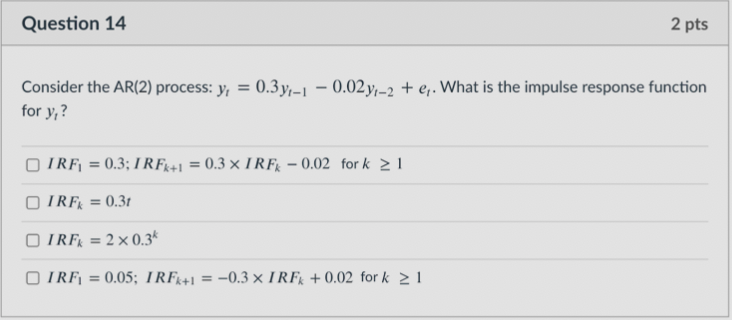

Solved Question 14 2 pts Consider the AR(2) process: y, = | Chegg.com

Lecture 13 Time Series: Stationarity, AR(p) & MA(q) - ppt download

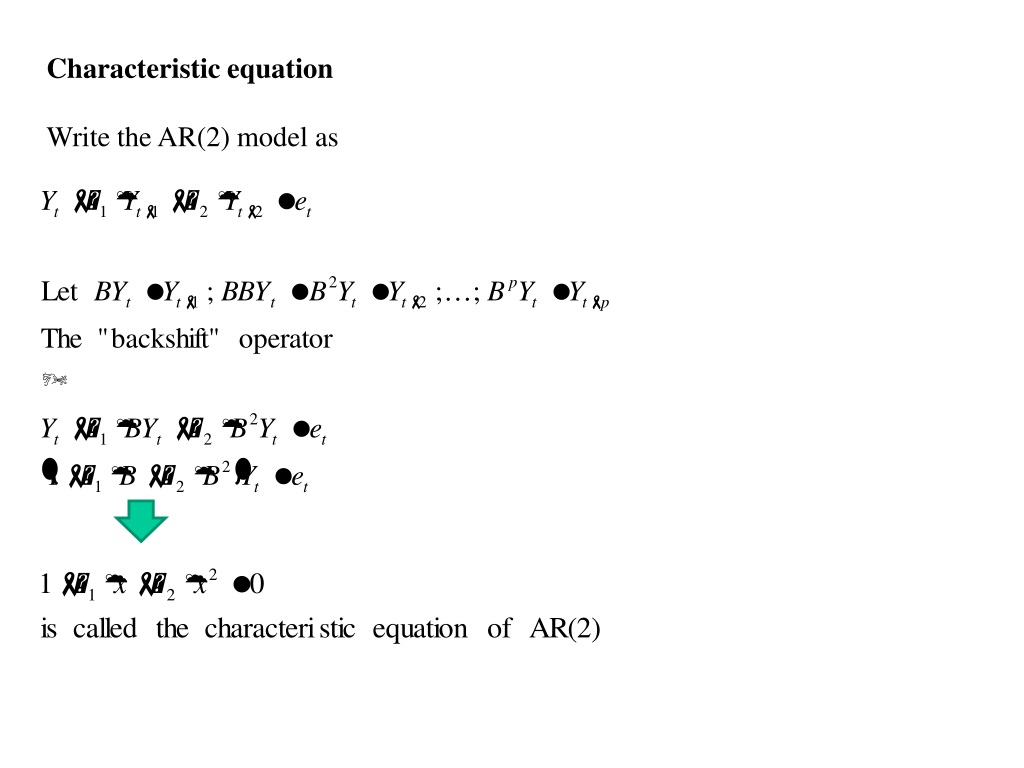

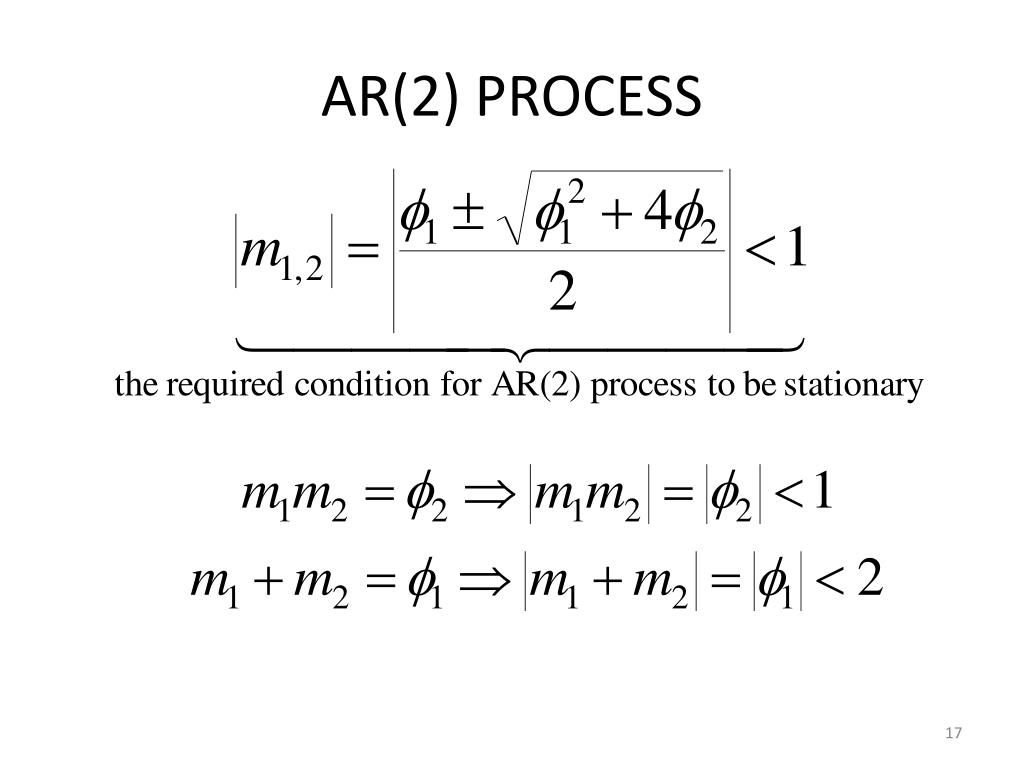

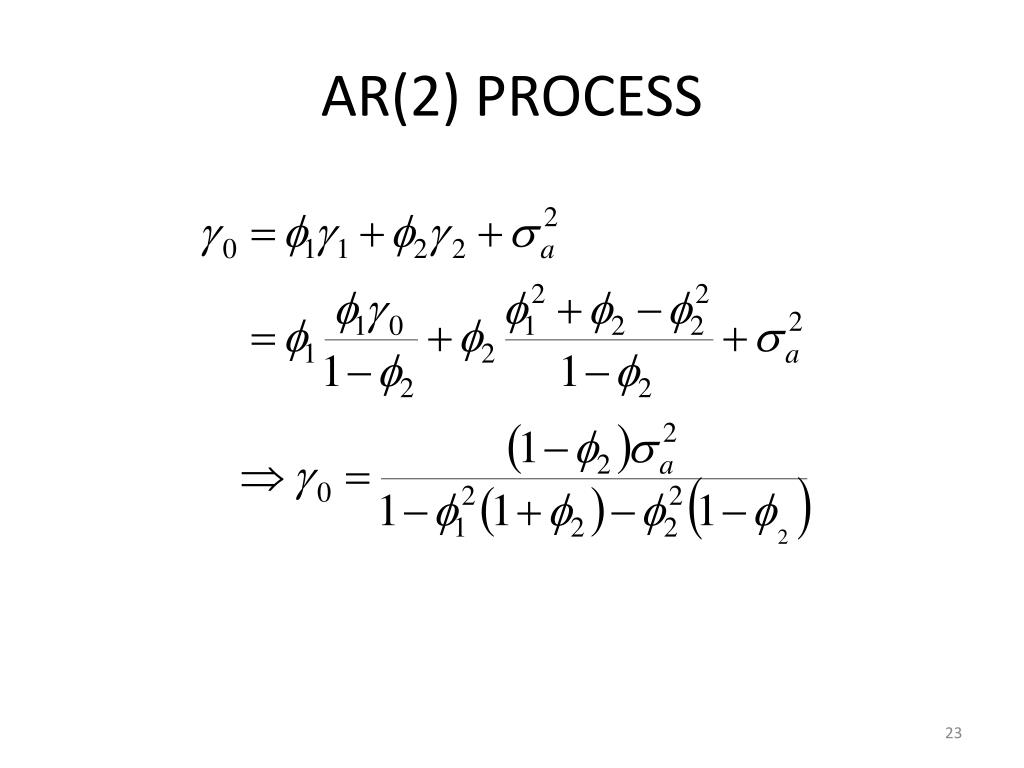

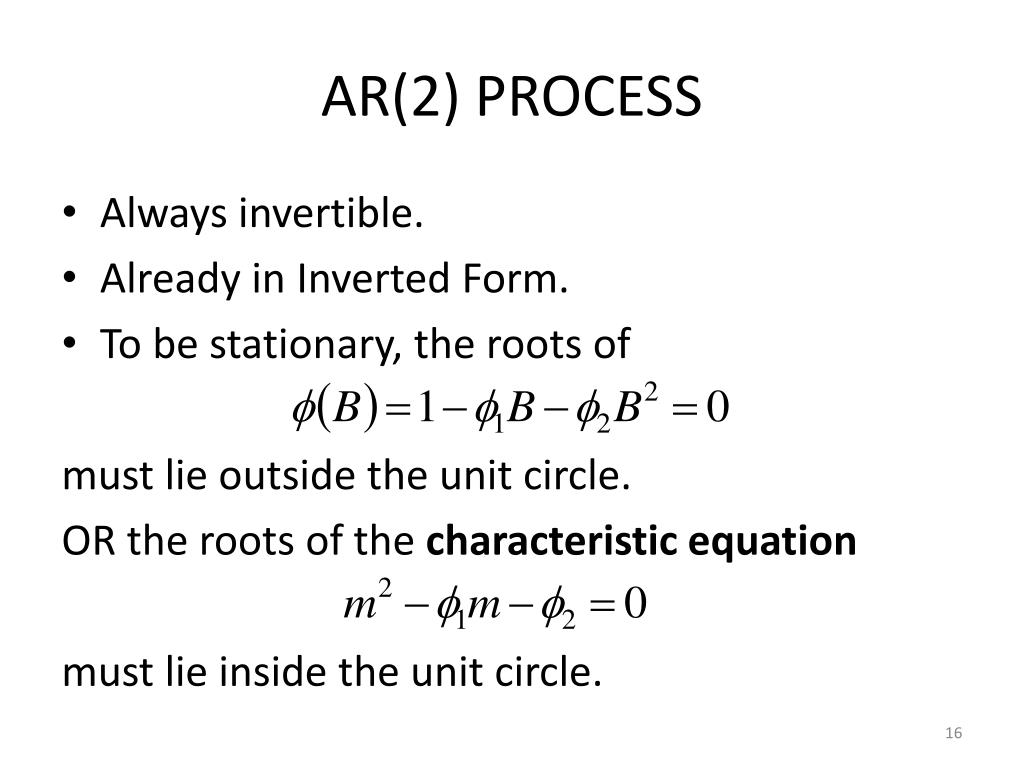

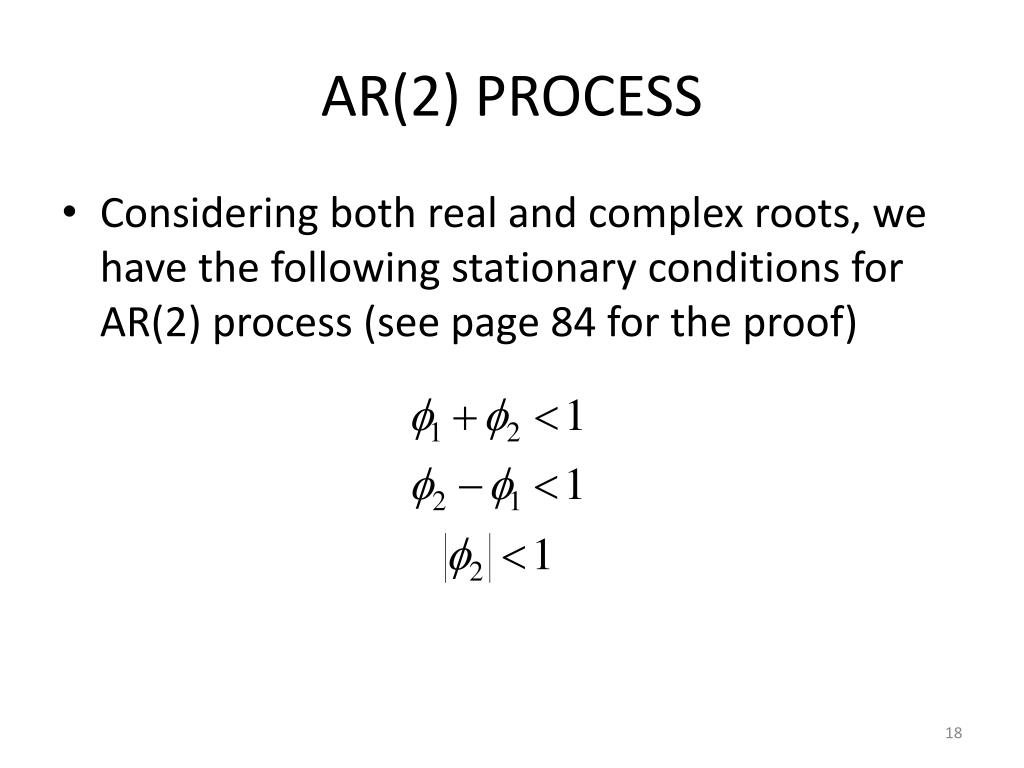

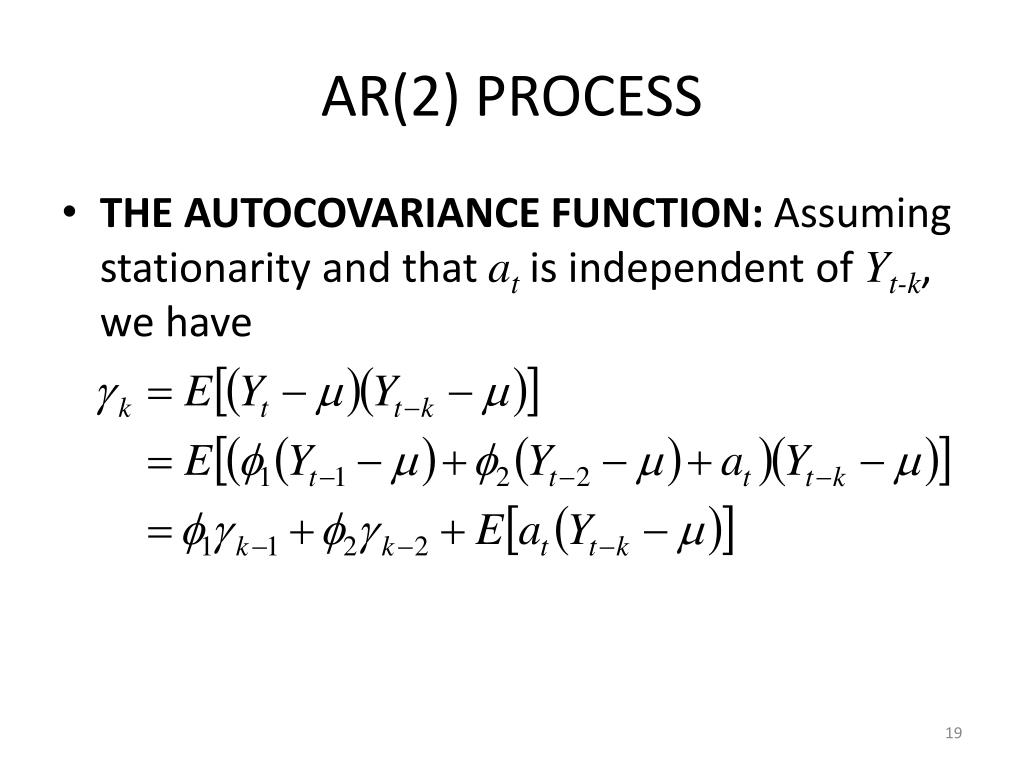

PPT - STAT 497 LECTURE NOTES 3 PowerPoint Presentation, free download ...

PPT - BABS 502 PowerPoint Presentation, free download - ID:3910986

Autoregressive processes : learning with an interactive tool – pierreh.eu

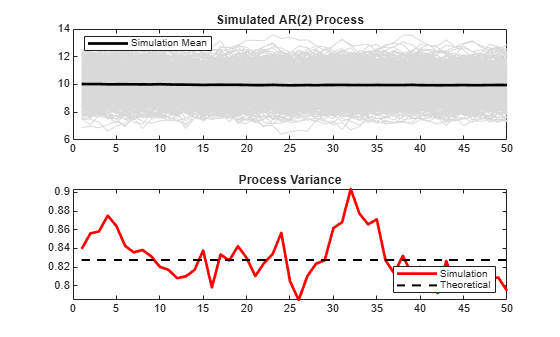

Simulate Stationary Processes - MATLAB & Simulink

Autoregression | PDF

Solved 3.7 For the AR(2) series shown below, use the results | Chegg.com

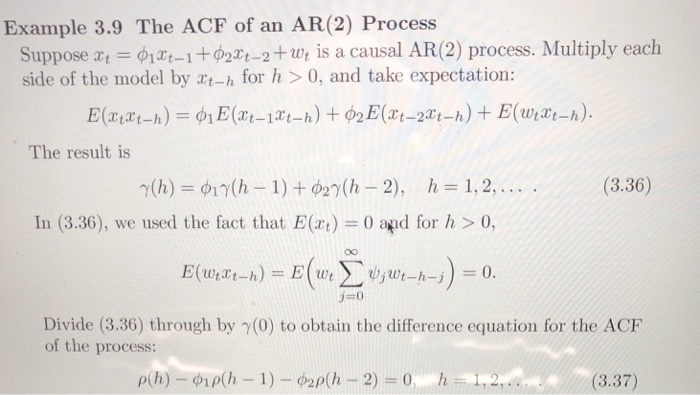

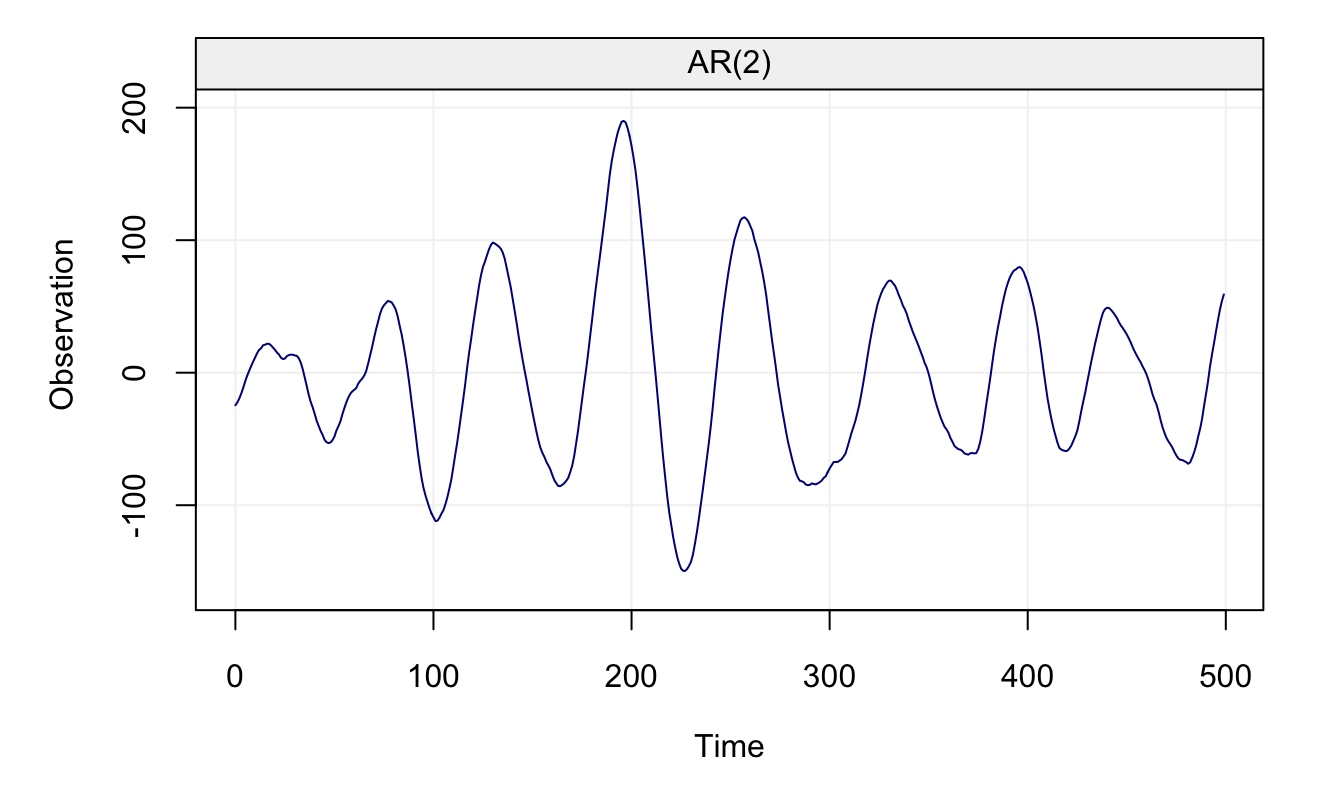

Applied Time Series Analysis with R

Partial Autocorrelation AR(p) | Real Statistics Using Excel

Stationarity Conditions for AR(2) Processes - YouTube

Time Series Course Dr. Maha Omair - ppt download

AR(2) models fit to LFP data a Power spectra of synthetic signals ...

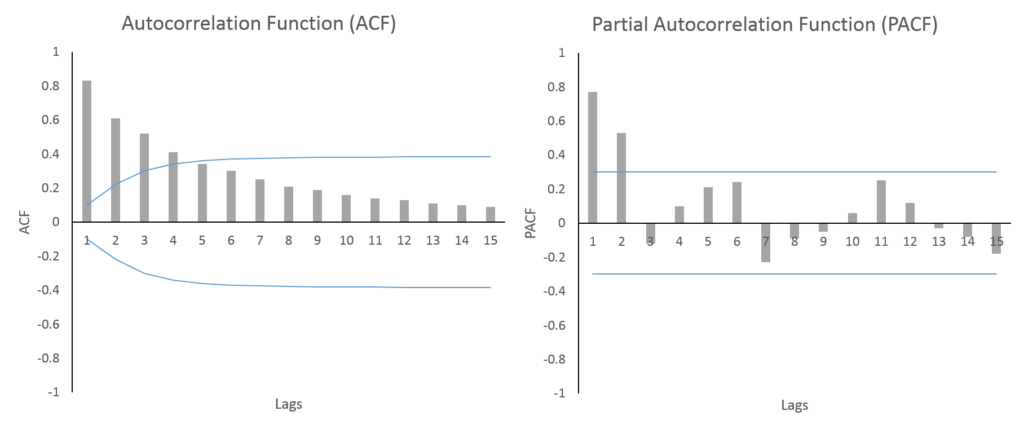

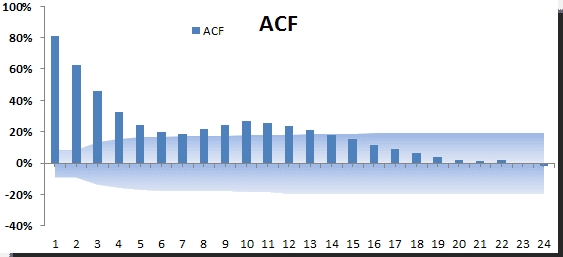

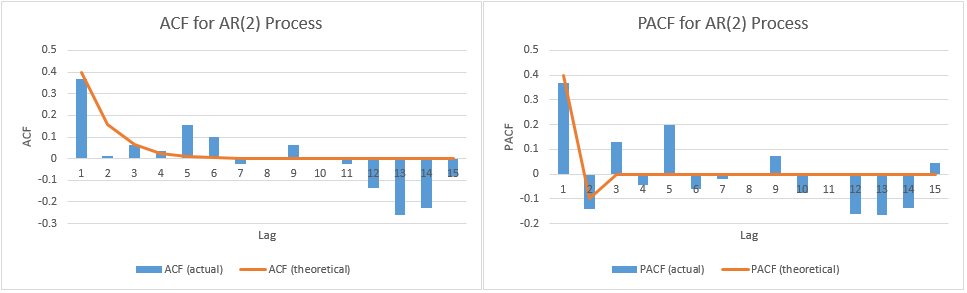

Interpreting ACF and PACF plots - SPUR ECONOMICS

PPT - Auto Regressive, Integrated, Moving Average PowerPoint ...

AR, MA, and ARMA Models

PPT - Command Sergeant Major Board of Directors Break-Out Session CSM ...

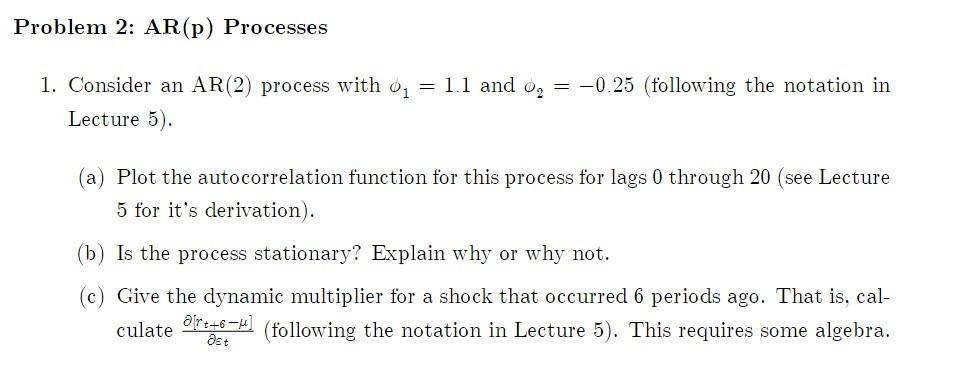

Problem 2: AR(p) Processes = = 1. Consider an AR(2) | Chegg.com

Q2. For the AR(2) series shown below, use the results | Chegg.com

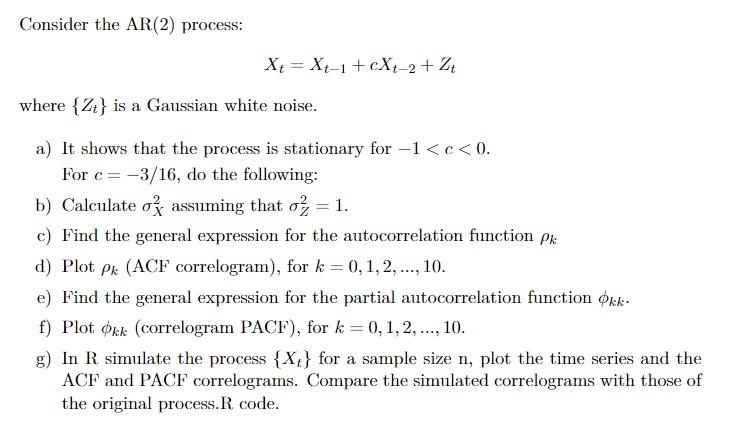

Solved Consider the AR(2) process:xt=xt-1+cxt-2+Ztwhere | Chegg.com

Solved Consider the AR(2) process, (X). given by X, = 21 | Chegg.com

A Correlogram tale – Help center

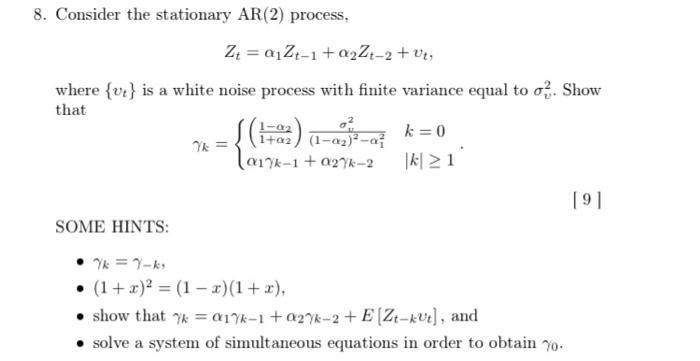

Solved 8. Consider the stationary AR(2) process, | Chegg.com

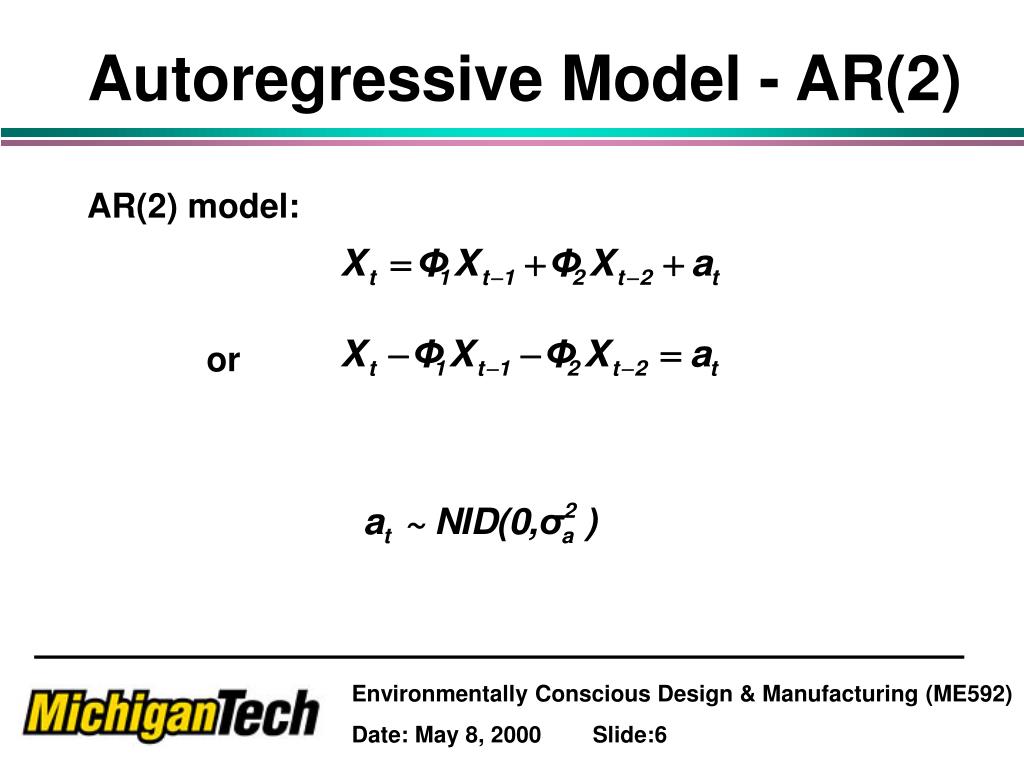

PPT - Environmentally Conscious Design & Manufacturing PowerPoint ...

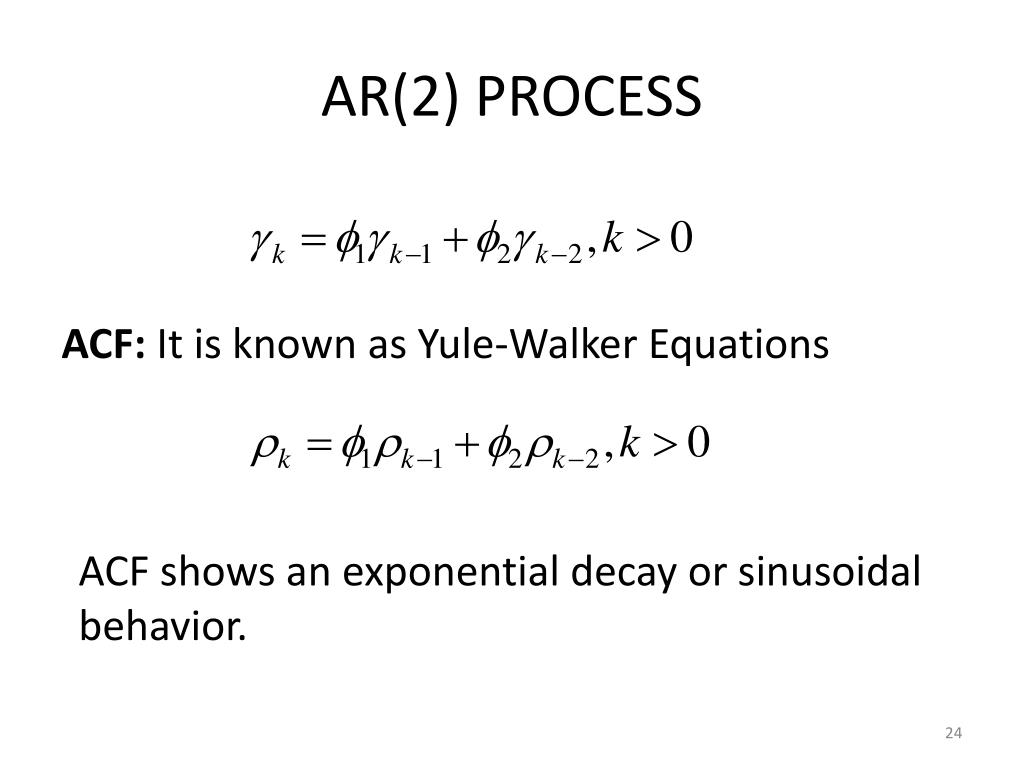

AR(2) and AR(p) Models: Time Series Analysis

Solved Consider an AR(2) process of the | Chegg.com

Solved Suppose we have the following AR(2) | Chegg.com

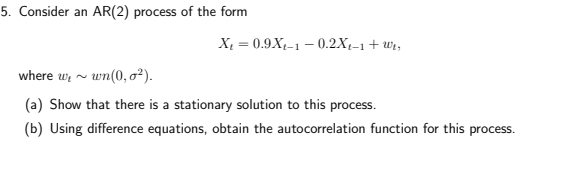

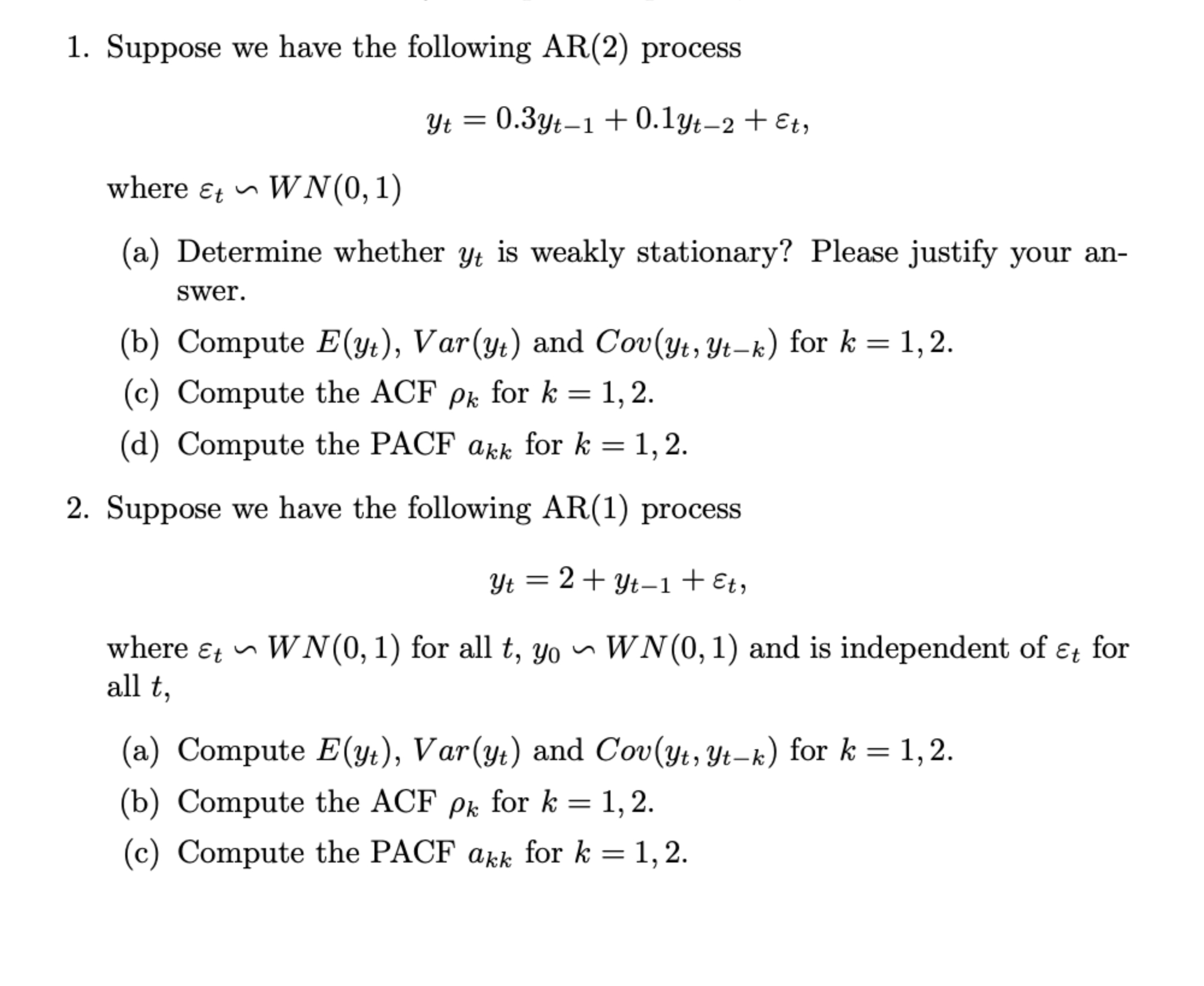

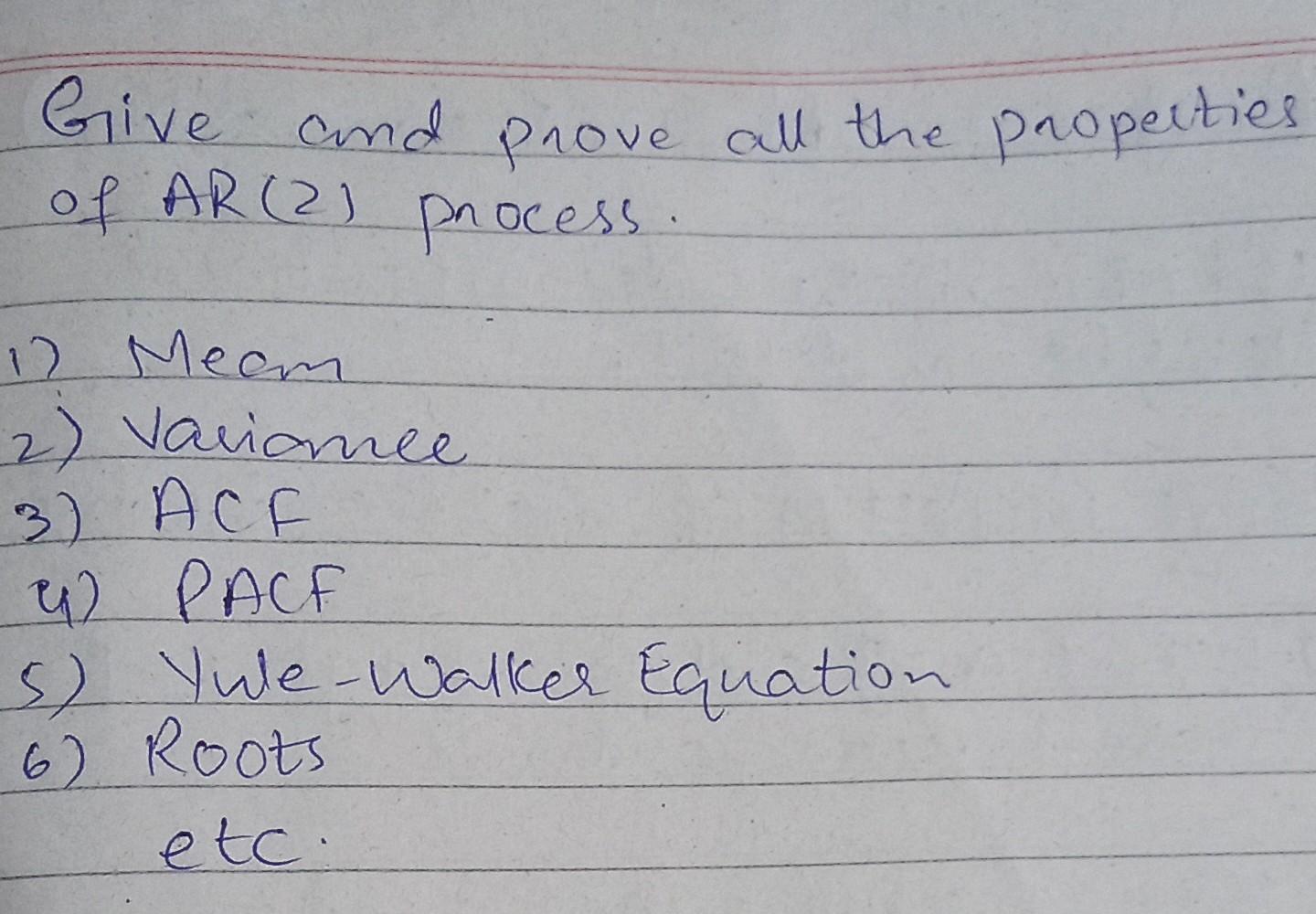

Give and prove all the properties of AR(2) process. | Chegg.com

.jpg)

.jpg)